Bonnie Koo

I grappled with productivity and efficiency in 2018.

“I don't have time,” came out of my mouth too often. And, I had lots of proof that I didn't have a lot of time. I work as a dermatologist, it was my first year with a new baby who needed my attention, I do all the meal planning and other household management. Oh, and I work on this blog.

Yet, I had plenty of time.

I've spent the past several months trying to figure out how I couldmake 2019 more productive, so I can have more free time with myself and my family. I've spoken to friends and coaches, read blog posts and listened to podcasts on productivity.

Productivity is your ability to increase your effectiveness and efficiency – not just working more. Don't we all want to work smarter and not harder?

So here are my top 5 tips to make 2019 more productive.

#1. Commit to being productive

The first step is to get your mindset right. Get to it or stay unproductive.

Your choice.

#2. Find a system that works

This is the part that may take some time and tweaking. It took me several months to figure out what would work for me.

I use google calendar, a journal, and Asana to organize my life and business.

I've always used google calendar to organize appointments so that part was easy. It syncs to my iPhone's native calendar. I have 3 calendars: personal, work, and joint (with Matt).

The next two parts took time and effort to learn and use optimally. I initially tried a beautiful templated paper planner by Ink & Volt. I loved the planner and the templates – but I never used the planner. In fact, I have two of these beautiful planners with very little writing in it. Failure indeed.

I next tried the bullet journal. It seemed like the perfect solution! I would no longer “waste” pretty templated pages since I created the template. I even purchased some pretty washi tape and colored gel pens. The bullet journal works for many people. But for folks juggling a zillion things including a business, it just didn't scale well. I also would forget to bring my journal with me sometimes and then not have any clue what I should be working on.

At #FINCON18 two friends (Ryan Inman of Physician Wealth Services and Travis Hornsby of Student Loan Planner) told me I have to check out Asana. They told me I could use it not just to keep my to-do list in order but to also organize and plan my blog post calendar. Best of all? It's free for most people. And the free version doesn't suck.

So I immediately signed up for an account and watched their tutorials. But I still didn't really know how to use it effectively. I was pretty good about entering tasks into the app but then quickly forgot about the tasks since they weren't organized. A few months went by. Then I watched this video by productivity master Paul Minors of New Zealand (complete with awesome accent).

I use Asana as my digital bullet journal. It keeps all of my personal and business to-do's in order. My podcast buddy Carrie Reynolds also uses it and we are able to collaborate and plan our podcasts much more efficiently now. I also use Asana for my virtual assistants.

Before hopping onto Asana, I recommend watching this introductory video on why Asana is so awesome.

#3. Start a weekly planning session

I now use my paper journal for my weekly planning sessions and general scratch paper. Every Sunday, I take about 30 minutes and plan my week. I first start with a few minutes reflecting on the previous week. I acknowledge what I accomplished the previous week. And I acknowledge what didn't work.

I then review my tasks in Asana by browsing the “Calendar” project. This project contains all of my tasks.

The key to never forgetting about a task in Asana is to assign it a “due date” and add it to the “Calendar” project as soon as you enter it. I use the due date as a start date instead. Every task is in at least 2 projects – the project it belongs to and “Calendar”. Calender is a repository of all tasks assigned by quarter. I also have a “Soon” and “Later” sub-category within Calendar as well. I basically use the Asana system outlined in the video above.

During this weekly review, I move the tasks I want to work on this week into my “In Progress” project. I use the board view here so I can visually see all the tasks I need to work on this week.

Regardless of what system you use to organize your tasks, use this weekly session to review tasks, re-prioritize and plan the week. This is also when I meal plan for the week.

#4. Limit distractions

In the age of screens and social media, this step is absolutely pivotal to if you want to make 2019 more productive.

Want to be productive? Turn off notifications. Close the Facebook tab in your browser. Unplug.

Warning — it may feel uncomfortable to do this. You may feel anxious. You will soon appreciate this quiet time and be amazed at what you can accomplish.

Did you know that our smartphones are specifically designed to keep us using them? Ever feel a little anxious when you don't check your phone (or email or that notification that just popped up?). Screens are the new addiction and ruining productivity.

Take the time to really consider how to use technology vs. letting it use you.

#5. Take care of your body and mind

It's pretty hard to be productive if you're tired, hungry or not feeling well.

So yes, you need to get enough high-quality sleep, eat well and exercise regularly.

Final Thoughts on Tips to Make 2019 More Productive

Change is hard. But if you're committed to your goals this year, you need to boost your productivity. Take one tip from this list and work on implementing it for a month. Then, see if you can add another. As you feel your productivity increase, so will your motivation. That's a cycle you want to get caught in.

What are your top productivity tips? How do you plan to make 2019 more productive? Comment below!

Join the Wealthy Mom MDs Facebook Group to continue the conversation!

This is a guest post from my fellow woman physician blogger, Dr. B.C. Krygowski. She's a palliative medicine physician who discovered FI & Frugality as a way of life. She blogs at bckrygowski.com, and she has ten tips that any high-income earner should try out to add more frugality to their lives.

# 1. Look into Home Exchange.

Home exchange saves me serious money because I can swap homes and cars with other families for overseas vacations.

# 2. Schedule a half-day to sit down and figure out your priorities.

Do you say you want to be mortgage-free more than anything, yet you continue to take four (or more) exotic trips a year? Your life actions say something different than your words. Maybe consider cutting the exotic trips down to one or two a year and put the money you’ve saved towards paying off your mortgage instead.

# 3. Track your expenses.

Doing this helped me to find acceptable, but less expensive ways to achieve the same quality of life.

# 4. Commit to one month of decluttering your house.

Seriously, this is guaranteed to make you spend less money. You’ll be horrified at all the stuff you toss, give away or donate during a one-month declutter binge. In the future you will stop buying so much stuff.

# 5. If you have an Aldi near you, learn to embrace Aldi.

Shopping at Aldi helped us slash our food bill The trick is to stock the car with bags and quarters so you can get a shopping cart and bag your own groceries. Aldi saves us time too: it’s the quickest grocery store to get in and out of. They also now deliver with Instacart.

# 6. Learn to cut hair—don’t be afraid, you can do this!

When my husband started to read Mr. Money Mustache, he went to Walmart and bought a color-coded, foolproof hair trimmer. It came in a plastic container with instructions. I discovered that after a few tries I could cut men’s hair. I estimate this $22 investment saved us about $6,000 over the years of cutting not only his but our two boys hair. Plus it’s saved us time because I don’t have to wrestle the kids into the car.

# 7. Stop shopping.

Send your significant other into the store instead. My husband goes in with a list and only exits the store with what’s on the list. It’s like he has blinders on when it comes to impulse purchases.

# 8. Embrace the Instant Pot.

Not only will this fantastic device save you time, but oodles of money too!

# 9. Learn how to store food properly, so you waste less.

I have to admit though, I’m a visual person, so the mushrooms kept going bad when we’d put them into brown paper bags. Out of sight, out of my epicurean mind. I’ve taken to propping them on their side on the shelves at eye level, so they’re the first things I see when I open the fridge door.

# 10. Periodically examine your expenditures sheet with your significant other.

This falls under “What are your goals/priorities?” We sit down a few times a year to examine our spreadsheet and analyze where we should spend not only less but also more money.

Girlfriends, I have faith in you taking control of your finances—you got this!

Yours,

Final Thoughts on Frugal Tips for High-Income Earners

It's easy to fall into the trap of allowing a high income to dictate high spending. You certainly don't have to use all these tricks all of the time. However, by making frugality a priority in your life as B.C Krygowski does, you'll be surprised how much money you can save and invest without feeling like you're making huge sacrifices.

Join the Wealthy Mom MDs Facebook Group to continue the conversation!

Did any of these frugal tips surprise you? What do you do as a high-income earner to keep more money in your bank accounts each month?

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – Heather!

Tell us about yourself:

Hello, I’m Heather. I’m family medicine and a brand-new attending. I practice both inpatient and outpatient medicine at an academic hospital, and enjoy spending time teaching residents and students in addition to my clinical duties. I was born and raised in a medium-sized city in the Midwest with the greater metropolitan area approaching approximately 1 million. Both of my parents are practicing physicians. They gave me a small amount of money toward my education (to be applied toward undergrad), but otherwise the rest has been paid for through scholarships and loans. I came back to the same city to complete my residency and am now just starting faculty. Because my parents both work, they aren’t incredibly helpful with childcare, but it is still wonderful to be close to family! My husband is in his final year of surgical subspecialty training, and also plans to work in the academic setting upon his graduation. I have two young children, and am expecting my third child soon. I can’t say I have much time for hobbies after just finishing my training in a dual-physician household with young kids. In my former life, I enjoyed soccer, skiing, traveling, reading, and spending time outside. I went into medicine because I love helping people reach their greatest health potential. In family medicine, I feel I am in a unique position to do this as I am able to care for patients in the clinic, providing preventative medicine, education, and chronic disease management. When patients are sick, I am able to see them in clinic and also care for them in the hospital. I especially enjoy working with underserved patients, and academic medicine allows me to have a great diversity of patients with the majority of my patients not speaking English. Most days, I am happy with my decision, although it is frustrating the amount of paperwork and non-clinical duties I have to complete. It is sometime frustrating when seen as a lesser physician than specialists, especially when I graduated cum laude from medical school and as a member of AOA, and have such a wide breadth of practice.

Did you graduate with student loans? How much & what are the interest rates?

I went to a state school, and originally took out about $170,000 to pay for my education. Interest rates were between 5.16% and 7.90% and all unsubsidized. I did receive a partial scholarship all four years. I was awarded a full ride scholarship to a different school, but elected to go take out the student loan burden to attend medical school in the same city as my husband. While I would make the same decision again, it is frustrating to think of how my financial situation would be different without this loan burden. My husband graduated medical school with a similar loan burden.

How fast (or not) are you paying them off?

I paid off one loan in medical school, a Grad PLUS loan at 7.90% interest for only $3,000 taken out my first year of medical school. I paid this off my second year, when I was able to take out an unsubsidized loan at a lower interest rate (6.55%, so only a bit improved). I have not yet paid off my loans or refinanced them, although I am in the process of refinancing at the moment now that I am an attending. Although I qualify for PSLF, I am not pursing it as it makes me too nervous. I have paid the bare minimum through income based payments throughout residency, and my loans are now over $200,000 (yikes!). However, we have paid off more than $100,000 of my husband’s loans. We knew that my loans were much more likely to qualify for forgiveness or PSLF than my husband’s, and that I would be an attending sooner (thus able to refinance), so we’ve paid anything we can toward them in residency. I am comfortable with this plan and completely trust my husband, although I understand that some may not take this approach. We plan to continue to pay his off as aggressively as possible, and hope to be done with his loans in about 18 months. We will then aggressively pay mine down, and hope to be done within 4-5 years.

Financial aspects of kids

When did you have them?

I have two kids, and a third on the way. The first was born my fourth year of medical school, and the second in residency. They are both young, and when my next child is born, I will have three children under age four.

Are you planning to fund their college expenses?

Our kids do have 529s set up, although we haven’t significantly contributed to them given our own student debt. We encourage grandparents to gift toward them instead of extra toys for birthdays and Christmas. When no longer with our own debt, we would like to fund them with enough for them to attend an in-state university.

What are your child care expenses?

We have used day care exclusively for my children. I did not feel comfortable with a nanny or spending time alone with infants, so went the daycare option. We are overall happy with our decision, although sick days and drop off/pick up times have been stressors in the past. I currently spend $1200 per child per month, which means I will soon be spending $3600 each month in childcare. This is, by far, our largest monthly expense. We also spend quite a bit more on trusted babysitters (especially college-aged family members) to help us with early morning, late evenings, nighttime, and weekend coverage. Now that I am an attending, I have the luxury of more predictable hours.

Are your kids in private or public school? What is the cost including after care if needed.

We plan to send our children to public school when they start kindergarten, as we have good public schools in our area and like our children to be exposed to diversity.

Financial aspects of marriage

Are you married?

I am married.

Did you get a pre-nuptial or post-nuptial agreement?

We got married in medical school and had no prenuptial agreement – we only had debt at the time!

Do you and your husband agree on finances?

We agree on finances, largely because I am responsible for almost everything financial in my household and my husband agrees with my decisions (and is grateful he doesn’t have to do it)!

What financial mistakes have you made?

I probably could have taken out slightly less student debt as I graduated with approximately $10,000 in my bank account. I did eventually use this to pay down student debt, but was worried about keeping enough of an emergency fund available. I contributed the maximum amount my Roth IRA since I was 16, however, I put the money in and didn’t invest it for quite a while because I was overwhelmed with the options. While I am grateful for this money, I wasted the benefits of years of compounded interest.

Have you experienced a financial catastrophe?

We have been fortunate to have avoided any financial catastrophe.

General Finances

What’s your FI (financial independence) number?

We don’t have an FI number, largely because it seems too far away at this point. We are aggressively paying down student loans, and then would like to move to a bigger (but still modest) house. I am working 80% as an attending, but would love to decrease that further to 50-60% in the future if financially able (and my department supports this!).

Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

I handle almost all the finances in our relationship. We DIY. This does result in some mistakes (such as not investing Roth IRA initially, as mentioned above). I do budget through Mint, more to track our spending. Both my husband and I are fairly frugal. We rarely spend money on entertainment, eating out, or travel. Any leftover money not used by childcare, mortgage, monthly expenses, or to replenish our savings/emergency fund goes toward loans. As we finish our training and have more control over scheduling and finances, we would love to travel more.

What is your net worth?

We do own a modest 3 bedroom home. It was purchased at the start of residency for around $175,000, as we had a dog and a monthly mortgage was cheaper than renting a house with a yard. We also knew we planned to be in the city long-term. It is currently valued at $230,000. We are hoping to pay off our student loan burden (or at least be close!) before moving to our “forever” home. I don’t plan on a new build or anything extravagant, but I do wish for a bit more space for our growing family! In addition to our student debt and mortgage, we do have one car loan. When we found out we were expecting our third, we needed something bigger than a compact sedan to accommodate three car seats! We are typically pretty opposed to financing things, but our car interest rate (0.5% for three years) is so much lower than our student loan interest rates (lowest rate 5.16% and most at 6.55%) that we used the money for the car to pay down our student loans and will both be attendings to pay off the car loan before the three years are up. I am fairly conservative and keep at least $10,000 in our emergency fund. I know I could probably get by with much less, given that we are a dual-physician household, but with young kids and a current pregnancy I don’t want to be caught surprised.

How are you saving for FI/retirement?

We both contributed to Roth IRAs maximally from age 16 until starting medical school. Neither of us contributed anything in medical school. We then contributed to our Roth IRAs maximally in residency, but no other contributions. Now that I am entering the attending world, I will have a 403(b) and 457(b). As a university employee, I get fairly generous matching starting next year (2019). We plan to maximize these contributions starting next year. The area of finances I feel most deficient in is investing. We do our investing ourselves. I admit I don’t fully understand investing/the market. Most of our money is in index funds, like the S&P 500. I would like to learn more about this in the next year to better invest my money.

Do you have insurance?

We both have term life insurance, no whole life insurance. We both have personal, own-occupation disability insurance. We have umbrella insurance through our home/car insurance company. We’ve never had to use it. We also just established a revocable trust and updated will.

Do you give to charity? If so, where and why?

We give to charity, although only about 2% of our net income. We would like to give closer to 10-15%, as soon as our loans are paid off. We currently/plan to contribute to our church, our undergraduate university, and local organizations we support.

Any parting words of wisdom?

Our financial plan largely comes from White Coat Investor and Dave Ramsey. We are financial amateurs, but we at least know where our money is going each month and can use that to cut it down to the bare minimum to allow for loan repayment. We are both so excited to be a bit more loose with our money as soon as we don’t have that over our heads!

Tell readers a fun fact about you

I took a month off between residency and starting as an attending, and it was wonderful to spend time with kids, catch up on life/adulting, and be able to read my first book for pleasure in 5 years (whoops!)

And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I loved reading Heather's story and I hope you did too. I was totally inspired about reading how she was able to take control of her and her husband's finances and get on track for financial freedom.

pregnancy, delivery and my first year with baby in tow I've learned a thing or two about the financials of having a baby as a woman physician.

You’ll need to accept the fact that you will likely make less during pregnancy, during your leave, and even after you return to work. This is due to how practices usually pay you and adjust your pay for time not seeing patients. Brace for impact.

Read my top financial tips on KevinMD.

2018 can be summed up with one word – growth.

We moved to a new city with a new baby at the end of 2017. M and I started new jobs. We are still settling into Philadelphia and it does not feel like home yet. We are renting. We were not ready to commit to buying so we renewed our lease for one more year.

After plugging in some numbers in a rent vs. buy calculator it is clear that we need to buy after our lease is up. Financially, our net worth stayed about the same despite both of us maxing out all available tax advantaged accounts (401(k)s, backdoor Roth IRAs, HSAs, funding a brokerage account at Vanguard and investing in a real estate syndication.

How? We sold M's condo in NYC and after taxes and other selling fees–we lost a good chunk of the equity. The market wasn't so hot in 2018 either. We parted ways with our financial advisor and I'll admit that since then I have not been as organized about our investments. I can't even really tell you how our investments did this year! But we continued to invest in the market and ignored what was going on. While many folks are worried about the market downturn, I see it as a sale. With Physician On FIRE and 39point6's help I did my first tax loss harvest.

Our biggest financial accomplishment was paying off my student loans in early 2018! We are debt-free. Obviously, we could not predict the market but I think we made the right choice. I admit it was somewhat anticlimactic but I think being a brand new mom in a new city had something to do with that.

Later in 2018 we had an unexpected loss of income and being debt-free and living below our means was pivotal in weathering that storm.  Jack turned 1 and has a positive net worth! He has a UTMA, ESA and a 529. He will be opening up a Roth IRA soon.

Jack turned 1 and has a positive net worth! He has a UTMA, ESA and a 529. He will be opening up a Roth IRA soon.

Miss Bonnie MD In 2018

I somehow managed to continue working on MissBonnieMD.com and be active on the various physician finance Facebook groups.

In March, I had the honor of speaking at the inaugural White Coat Investor Conference–The Physician Wellness and Financial Literacy Conference in Park City, Utah. I spoke about some of my favorite topics–outsourcing and prenups in addition to estate planning.

All the speakers and topics were fantastic. The best part of the conference was hanging out with online friends “in real life” including my podcast buddy Carrie Reynolds, Dawn Baker, Nisha Mehta, Peter Kim of Passive Income MD and his wife, Hatton1 and so forth. I had already met Physician on FIRE in NYC previously. Oh and of course I got to meet Jim Dahle! In case you missed it, you can purchase the virtual conference and watch every lecture.

During the summer I connected with some of the awesome physician podcasters at Podcast Movement in Philadelphia. I met Nii from Docs Outside The Box, David from Doctors Unbound, Taylor from The Happy Doc, Tarang from Doctor Money Matters and Ryan Gray from Med School HQ. Carrie and I attended the ChooseFI meetup and got to chat a bit with Jonathan. In September I attended FINCON and had the pleasure of hanging out with my physician finance blogger friends. We had quite a group convene in Orlando! One of my favorite parts was meeting british woman doc Nikki from The Female Money Doctor.

I left the conference totally inspired to keep working on this website and help women find financial freedom. I was featured on two podcasts last year:

I had a blast recording this podcast with Nii at FINCON in Orlando, FL. Not often do I get to “see” who I am chatting with. Nii graciously included my blog in his “Top 5 Personal Finance Blogs for Physicians” episode.

![]()

One “dream goal” came true when I got to chat with Farnoosh Torabi about my blog and finances on her So Money podcast. I love her book When She Makes More and highly recommend this book to all breadwinning women! Too bad we didn't get to connect when we were neighbors in Brooklyn! Carrie and I recorded 10 podcasts in 2018! One of them included an interview with Jim Dahle. We hope to do them more often. I wrote a Christopher Guest Post for Physician On FIRE where you can read about my favorite wines. I wrapped up the year by giving two local talks–I spoke to dermatology residents at Jefferson and young Barnard alums about personal finance. I have some big goals for Miss Bonnie MD in 2019:

- Complete redesign of the website

- Write a book

- Increase readership and traffic by 100%

- Increase revenue by 100%

I'm excited about 2019! I hope you've created some written goals to go after this year!

life and disability insurances. But do you have a will? Would your spouse and loved ones know what to do when you pass? Do they know how to access your accounts and other important documents? That's why you need a legacy binder. Death planning is, unfortunately, the high priority item that rarely gets done before your loved ones need it. It's probably due to a combination of thinking you will have plenty of time to get to it and avoiding thinking about your demise.

Start Your Legacy Binder with a Letter of Instruction

Your loved ones will reel from your death. Hopefully, you are adequately insured so they can take enough time to grieve and sort out your matters (and pay for counseling). Do you want them to be mired in tracking all your accounts, passwords, and other important paperwork? I'm guessing no. Make those logistics the easy part of dealing with your death. How? I recommend creating at the minimum a “Letter of Instruction.” This is an informal document (not the will) to guide the executor of your estate and your loved ones on important information that is in addition to your will. You can create this document yourself to ground your loved ones in all of the essentials.

What goes in a Letter of Instruction?

Make sure it includes the following information:

- Legal documents. Specify the location of all important legal documents they may need to handle your estate. These include the will (the original copy), social security card, birth certificate or passport, marriage and/or divorce papers, property deeds, automobile titles, etc.

- Financial information. Provide a list of all your financial accounts and account numbers: bank accounts, brokerages, retirement accounts.

- Passwords to your accounts. Make sure to include passwords for financial information, email, social media. I highly recommend using a password manager such as LastPass. This is what we use. In case you didn't know, Facebook allows you to name your legacy contact.

- Burial instructions. Tell your loved ones the exact details, including the name of the cemetery and plot location. Or if you desire to be cremated, be sure to include instructions as to how you want your ashes distributed. If you are a veteran, you may wish to look into being buried at a National Cemetery.

- Contacts. A list of family members (and your relationship to them–basically a family tree) and friends you would like to be notified of your death. Phone numbers and addresses are helpful in addition to email addresses.

- Policies. List all life insurance policies. Keep a copy of the policy page and the beneficiary designations. We use LastPass to store all our important policy pages.

- Tax information. Give the location of recent income tax returns and any necessary accounting information.

- Debts. Make a list of any outstanding debts.

- Professional contacts. Provide contact information for your CPA, attorney, insurance agents, etc.

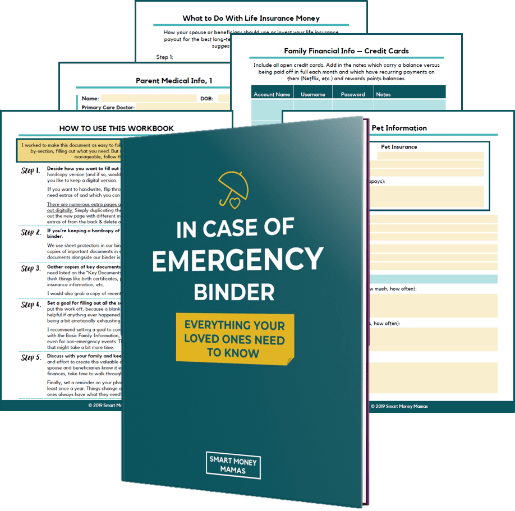

The In Case of Emergency Binder

If you're like me, you'd be more likely to do this with a fill-in-as-you-go workbook:

Chelsea of Smart Money Mama's developed this In Case of Emergency Binder (ICE) for her own family to get organized in the event of, well, an emergency. Emergencies include not only death, but a natural disaster or severe illness. I purchased her ICE binder last year and, of course, have been slow to finish this important document. Only a few weeks ago did I finally get in touch with an attorney about having our estate plan documents reviewed since we moved states over a year ago.

Make this one of your family's financial goals for 2019. And once it is completed, store this document in your estate plan binder and digitally. LastPass is not only a password manager for your whole family but it can store digital documents securely.

Final Thoughts on the Importance of a Legacy Binder

Whether you purchase a pre-made legacy binder, work with a legal professional to create one, or design your own, get it done. Not next year, not in the next six months. Make a commitment to yourself and your family to start your legacy binder right away. No one wants to think about their death, but it is a fact of life. A legacy binder protects your loved ones and should offer you the ultimate peace of mind knowing that your wishes will be respected and your loved ones will be cared for after you're gone.

Is your family prepared in the event of your untimely death? If not, get started!

This is a guest post by Letizia of Semi-Retired MD. She and her husband are both physicians and financially independent, in part, from investing in direct real estate. Their website is chock full of amazing information on how to choose the right investment property.

Investing in real estate can seem overwhelming at first. Where should I start looking for properties? How do I know if a property is a “good” deal? Who can help me through the process? Real estate investing, however, is not as difficult as it first may initially appear. You know much more about real estate investing than you think you do.

Most people have had experiences with renting and buying their own apartments and homes. These types of experiences, when combined with focused reading and supportive mentors, can make a plunge into real estate investing relatively easy and successful, even for a newbie.

In this post, I cover some of the reasons that direct-ownership of real estate investments is such an attractive way to build true wealth. I also provide you with simple guidelines for how you can take the first few steps towards becoming a successful real estate investor as you work to become financially independent. By the time you’re done reading this, you will know how to start working towards achieving financial freedom for you and your family by owning your own rental properties.

Do I need to own rental properties? Can’t I just buy real estate stocks?

There are numerous ways to invest in real estate. On one end of the scale is the most passive form of real estate investment, Real Estate Investment Trusts (REITs), which are traded much like mutual funds. REITs are followed on the scale by less-passive forms including syndications and finally by direct-ownership of rental income-producing properties.

In this article, I concentrate on the direct-ownership of rental properties. I do this because this type of real estate investing will get you to financial freedom the fastest. This is not to say you should not consider more passive forms of real estate investing on the path to becoming financially independent if it suits your risk-profile, interest and/or time restrictions. Just understand that some of the benefits of real estate investing discussed below do not apply to less-passive forms of real estate activities.

Do I have time for this?

We all know women often shoulder much of the the burden of unpaid work in the household. So why should you add the responsibility of real estate investing to that load? Why not leave it to your significant other?

First, once you learn how to successfully invest in real estate, your skills and knowledge will never be lost. You will always know how to bring in money for your family using real estate investing no matter what happens. We’ve all seen the stories of women losing their significant others, becoming sick themselves and going through horrible divorces. I, myself, have been through a divorce. And like others, I had to face the question of how I was going to support myself and my family.

As doctors, we can often fall back on our jobs when things like this happen, but wouldn’t it be better if we had our jobs, $100K in semi-passive income coming in each year from our real estate properties AND we felt confident that we could run the business (and even expand it)?

Isn’t owning rental properties a lot of work?

It’s true – direct-ownership of real estate property is not 100% passive. You have to manage the property managers; you have to manage the bookkeeper. There’s work involved with buying and selling properties. However, the amount of work for the earned income is disproportionate.

You can work a couple of hours a month and earn tens of thousands of dollars. And, over time, you can make your real estate business more and more passive by putting in place systems and people to manage most of the day-to-day issues. I’d argue it’s worth learning to make money this way so you never have to make financial decisions (or family or personal decisions) out of the fear you won’t be able to support yourself and your children.

How can real estate help me become financially independent?

In my mind, there are three main reasons you should start using real estate investment properties as a vehicle to propel yourself to financial freedom.

# 1. Wealth Building

We recently analyzed our real estate portfolio and found that we, on average, have a greater than 25% return on our real estate investments. How do we do this?

- Leverage: when you own investment property, you also make money on the bank’s loaned money as well as your own. That’s the power of using leverage.

- Cashflow: cashflow is the amount of money you make each month after all the expenses are paid. It’s the rent that actually goes into your pocket. Cashflow is the extra income source that can allow you to cut back at your clinical job or allow you to weather a particularly difficult financial month (or year).

- Equity Paydown: when you buy a property right, your renters pay down your mortgage each month, thus making you money a third way: equity paydown. Equity paydown grows each year as your mortgage payments become less interest and more principal.

- Property Appreciation: by the nature of the real estate market, your investment property will usually gain market value (appreciate) over time.

- Rent Appreciation: this is the amount that you can increase rent rates per year. It usually ranges on the order of 2-3% percent per year, which, over ten years can mean that your property’s rent increases 85%!

- Forced Appreciation: in addition to market-controlled rent appreciation, you also can increase a property’s value by improving it and then increasing rents proportionally (or disproportionately), which is called forced appreciation.

And, finally, there’s tax savings, which we will discuss more below.

#2. Control

When you put your money into REITs or the stock market or even into syndications, you lose most of your control. You cannot control if the CEO of a company is going to embezzle money. Also, you cannot control if the general partners of a syndication are going to make good financial decisions. You can only hope and trust in others to manage your money well.

In comparison, when you directly own investments, they belong to you. You can control how they are managed. You are the decision-maker. In fact, you are the CEO. You can make changes that add to the bottom line, which, in this case, ends up directly in you and your family’s pocket.

# 3. Tax Benefits

The tax benefits of direct-ownership can be substantial. While these may not initially be your primary driver to get into real estate, they really should be at the top of your list. They can significantly reduce a typical physician's tax burden.

One of the main reasons the tax advantages of owning real estate is so great is because the government allows you to depreciate at minimum 1/27th of the value of your property (the building, not the land) each year. This means that over the course of 27.5 years, your property value becomes $0 (and, remember, you’ve only paid probably 20-30% down, so you’re actually collecting depreciation on the bank’s money as well as your own). What this means in practice is that you make money through cashflow each year but it looks like you are actually losing money (paper losses).

Depreciation, when combined with the write-offs you make on improvements/rehab and the fact you don’t pay payroll taxes on your earnings, means that making $100K in real estate is equivalent of making closer to $140K at your job.

How do I even start investing?

Now that we’ve covered some of the benefits of investing in real estate, let’s tackle how you can actually get started to building your business. The first step is to educate yourself. You need to understand the basics. When you are presented with a property, you can run the numbers and know if it is a good deal. It is not a good idea to rely on others to tell you if something is a good purchase since they may have competing interests.

Read and Listen

When we first started real estate investing, we found a couple of books extremely useful. Rich Dad, Poor Dad by Robert Kiyosaki gave us the “why” of why we needed to expand beyond just relying on our 1040 incomes for the rest of our lives. Then we used books like Real Estate Millionaire Investor by Gary Keller to explore the hows. Over the years we’ve also added in podcasts, like Bigger Pockets, which give us both motivation and useful information by learning about other’s stories. [ Editor's note: Also check Paula Pant's Afford Anything podcast ]

Know the Numbers

One of the keys is when you’re educating yourself, make sure you find a good cash on cash calculator (you can get ours in our Facebook Group). That way, you you can plug the numbers in for deals you come across to determine if they meet your criteria. You should have a minimum cash on cash you are willing to accept from a property. This keeps you from buying properties that are not going to bring in money each month.

Connect with Others

Another important step is to network with other investors. By networking, you have people who can connect you with their resources and offer advice when you’re not sure what to do. Experienced investors have come across a lot of weird situations. Instead of reinventing the wheel yourself and making avoidable mistakes, why not take advantage of collective experience and knowledge and help yourself grow faster with less risk?

You can find investors in a variety of ways. You might try any of these:

- Connect at meetups.

- Join local Facebook groups such as REI MD.

- Read real estate investment-focused blogs.

Build your Team

Another key step is to find yourself an investment real estate agent. This is not just any real estate agent. Instead, find someone who specializes in working with investors and who ideally owns his or her own investment properties.

In addition to finding you deals, an investor agent should be able to help you build the rest of your team like your property manager and your general contractor, since he/she has used and vetted these same people for his/her properties.

Harness the Power of Women

Now, I know I’m biased here, but I do believe that women are uniquely positioned to be successful in real estate investing. Many of us run our family’s finances. We organize the details of our family’s schedules. Plus, we do all the planning and packing when we go on trips. We manage a lot of relationships. And all of us are awesome at multitasking.

We bring all of these skills to the table when we enter the market as real estate investors looking to become financially independent. The key is just to get started in educating yourself and building your team so that you can work towards building financial independence for yourself and your family today.

Want to learn more?

Explore our blog at Semi-Retired MD or join our facebook group.

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – The Frugal Physician!

Tell us about yourself:

Hello! Many thanks to Miss Bonnie for having me on here. Like many of you, I’m a multitasking, sometimes malwired machine that runs on caffeine. You can call me… The Frugal Physician (cue theme music). I’m mommy to two toddler boys, wife to my trophy husband (he loves it when I call him that), blogger at www.thefrugalphysician.com, and primary care physician trained in internal medicine. I dream of one day owning a jazz club and crooning at the piano in fancy dresses. They won’t be able to kick me out because I’ll own the place! And, I’m banning tomatoes. Anyway, until then, I’m focusing on being frugal and paying off debt. I live in Upstate New York (also known as “not the city”). I’m in Internal Medicine. So basically, I’m Dr. House…minus the cane and the opioid addiction. I started off in Hospital medicine and then switched to primary care. You’re going to think I’m nuts, but I LOVE primary care. I love being the first diagnostician my patients see and I love building relationships with my patients.Are you a resident or attending?

I’m the boss, baby. Not really, I’m employed. I’m an attending 3 years out of residency.Did you graduate with student loans? How much & what are the interest rates?

I graduated med school with $191k in student loans but by the end of residency they had grown to $237k, despite the $25k of payments I made in residency. I found myself on the wrong side of 6-8% compounding interest when $18k of interest compounded as I switched to standard repayment as an attending. So frustrating!How fast (or not) are you paying them off?

Oh yeah, I’m burning through them. First I refinanced with Sofi. This year, I’ve paid about $120k in 9 months towards the blasted student loans. Why? Because student loans weigh down my soul and crush my happiness. And, I did the math. If I put everything I’ve got towards the loans and burn through them, I can still catch up on investing by the end of 10 years. See my post “Counting Macaroni’s.” My goal is to buy my freedom! Once the student loans are gone and I have a good stash of savings, I really feel like I can be a better doctor. I can advocate for my patients and for what I think is right without fear of not being able to feed and clothe my kids if I lose my job. My dream is to one day start a non-profit, cash only clinic with a graded pricing scale based on income.Financial aspects of kids

When did you have them?

At the very end of residency and in second year as attending. Wouldn’t recommend that. In hindsight, having them both in residency would have been better. Being a nursing, sleep deprived new attending blows. We have a lot more protections in residency as far as benefits and work conditions go.Are you planning to fund their college expenses?

Yes, once I’ve paid for my schooling expenses. Right now, they have regular brokerage accounts for the money they get for birthdays, etc. I’ll roll that into 529’s once they meet the minimum required for the state.What are your child care expenses?

$2200 a month for daycare … barf. Still going.Are your kids in private or public school? What is the cost including after care if needed.

We’re going public. Free school! New York taxes sucks but they pay for nice schools.

Financial aspects of marriage

Are you married?

Married to a studmuffin.Did you get a pre-nuptial or post-nuptial agreement?

No, wasn’t smart enough to think of that. I was a broke resident not Jay-Z, so my head just wasn’t there, you know?Do you and your husband agree on finances?

Mr. Frugal Physician was always on board with the idea of achieving financial independence. Agreeing on deflating our lifestyle and increasing frugality took some time to achieve. Key to our success are monthly budget dates, where we can realign our goals and our spending habits.Does your spouse stay at home?

No. He did that for two years and that didn’t work for us. He is a lot happier working. Staying home is a lot of work!Are you the breadwinner?

Used to be for the two years Mr. Frugal Physician stayed at home, took care of our baby, and worked on his masters. It was tough.Financial Mistakes

What financial mistakes have you made?

Oh boy where do I start. Wish I had started a Roth IRA in college when I was working 3 jobs. Right out of residency, I inflated my lifestyle to my attending salary, which was a big mistake. We reversed course and deflated the lifestyle within two years. More about this on my blog.Have you experienced a financial catastrophe?

Yes, our house flooded with Hurricane Irma. Flood insurance doesn’t cover everything you might think. Biggest lessons: read the insurance policy and talk to insurance provider before making any changes to areas of the house that might flood. Keep a written record of all communications with the insurance company.

General Finances

What’s your FI (financial independence) number?

$2.5-3 mil. Calculated by using the 4% rule: Yearly expense x 25. I don’t plan on retiring when I reach FI, though. Being idle is not my forte. I just want the option and the freedom.Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

I do. We met with a couple of financial advisors, but I really wanted to learn how to do it. I’ve found DIY to be much better. I get much better returns than my financial advisor just investing in low cost index funds.What is your net worth?

About $165k including home equity. Up from the negative $100k or so just a couple of years ago.How are you saving for FI/retirement?

IRA’s, 401k’s, HSA. But currently, most of our extra money is going towards paying down student loans as fast as possible. Asset allocation is 80:20 stocks to bonds. Plan to get into real estate more in the future.Biggest financial failure/regret:

Just wish I had started saving earlier.One thing you wish you knew:

That I didn’t have to finance my lifestyle in medical school! Wish I had been more frugal while in school and had taken out less debt.Do you have (long term) disability insurance? Life insurance? Umbrella?

Yes to allHave you had to use (long term) disability insurance?

Thankfully, no.Do you give to charity? If so, where and why?

Yes! Giving brings me a lot of joy. Since we don’t have extra money right now, we donate our time. My husband and I volunteer to cook meals for the Ronald McDonald House. We did a lot of fundraising this year for the Leukemia and Lymphoma Society.Any parting words of wisdom?

Just spend less than you earn. Invest the rest. Read J. L. Collins’ “Simple Path To Wealth.” Plug into the financial independence community and you will learn a lot!Tell readers a fun/random fact about you:

I used to have an elephant mow my lawn! I’m a first generation immigrant. In India, we had an elephant that lived with her caretaker in our neighborhood. Her name was Jamuna. She would come around and give us rides. My parents would let the grass grow long enough for her to eat and then let her have at it!And finally, where can people connect with you?

Come subscribe to The Frugal Physician at www.thefrugalphysician.com, follow me on Twitter @FrugalPhysician!And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I love how The Frugal Physician is crushing her debt at lightning speed. Go check her out! ]]>

Life Hacks post. She blogs at PracticeBalance.com about finding balance as a physician mom. She and her husband are financially independent. You can read her interview here. The other day, my 2 year old daughter asked, “Who gave us this house?” We both paused and looked at each other. “Um… No one. We bought it with our own money that we made ourselves.” This is the first time we had talked to her about anything related to money, and I’m sure it won’t be the last. As she grows up, she’ll no doubt deal with the marketing of products directly to her, comparisons to friends, cases of the “I wanna’s”… then ultimately management of her own earnings and debts.

Always creating and learning

Unlike some families where money is a taboo subject, we hope to have many money conversations with our daughter as she matures, because financial responsibility is very important in our family. We’ve worked hard over our adult years to become financially independent and free from any debt or mortgage, which has allowed us to both work part time. When I was a young girl, I never felt that my family was in a state of lack. But I also never grasped the mathematics side of money, the finiteness of it. That all changed when I became a mother. Although my husband had been equating money with life energy for many years at that point, I didn’t see it until I had this being in front of me that I wanted to spend all my time with. I had spent years, tears, money, and life energy to have her (due to infertility), yet she was priceless. Any time at work was suddenly time away from her.

One of the lessons I really want to teach my daughter is the idea of value. Value is relative and individual, as one person’s prized possession can be another’s throw-away item. Likewise, the way we prefer to spend our time (which ultimately equates to money) can vary drastically from person to person. I cringe when I hear people use the words, “We can’t afford it.” Kind of like saying, “I can’t eat that cupcake” or “I don’t have time to do ______”, it’s rarely true in a literal sense. You can if you want to, but you choose not to, for whatever reason. It’s a mistake made often by people in all financial situations, both wealthy and poor.

What harm is done in saying “we can’t”? It sets a tone of scarcity vs. abundance. The scarcity mindset keeps us from feeling we have choices or control over our financial situation. It places issues in a negative light, such that we make decisions out of fear and compare ourselves to others. On the flip side, being valueist means that we see the potential abundance in things. We make decisions from a place of optimism, because again, anyone can afford anything they inherently value.

Taking time to find the rainbows

Affording anything, however, must come with financial sacrifice in other areas of our lives. We’ve all seen examples of people driving around in very fancy cars despite meager earnings. I’ve been to third world countries where a family shack contains a large screen TV. Everything we buy is a choice and is conversely a choice in the opposite realm (against saving or spending on something else). How much is an extra hour a day with your child worth to you? Is it worth not having a cleaning lady, taking a 30% pay cut, moving to a smaller house? In addition, there are degrees of choice here; you can choose to NOT buy the nicest item you can afford. The common belief that everyone buys the nicest things “they can afford” leads to a false evaluation of success based on material goods.

Of all the things I value, time with my family sits at the top of the list. I hope someday my daughter will understand this concept when she wants me to buy her something that I choose not to buy. The best thing we can do is to live our lives in alignment with our respective values and provide an example for our children.

Don't miss out on future blog content, join my email list!

This past year has been an amazing year of growth and change for me. It left me realizing I had to find a way to optimize my life.

In one year, I became a mom, I moved to support my fiancé's career and to get our family into a better place financially. I left my academic practice in New York and joined a private practice. Moving to a new city with a newborn in tow means leaving all your friends behind. Meeting new friends as a new mom is challenging.

I’ve learned a lot about myself. For one thing, I’ve learned to be honest with myself. I’ve also learned that I can’t do everything. Being a mom, a physician, running the household, and trying to run a side business – well that’s more than enough to make anyone go a little crazy.

I spent a lot of time and trial and error trying to optimize my life. One mantra I really took to heart is that time is our most precious resource. It truly is.

Time Is Our Most Precious Resource

How I Optimize My Life

So I’d like to share my 5 life hacks and tips I’ve implemented to optimize my life so that I am freed up to spend time where I want.

# 1. Outsource _________ .

I love to cook. However, in the immediate postpartum and beyond, I found that I really couldn’t find time to cook. In fact, I found it it quite stressful to think about meal planning. I went through several iterations of how to get help in this area initially. Truthfully, I felt a little guilty for not wanting to cook for my family (and I know how to cook so it wasn't a skill issue).

I had to give myself permission to spend on something that would make my life easier. It may not be forever.

My mother took care of me and baby Jack until he was six and half months old. Picture home cooked Korean food every day while I could focus on breastfeeding and recovering from childbirth. Once that ended and I was back at work, I found it challenging to feed myself and my fiancé good food. I initially used a prepared meal service that cooked all the food and delivered it. I would just need to heat them up in the oven or microwave. It was not the cheapest option but it filled a need, so we did that for a month or two.

When I felt that I could devote more time to this area I then turned to meal planning. We have an instant pot. In case you’re not familiar – how could you not know about this already? – it is an electric pressure cooker. You can make “dump and cook” meals. I still found it challenging to actually plan meals for the week and finish up all the food we purchased. You can only have so many taco nights ….

I ran out of steam in the meal planning area. Our current situation is that we now subscribe to a meal prep service such as Sun Basket and Marley Spoon (our current favorites). We usually choose the paleo-like options and get 3 meal kits a week. This combined with hack #2 below has been a killer combination for us.

# 2. Hire A Part-Time Wife

Why do women physician moms think they have do everything? Most of us work full time in our demanding jobs as physicians then come home to immediately transition to being mom and housewife. Combine that with a maybe not so equal partner (in terms of division of labor)- this is surely a recipe for lots of unhappiness. Thankfully, Matt likes to cook and do laundry (!). But the truth of the matter is we both work, so this is an area that we could use some help.

We have a cleaning service that comes every two weeks to do a thorough cleaning of our apartment. That was a no brainer.

But the best hack I have found to date in this area is who I called my part-time wife. She is a part-time nanny for another local physician mom. She comes to our place 2 to 3 times a week. When she comes by, she organizes & tidies up (puts away all of Jack's toys, folds blankets), unloads the dishwasher, wipes down counter tops, removes garbage & boxes, waters plants, and does tasks like get the coffee pot ready for the next morning. Additionally, she’ll do the laundry and fold it and put it away. Magic.

We come home to a clean and tidy home. It is mentally calming and relaxing to come home to this!

# 3. Take Care Of Your Body

Like many moms, I gained a little too much weight while I was pregnant. And my body was a bit of a wreck after childbirth. It was also in the middle of northeast winter when Jack was a newborn. I have a gym downstairs in my building. But I know myself and know that I work best in a class where someone is literally telling me what to do. Previously, I used to work out at Orange Theory in New York – when it was across the street.

I hired a personal trainer. I worked with him 1-2 times a week over several months. Eventually, I got back my strength and core training with Mike. Hiring Mike was probably one of the best decisions I ever made for myself. (And if you’re in the Philly area you should definitely look him up!).

# 4. Clear Your Mind

I don't know about you, but my mind is always buzzing with ideas and thoughts. And my to do list. And that patient I saw yesterday. It's enough to drive most people mad.

I started using Headspace to start my day. It's a phone app that walks you through a guided meditation. Also, I started using Asana to organize my business and my personal life. Think bullet journal in a digital format. I tried using a traditional bullet journal but it just didn't work for me.

# 5. Invest in YOU

And finally, my latest and what I consider my best gift to myself is working with a coach. Life coaches work with you to remove the barriers to your best authentic self. Our dreams and reality are limited by our thoughts. I guess you could call Sunny my thought coach. She's also my business coach. She points out when my thoughts aren’t serving me and encourages me to transform them into something that will call me into action. My first few calls with her were all about me feeling completely overwhelmed with everything on my plate. I mean there’s just no time to do all the things I want to do and that’s just the truth!

And finally, my latest and what I consider my best gift to myself is working with a coach. Life coaches work with you to remove the barriers to your best authentic self. Our dreams and reality are limited by our thoughts. I guess you could call Sunny my thought coach. She's also my business coach. She points out when my thoughts aren’t serving me and encourages me to transform them into something that will call me into action. My first few calls with her were all about me feeling completely overwhelmed with everything on my plate. I mean there’s just no time to do all the things I want to do and that’s just the truth!

Well clearly it's not. It's just a thought. She doesn't let me indulge in thoughts that don't serve me. Although sometimes I really want to.

Final Thoughts on How I Optimize My Life

Using these five hacks has really helped me optimize my life despite all of the new challenges and commitments I've taken on. As time changes, I know that I'll continue to rely on these same strategies and come up with new ones. If you find yourself looking to get more from your day, week, and month, try out one of these tips today.

What life hack or tip have you implemented to free up your free time? Comment below!

Don't miss out on future blog content, join my email list!]]>

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]