Bonnie Koo

If you're interested in learning more about finances and don't have the time or interest to wade through books, blogs, and online forums then this course is for you. I wish this course was available when I first got interested a few years ago. I had to read several books, read a ton of blog articles, and post a lot of questions online to learn what I know now.

When you finish the course, you’ll feel confident that:

If you're interested in learning more about finances and don't have the time or interest to wade through books, blogs, and online forums then this course is for you. I wish this course was available when I first got interested a few years ago. I had to read several books, read a ton of blog articles, and post a lot of questions online to learn what I know now.

When you finish the course, you’ll feel confident that:

- You have all the insurance you need at the best possible price and none of the insurance you don’t need

- You are managing your student loans the right way, maximizing the benefits of government programs, minimizing interest paid, and getting out of debt as soon as possible

- You are either capable of managing your investments yourself, or you are paying a competent advisor a fair price to do it for you

- You are saving enough money to reach your goals and can spend the rest on whatever you like without feeling guilty

- You aren’t paying any more taxes than you need to

- Your children and your assets will be taken care of if something should happen to you

- Your assets are protected from lawsuits as much as possible with a simple, straightforward, and inexpensive plan

- You have a written plan to follow that will guarantee your financial success

Click here to find out more details and to purchase with code: MATCHDAY18 for 15% off

As an affiliate for this course (the course is the same cost to you regardless of who you purchase from) I was able to take the course for free. It is quite comprehensive and I cannot think of a more time efficient way to learn this stuff. Have you taken the course? Comment below! ]]>

push presents are a thing. And it turns out that I got the best push present ever!

About a year ago, M asked me to marry him and promised to keep our net worth positive. At that time, I was dragging us down with my student loans.

Well, not anymore! M paid them off!

Yup, I no longer have student loans. Happy dance in order:

And, we are now officially DEBT FREE !!!!!!!!!!!!

The Case to Wait to Pay Off Debt

I hear people say all the time that you don't “need” to pay off low interest debt quickly. I see their point and I wasn't planning on paying off these loans for another 3 years. Right out of residency, I favored maxing out my tax advantaged retirement accounts over making extra payments towards my student loans.

Why No Debt Is the Best Push Present Ever

Despite this argument, having no debt really feels fantastic. And it comes with some really significant perks too.

Being debt free means:

- No extra monthly payments

- A lower monthly operating budget

- Any extra money we get goes to us, not debt

Final Thoughts on Being Debt Free

Existing loans and taking on new ones (mortgage, car loans, etc) give you the illusion that you can afford something you actually can't.

Like 0% interest car loans – trust me, they aren't doing that to be nice to you. They know you will buy a more expensive car on credit even if you aren't paying interest. After all, it's just another monthly payment, right?

Couples who pay off debt together stay together. Of course, not every couple might have the means or the desire to pay off debt in one fell swoop like this. The most important thing is to make sure that you're on the same page financially, or at least taking steps to get there. Having solid financial footing before bringing a baby into the world truly feels like the best push present.

2018 is well underway. Last year, M and I had a good amount of tax advantaged retirement “pots” available to us along with some employer match and contributions:

- My 403(b) + generous employer match + contribution

- My 457(b)

- My cash balance plan

- My backdoor Roth IRA

- My solo-401(k)

- His 403(b)

- His Roth IRA

- His solo-401(k)

- My 401(k) + employer match

- My solo-401(k)

- My backdoor Roth IRA

- My HSA

- His 401(k) + employer match

- His Roth IRA (may need to backdoor it this year)

- His family HSA

- Our taxable account

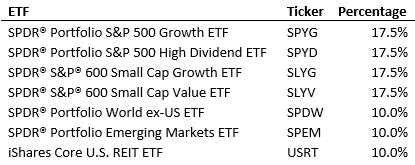

- 68% US stocks

- 17% Large cap growth, 17% Large cap value

- 17% Small cap growth, 17% Small cap value

- 24% International stocks

- 12% Large cap developed countries

- 12% Diversified emerging markets

- 8% US REITs

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

Having a baby and becoming a mom is stressful. There's no denying that. Planning for a maternity leave can be stressful, too. If you're expecting your first baby (or even a second or a third!), you might be wondering what a longer maternity leave looks like. Here's how I spent (and funded!) 16 weeks of maternity leave.

A Word About Stress

Everyone handles stress differently. No two births are the same. There are so many variables when it comes to maternity leaves.

For me, well, my leave was pretty stressful.

There was moving and almost dying along the way. At some point (OK, multiple points), I was overwhelmed and probably met criteria for postpartum anxiety. I spoke to a psychiatrist friend who pointed out that I pretty much experienced all the top life stressors except death of a loved one (and let's keep it that way!) within a 4 month period:

- New baby (especially the first one)

- Moving

- New Job

- Serious illness

She also pointed out that what's especially hard for new mothers is that no one is taking care of us. We are always taking care of baby (and spouse).

A Look at 16 Weeks of Maternity Leave

I feel lucky that my mother lives nearby enough and has been with us most weeks.

Breakfast of Champions – home cooked Korean food

So, I decided to give myself a pass on pretty much everything. For me, that meant a lot of stopping.

I stopped worrying about…

- Posting consistently on this blog.

- My new postpartum figure (well, kind of).

- Every single bit of what I was eating.

- Spending too much especially if it made my life easier during this time.

I am still trying to worry less about the not fully unpacked apartment.

Oh, and I finally figured out the biggest fallacy of “maternity leave” — nothing gets done despite not “going to work.”

Funding a Longer Maternity Leave

Throughout my leave, I was often asked how are we able to afford taking 16 weeks of mostly unpaid leave.

Let's back up and actually look at my leave. I took 16 weeks of leave, and it was only very partially paid. 6 weeks paid at my old base salary was all I got.

So how did we swing the full 16 weeks of maternity leave?

The answer is simple: We lived below our means, and we saved for it. Remember, you have about 9 months to save for maternity leave!

Let's go back to the idea of living below our means. In other words, we do not need our whole paycheck to get by. While I was pregnant, I stopped making extra payments to loans in favor of saving for this time.

Then, I had a cushion to pay for my maternity leave.

It definitely didn't feel good to watch my checking account balance only decrease during my leave, but seeing his face daily more than made up for it.

What are you looking at?

Final Thoughts on 16 Weeks of Maternity Leave

Isn't this what it's all about, Moms? I hope everyone about to have a baby can have the freedom to spend more than the typical 4-6 weeks of doctor maternity leave.

Look hard at your budget while your expecting, and see what you can do to save a bit extra. Even if you can't fund 16 weeks of leave, anything extra counts. You won't regret it.

What do you think of funding a longer leave? Comment below!]]>

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – Leah.

Tell us about yourself:

People have a binary response to what I do, either “wow” or “eww”; there is no in between. Thankfully I have a wonderful partner in life who finds this binary response as funny as I do. I'm a forensic pathologist. What is not binary is that nearly everyone says that I am not what they had envisioned as a forensic pathologist, and that they would never have guessed what I do. I'm not weird, (by most standards), have a normal family life with my second husband, one girl, one boy, a dog, and a cat. Overall pretty balanced life. Of course, like nearly everybody else, it didn't start out that way. Most people consider me “Hispanic” although for me it wasn't a label I applied to myself, nor did I consider myself a “minority” until I moved to the “deep South”. It's all relative. I speak English and Spanish interchangeably, my baseball team was the Chicago Cubs before they were cool, and my favorite dessert is apple pie. Currently I live in a relatively expensive suburb to a coastal town thoughtfully referred by some locals as “Mount Plastic”. You get the idea. But when you are moving from the Caribbean to the mainland US and your only reference is the quality of the school zones as graded by the “internet”, that's where you end up. In an engineered neighborhood with cookie cutter homes and the best public school zones in town. No regrets, it was a great choice, and the neighbors are fantastic. I am absolutely certain I ended up in the right specialty, but it was entirely a happy accident thanks to not matching and the post match “scramble”, now “soap?”. I repeat, I did not plan to become a Forensic Pathologist (!), and it has been the best thing that could have happened to me. I was the happiest intern for the first 3 months of my pathology residency when I did my required autopsy rotations; I remember saying I could not believe they were paying me to do autopsies. They still are. I know I can do something else (PM &R and Gyn come to mind), but given the choice and knowing what I know now, I would never change my specialty. I love my work life balance, my open book specialty, being able to take time off whenever I want to participate in last minute school things, and all the interactions with amazing people that make up the law enforcement and death investigation systems, judges and juries. I honestly wish that more medical students knew about the fun side of pathology as a specialty, but if they were like me in medical school, it never has crossed their mind. Now, as an attending, 10 years out of residency, I make sure to reach out to as many medical students as I can to show them how fun Forensic Pathology can be.

Did you graduate with student loans? How much & what are the interest rates?

Again, I was lucky to go to subsidized state school – I graduated with $60K in loans. But in reality I had no idea what to do with medical school loans and would have left them as is. But my best friend told me right after med school (2003) I should consolidate and fix my interest rate because rates were historically low, so I did. It's good to listen to other people who are more financially savvy than us, even though she and I have vastly different financial habits and lifestyles. So my loans got converted to a 20 years fixed at 3.25% and I'm kicking myself because I possibly could have paid them off by now. The monthly payment is so low, that I have just been lazy I guess. Life happens and getting rid of a $200 payment is not high priority.Financial aspects of kids

When did you have them?

I had my daughter during 3rd year of medical school. I had planned for 4th year, but oh well, first year anniversary celebration. I was trying to avoid infertility issues that plagued my mother by having at least 1 kid before 30. My daughter ‘s arrival caused a 1 year delay in my medical school graduation date and my ex-husbands true colors to flourish as a sucky dad and partner. Divorced when she was 4. Met my second husband immediately, and my second child was born 8 1/2 years after my first. He was 6 weeks old when we moved permanently to the mainland. Today they are 7 and almost 16 years old. When we relocated, we moved to the expensive part of town of mainland US so kids could go to good public schools- saved me the 10K/year I was paying before I moved (for 1 kid), and now I happily pay my taxes to the county in exchange for public schools that have caring teachers. Day care/school for my youngest was transitorily expensive at $1400/month for 1 kid, year round, starting at 2 1/2 years, but that was only 3 years and now he's in public school. We tried a nanny briefly when our son was a baby but she moved away after a couple of months and my husband just sucked it up big time until the baby went to preschool and took care of him, even taking him on business trips. The economic relief came when he graduated to kindergarten. But now I face the other end of the child expense spectrum. My eldest is 1 year away from an early high school graduation and college, and her college fund is woefully underfunded. I feel it's too late, much too late to fund anything significant for her at this point, so we will approach this with a prayer for a good scholarship and thankfulness for her 4.6 weighted GPA. Learning from my mistakes, and in a much better position financially than when my daughter was growing up, I will fund my son's 529 much better; he is 10 years away from high school graduation so I should have time to do better. Didn't have a third kid because we could not afford to give it what we want to give our children time wise. Sometimes I'm wistful because I would have loved another child for my second husband, but he's clear he didn't want any more of the responsibility associated to their social agendas. Because he is the primary caretaking parent due to his work from home flexibility, he got his wish. I had previously decided no kids after 40 due to genetic risks, so by now at almost 42 it's no longer an option.Financial aspects of marriage

Are you married?

To marry or not to marry, that is the question. Most people do not know my second husband and I are not technically married, and this includes my youngest son. Socially we are. Legally, somewhere in the gray zone because this state recognizes common law marriage and it’s been 11 years, but if you get down to details, not technically married. Why? Taxes. Different tax habits (he files late, I file early), different tax bases (mainland US for me vs. back home for him), and the marriage penalty of higher taxes if we do. We have a few assets from before marriage that we keep separate and legally we would have to write a simple prenup for the old assets. Plus, having been really married before, divorce can be expensive, even when you share nothing but debt. My second husband and I do not have the same financial views or habits, and it took some balancing and compromise to get to a household budget. I'm a saver, he's a spender so he now gets to release his spending beast at the supermarket and costco instead of home depot and best buy. I splurge once a year during the back to school. I defer money (the maximum allowed contributions) into the retirement plans so we don't see that money; like it never existed. We make do with what's left over of the paycheck even if its a bit tight.Are you the breadwinner?

I'm the primary breadwinner. My husband makes enough to pay for dinner once in a while and pay for his IT business things back home. We have access to each other's personal accounts, but what is his is his, and what is mine is ours; honestly I don't have the time to do all the household things he does. He controls his IT business account and I have a personal account back home for receiving (or not) theoretical child support. That being said I monitor the spending closely for things that might not belong to us. I've seen horrific financial issues with identity theft so we are extremely vigilant that every single transaction is ours.Have you experienced a financial catastrophe?

Financial catastrophes are divorce, illness, or loss of a job (when your field is so specific that you aren't cross marketable locally). The more you have, the more expensive the catastrophe is, because of the higher holding costs associated to simply keeping a home, cars, boats, kids in private schools, insurance. The lower you live below your means, the easier it is to weather the unforeseen. Public school is free, no job no problem. Paid off cars only have registration/property tax: example my 1999 Lexus SUV with high mileage has a $6.00 yearly registration. I'm pretty sure I can scrounge this up from the change bucket. My newest “splurge” in a vehicle is a 2005 Lexus SUV, 12 years old, $56 yearly registration. Of course I can afford a new one, but why? This one takes me from point A to B exactly the same as a new one, and it still has all the bells and whistles. Having a safety net is important, the best one is the “emergency fund” and the second one is “enough insurance”. Rich family member works too. Keep your house payment affordable, your car payments paid off or affordable, and don't spend to keep up with the Joneses because the Joneses aren't going to pay your bills when TSHT Fan. That being said, I am not “loan averse” or debt averse. Long term holdings – house, car and education- are best paid off in the long run with future earnings that have less value. Loans are leverage, protect your credit and this will help you weather minor unforeseens and help you get ahead.

General Finances

What’s your FI (financial independence) number?

Our financial independence number is a moving target and will end up being when we both “had enough” of full time work – as long as primary house and vehicles are paid off and kids are out of college (around 2030). I will be 55 and hubby 58. We are thrifty to the extreme. Sale and clearance are our favorite words, along with consignment and second hand. We take used toys and kids clothes to second hand stores for purchase, sell used things on craigslist, save all the spare change into the emergency fund and have taught the kids to save their money.Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

We have a financial advisor that we like on a personal level. He did get us the fixed rate term life insurance we needed, advised us to open our own self managed 529 accounts (instead of advisor led), and uses computer software to model where we are at the time and what the projections will be. He sees us for free. I had to beg him to open a small IRA for me that I contribute to yearly, and don't mind paying him advisor fees on that amount since he is so available to us for answering all sorts of questions for free. Going with my husband was eye opening for the both of us, turned out we were much better off than we thought but still a long way from where we want to be.What is your net worth?

It may seem crazy but I don't want to know my net worth. Market value of assets fluctuates, as does retirement account values. My FA calculates it periodically but we don't pay attention to it much because it will be different in 6 months. We have grown it exponentially and not linearly as expected, mostly with self discipline and luck in real estate investments.How are you saving for FI/retirement?

We started late and have to catch up. We save a lot into retirement – basically every penny that we don't spend on basic living, because I'm saving for my husband and I, and you can technically finance the kids education better than your own retirement.One thing you wish you knew:

I don't really have financial failures or regrets other than getting roped into inheriting my grandparents timeshare. Say no to timeshares! We used it a few times and but bottom line it ends up being 10 times more expensive than paying for it per use. Right now I'm paying an agency thousands of dollars to get rid of it. Once I'm done it will be filed under “learning experience”.What does FI/retirement mean to you? What does it look like?

We are not “do nothing in retirement” people, so even in retirement we would both work to keep busy, just not out of financial necessity. We both have marketable skills for easy sideline jobs.Do you give to charity? If so, where and why?

What we can't sell, we donate. We are possibly the odd ones out in the “Joneses” club around here, on one hand living in a house worth now over half a million dollars yet quietly picking up what our neighbors toss out on the curb and donating it. There is no reason for a bike to end up in the landfill when a child somewhere else can use it. We also donate directly to the schools and to animal rescue programs, because what goes around comes around. We are truly blessed.Any parting words of wisdom?

To summarize, some debt is good (house in good neighborhood/school zone), some debt is bad (credit cards), safeguard your credit, live well below your means to be able to survive whatever life throws at you, have safety nets in place, prioritize retirement over education savings, don't be wasteful, and don't forget to count your blessings and be thankful. As Lennon said, Life is what happens while you're busy making other plans.And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I loved reading Leah's story and I hope you did too.]]>

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician heroine – Sharon .

Tell us about yourself:

Hi! My name is “Sharon”. I am a pediatric subspecialist in a private practice. I like my job, but at times I do feel tired. I feel like I wasn’t as exposed to other specialties in medical school that I might have pursued (like radiology). I am currently married and have one son. I love to draw and cook. I am Hispanic. I live in Central Florida, which in my opinion is very reasonable in terms of cost of living. I am currently an attending 6 years out of fellowship.Did you graduate with student loans? How much & what are the interest rates?

I graduated with student loans but I was very fortunate to go to a medical school in my native country which was more affordable than in the US. I went to a public university. My loan interest is 2.65%. My loans totaled $72K. I still owe about $16K. I was pretty aggressive initially paying off the higher interest loans and I am planning to pay them off completely this year.Financial aspects of kids

When did you have them?

I had my son 2 years ago, as an attending.Are you planning to fund their college expenses?

My son is 2 years old. I have a 529 through the state of Utah. I will help him as much as I can, but my goal right now is to have about $150K for college.What are your child care expenses?

My son has been in daycare since he was 12 weeks old. It was not an easy decision but I didn’t feel comfortable having a stranger in my home all day with my baby. His daycare is very good, close to my office and has cameras that I can monitor.Financial aspects of marriage

Are you married?

Yes I am married.Did you get a pre-nuptial or post-nuptial agreement?

Maybe it’s a cultural thing? Not common in our culture. I guess I would've like to have one.Do you and your husband agree on finances?

I am the primary breadwinner and I am the one that makes all of the financial decisions and plans for the future. He just agrees with everything I do. I make about 3 times what he makes. He realizes that and we have found that keeping our accounts separate works best for us.Have you experienced a financial catastrophe?

No, thank god!

General Finances

What’s your FI (financial independence) number?

I don’t have a number, but I do have a game plan. I want to pay off my medical school loans (hopefully this year), followed by aggressively paying off my mortgage (hopefully pay it off in 10-12 years).Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

I handle the finances. To be perfectly honest, my husband shows no interest in learning about our finances, so I took complete control. I had a financial advisor and fired her after everything I have learned reading on my own.What is your net worth?

Minus $90,000.How are you saving for FI/retirement?

I am maxing out my 401K and I am in the process of doing a backdoor Roth. Next step – Index funds.One thing you wish you knew:

More about investing.Biggest financial failure/regret:

Not getting disability insurance as a resident.Do you have insurance?

Yes, we have term life and umbrella insurance.What does FI/retirement mean to you? What does it look like?

I want to be comfortable and still relatively young (late 50’s early 60’s).Do you give to charity? If so, where and why?

Yes, to a genetic syndrome foundation about $500 a year.Any parting words of wisdom?

Read White Coat Investor, follow Bonnie’s blog, follow Bogleheads and ask lots of questions!And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I enjoyed reading Sharon's story and I hope you did too.]]>

2017 was amazing year – personally and financially. In 2016, I ended with a negative net worth of -$92,000. Pretty typical for about a year after residency.

“I” became “We” in 2017 – We got engaged and had a baby. We also signed wills, power of attorneys, and health care proxies.

We ended 2017 with a positive net worth of > $500,000. This includes equity in a home. I still have those darn student loans – for now.

Our savings rate towards FI in 2017: 27% of gross income in the form of maxing out our retirement accounts, additional cash savings, extra payments towards my student loans and we paid off our car loan. I did not include employer match and contributions. Not too shabby!

What were my goals in 2016 and how did I do?

- Cross over into positive net worth – check!

- Knock out 50K of student loans (this is in addition to the min. payments) – close! I paid about $42,000 towards student loans in 2017.

- Max out all available tax advantaged accounts ($47K, not including employer contributions) – check!

- Start a taxable account – This didn't happen. Although I did contribute about $8,000 as after-tax non-Roth contributions towards a Mega Backdoor Roth IRA – even better than a taxable account!

How did your net worth grow in 2017?

Happy New Year! I hope everyone had a fun and healthy holiday season. What a busy past few months – personally and financially – giving birth, being hospitalized, being on maternity leave and moving are a lot to deal with! With every turn of the year is an opportunity to reflect on what worked and didn't work the year before and to create some new goals. First, let's discuss how to create goals. I am always surprised how most goals are vague – “lose weight” or “learn more about finances.” These are great goals. But they aren't specific and not very measureable. You may be familiar with SMART goals:

- Specific

- Measureable

- Achievable

- Time-bound

- 84% of the entire class had set no goals at all

- 13% of the class had set written goals but had no concrete plans

- 3% of the class had both written goals and concrete plans

So the above two goals reframed:

So the above two goals reframed:

- “Lose weight” is now “I will lose 5 lbs by 2/1/18.” The plan: going to yoga classes 2x a week and running 2x a week.

- “Learn more about finances” is now “I will read The White Coat Investor book and The Millionaire Next Door by April 30, 2018.”

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – “Hatton1” .

Tell us about yourself:

I call myself “Hatton1” on the White Coat Investor and Physician On Fire blogs. I am 60 and in the process of getting divorced as I write this. I live in the deep South in a low COL town. I actually grew up in the town I live in and have family here. I am an OB/GYN. I did OB 26 years. I went through one malpractice trial and won the case. I am doing just GYN 3 days per week with essentially no call. I own the practice. I could essentially retire any time but owning a business with employees is keeping me off the Obamacare exchange. Would I pick OB/GYN again? I really do not know. It is possible now to do shift work (hospitalist or laborist) which did not exist when I was doing OB. The lifestyle is brutal and stressful especially if something goes wrong! Per hour worked lots of other fields pay better. When I was younger I liked the excitement of a STAT c-section or a ruptured ectopic but I aged out of that. I suspect that lots of ER docs and trauma surgeons feel the same way.

Did you graduate with student loans? How much & what are the interest rates?

I had $29K in student loans. I know you all hate me. I had an academic scholarship. My parents paid for undergrad and bought me a car. Medical school tuition now is ridiculous. I don’t know if I would've gone with today's prices. I can’t even remember the interest rate or payment because it was that insignificant.Financial aspects of marriage

Are you married?

I am legally married as I type this. I expect my uncontested divorce to be final in the next week or two. I had no prenuptial agreement. My state is not community property.If you are divorced – what have you learned financially from this, and what advice would you give to unmarried women planning to marry?

My attorney gave me the advice of not raising your spouses lifestyle to the “doctor” lifestyle. If you encourage them to quit work then if you divorce you may face alimony. In my case my husband is still working full time and I went to part time. I gave my husband my equity in a farm we bought which I really did not want anyway. It cost me $35k and $600 in legal fees. We married later in life and kept our finances separate.

General Finances

What’s your FI (financial independence) number?

My financial independence number is 5 million. I hit this at age 56. In retrospect with what I now know about the FIRE movement I think I could've retired at about 45.What is your net worth?

I am now 60 with a net worth of ~ 7.5 million post divorce (Includes home equity).Are you DIY?

I handle my own finances. I used a commissioned stock broker for several years starting out.How did you get to FI and what does it mean to you?

I always filled my retirement accounts up and then filled up a taxable account. I have most of my retirement money in a SEP-IRA and some in a traditional IRA. I have converted a small amount to a Roth IRA. For what it's worth, most of my money is in a taxable account. FI means you can quit work or go part-time. It means no call or weekends. It means anything you want it to mean because you no longer have to work and put up with crap.One thing you regret:

Not buying an office building.Do you have insurance?

I no longer have disability insurance. I cancelled it mid-40s when I knew I had “enough .“ I have umbrella insurance ~2-3 million.Any parting words of wisdom?

My advice is basically grow into your income slowly. Do not keep up with the Jones. Dr. Jones is 75 and still working! I made a number financial mistakes along the way but came out ok. Basically learn about money or it will fritter away. I also recognize that I was very lucky. I became an OB/GYN when very few females were doing it. The demand was huge and I never had to market myself. Those days are gone and you will have to hustle to do well I think. Good Luck.And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I loved reading “Hatton1's” story and I hope you did too. I think she may be the first woman physician interviewed here that has achieved financial independence!]]>

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – Cecilia.

Tell us about yourself:

I have been pretty debt-averse my entire life, thanks to hearing my parents argue about money for my whole childhood (my mom, who trusts God and my dad to provide for us, would buy the things her 5 daughters needed, nothing exorbitant, but groceries for 7 are not cheap, and my dad would get mad about how much things cost…while he spent $70k a year keeping the family almond farm going!). My parents to this day have minimal retirement savings other than the land they own (50 acres in the California Central Valley), which is still mortgaged. They never really taught me to manage money, but it was always pretty apparent to me that spending more than you make is a bad plan in general. In any case, being debt averse and interested in many, many things (I changed my major 3 times in college and graduated with political science, psychology, a minor in neuroscience, and decided to go to medical school right before my senior year), it made a lot of sense to do an MD/PhD program (the ultimate decision-delayer for people who can't decide what they want to do!). I was fortunate enough to have my choice of several programs, and since I had been in California for my entire life, I wanted to see what life was like outside the state. I chose the University of Chicago. It was a long road, but I eventually got through my PhD after realizing halfway through that I really did not want to continue in basic science research! But I also did not want to accrue $100,000 in debt for the rest of medical school, so I stuck with the PhD. I finished medical school in 2007 and started a general surgery residency. This did not last long, as my contract was not renewed after my intern year. I was devastated. But it turned out to be the best thing that ever happened to me both personally and professionally. I was not ready to give up the dream of surgery, so I did a second year at the only other residency program in the area. I became very close to a co-resident, and he eventually introduced me to his identical twin, who became my husband. After I finished that second year, I had no residency position at all, so I was forced to evaluate my options and choose another specialty. It was very difficult to get back into a residency program – I spent two years working at an urgent care clinic in the Philadelphia area, and enjoyed it far more than I had thought I would. I knew I wanted a procedure-based but non-surgical specialty, and I hated spending hours and hours rounding on patients – so I considered both anesthesia and emergency medicine. I applied through the Match initially in anesthesia, and when I did not match that year, expanded to emergency medicine and anesthesia the second year. I thought long and hard about what I really wanted from a specialty, and finally chose anesthesia with plans to pursue critical care fellowship, since I really missed having my own patients. I was lucky enough to have made valuable connections in medical school; they helped me secure an anesthesia spot outside the match, which started 4 years after I had completed medical school and 2 years after I'd left surgery. By the time I finally finished my anesthesia residency, I had been out of medical school for 7 years; my peers who had started medical school at the same time as I had (in 1999) had been attending physicians for as long as 8 years. In choosing a specialty, you must decide procedure-based or clinic-based, primarily outpatient or primarily inpatient, flexibility with regard to family demands (although I did not think about this since I was unattached during most of this time), and whether you want to be primarily a consultant or “the” doctor for that patient. It's also very important to consider what life is like beyond residency – this is very hard to do when you have the limited perspective of a 3rd year medical student, but you really need to ask attendings what their lives are like several years out and how they are balancing everything. I have a feeling many medical students make the mistake of not thinking beyond residency. In my case, I knew I wanted to have some ownership of my patients and relationships with them that last longer than a few hours – anesthesia does not really offer this (unless you go into pain medicine). During my two years of surgery I had spent a great deal of time in the ICU, and I really enjoyed the challenges and rewards of caring for critically ill patients. As it turns out, critical care and anesthesia are also fairly well-reimbursed fields compared to primary care. I did not consider this aspect at all when choosing a specialty (I needed a residency, any residency!), but it was a very fortunate choice since it now enables me to work part time. The only caveat to this is that outside academic centers, it is difficult to find positions that allow one to do both critical care and anesthesia. So, I have two totally separate part time jobs at two different hospitals, and no benefits with either job. And in order to be part time, I work in an anesthesia group with very low reimbursement, such that my ICU time actually pays better (for example, the anesthesiologists at the hospital where I do critical care actually make slightly less than double what I make per hour for anesthesia). Nevertheless, I'm currently 1.5 years out of fellowship, working approximately 30 hours a week (in-house time; my actual “work” time involves a great deal of home call too, so I've just given the in-house time) between both jobs.Did you graduate with student loans? How much & what are the interest rates?

The ordeal of being forced out of residency training and spending time working would have been a financial catastrophe if I had had any loans other than a small amount from my undergraduate time. I went to a private university, graduated in 1998 with about $30K in loans, which were consolidated many years ago at a 2.8% interest rate. I'm not paying them off quickly because I can earn more than 2.8% investing, and I started saving for retirement very, very late. The time out of residency (prior to completing one) was a dark period in my life because there was no job security as a non- board-eligible physician (insurance companies will not reimburse for your care for the most part), and I had no guarantee that I would ever be able to secure another residency spot.Financial aspects of kids

When did you have them?

My first was born during my fellowship and went to an excellent and very affordable home daycare about a mile from our house ($270/week). I specifically chose a fellowship program that did not have a significant in-house call requirement. The program also offered weekends off. This was extremely important in terms of work/life balance! My second child was born during the first year I was in practice. I knew after having my first child that I wanted to work part time, and I wanted to be in private practice rather than academics since I just do not do well at large academic centers with their combination of killer politics and enormous egos. Spending time with my children is my first priority (although working is sometimes easier!) They are almost 1 and almost 3, and will go to public school (our priority when purchasing a home was excellent public schools, so as a result we are in a half-million-dollar <1,000 sq foot condominium!). We were able to find an excellent sitter for them, who picks them up in the mornings on the days I work and cares for them in her home, with her own children and one other child. She works with my flexible days, and we pay her a guaranteed minimum every week (two days), with a small bonus for more than 3 days a week and an extra $20/day for pickup. We spend an average of $1800 a month for care at the moment. We were also fortunate that my husband's parents came from India for 6 months to help us when each child was born; neither had to go to daycare until age 8 months. We plan to have a 3rd child if we are able (I'm already 40!). We do not plan to fully fund our children's college educations; we are saving for state school for undergrad at the moment, which is $400/month/kid with any additional money from grandparents going in as well. We started each 529 account with the $3,000 gift from paternal uncle and grandparents. This is because we have been cautioned that you cannot borrow money for your retirement, but you can for education.Financial aspects of marriage

Are you married?

Yes. I married quite late in life as well – during my 3rd year of anesthesia residency, at age 36. We had many in-depth conversations about our goals and plans for life, including finances, before we got married. I tend to spend a bit more money than my husband, and enjoy eating out quite a lot more, but overall we are very much in agreement. He is a PhD trained software engineer, and came to the US in 2002. He has been saving money for retirement or a rainy day ever since then, even when he was a graduate student.Did you get a pre-nuptial or post-nuptial agreement?

My husband and I do not have a pre- or post-nuptial agreement; neither of us cares about money very much, and we trust each other completely. We would both just want the best for our children if we were to separate.Do you and your husband agree on finances?

We have full access to each others' accounts, although I do our financial planning. We never really combined accounts; when I was a resident and there was a large discrepancy in our incomes, we split expenses proportionally based on after-tax income. We have a single joint checking account which we use only to deposit checks with both our names on them; otherwise we pay set expenses from our individual accounts (he pays mortgage, property taxes, shared credit card bill; I pay kids' expenses, various insurances other than his life insurance, and transfer money to him if we have large purchases on the credit card, like plane tickets or new furniture).Are you the breadwinner?

Now, we both earn six figures – he is full time and I am part time at two jobs, and I expect to make somewhat more than he does this year for the first time. Last year I took 3 months of unpaid time off (a month total of vacation, 2 months of maternity leave), so I did not make as much as I will this year.Have you experienced a financial catastrophe?

My boss at the urgent care clinic (before anesthesia residency) was one of the least honest people I have ever known; the only bona fide financial catastrophe I have experienced was a baseless lawsuit he brought against me during my second year of anesthesia residency (for breach of a contract he'd tricked me into signing without realizing it). Hiring a lawyer for the suit, which dragged on for 6 months, set me back $35,000 – money which my fiance at the time ended up paying off for me.General Finances

I started my journey of learning about money management in my dark period between residencies, when a friend referred me to the book “I Will Teach You to be Rich”, by Ramit Sethi – I'd never realized personal finance could be so funny! Although it is not specific to physicians, the principles of the book are very accurate and based in how people really live, not how they think they should live or how they think they are living. From there, I worked with a financial adviser who collects residents via free dinners and offers them free advice during training, then wants 1.2% of AUM plus $2,400 to do a “life” plan once done with residency. I broke up with him after I realized the 529 he'd steered us toward for my firstborn cost ~6+% and a state plan I set up myself would cost about 0.3%. But I do credit him with helping me get life and long-term disability insurance, as well as pointing out the need for umbrella (and therefore high-limit home and auto) insurance. I've not yet needed to use my long-term disability coverage, and it is quite expensive ($4800/year for a $7,200 monthly benefit). I just don't want to take the risk of getting rid of it. It is cheaper, incidentally, if you pay for it annually rather than monthly (mine is about $20/month less).What’s your FI (financial independence) number?

I am still trying to figure out what our financial independence number is; probably somewhere close to $4 million, assuming we spend about 25-30 years in retirement and need about $150K/year. It is very difficult to know exactly what this number should be, since it depends on how old we are when we retire (husband wants to be done around 60, I am thinking perhaps 65, and we expect to live to be at least 90 since I have two grandparents still living in their early 90s), as well as what happens to Medicare in the next decades. If we are unable to gain insurance through Medicare, the numbers will be VERY different. It also depends on where we want to live and when/whether we end up buying a bigger house (anything in a good school district is about 1.5 million right now, and if we wait to buy, it will only go up).What is your net worth?

I'm not sure exactly what our net work is but it is somewhere close to $1 million given my husband's 15 years of dedicated saving. The current plan is to save like crazy for another 7-8 years to try to hit $2 million, then reduce our contributions to more like 50K/year and buy a larger house, with extra payments to the mortgage if we can afford them. The flaw in all of this is that we will have to sell our current condo to afford a down payment, but we would prefer to keep it to make money. I will also very likely have to take a full time job since there will be simply no way to afford payments on a 1.5 million dollar mortgage (with $2,000+/month of property taxes) without a combined income of at least $500K – housing expenses will be $12,000 per month once extra expenses, insurance, and taxes are factored in. This compares to $2,900 a month on our tiny condo. Running those numbers makes me think perhaps we will just stay here forever and find a way to squeeze our hoped-for three children into our 2 bedrooms!How are you saving for FI/retirement?

Our savings goal at present is $100K/year (we were at about 90K last year, which was about 35% of post-tax income). This is a combination of a solo 401K for me (lower fees and up to 25% of net profits as the employer contribution, a better deal than the 401K offered by my W2 anesthesia position), my husband's 401K (with a paltry $3,000 employer contribution), backdoor IRAs for both of us, and his discounted employee stock purchase program (17,500/year). The remaining amount goes in taxable accounts (Vanguard brokerage account). I have a few individual stocks, but the vast majority of my portfolio is Vanguard index funds (I like the Target Retirement Date funds since they automatically rebalance as the target year approaches). I have a little money invested with Lending Club and Ariel Investments; the fees for the latter are quite high (about 1%), but their average returns are about 10%, so I figure it is worth a try for a few years.One thing you wish you knew/regret:

One thing I wish I had realized about marriage is that there is a tax penalty for it unless only one spouse works, since the total household income determines the tax bracket! We both have zero exemptions and extra withholding on our W2s, and I pay very large amounts of estimated taxes on my 1099 income because I do NOT want to be unpleasantly surprised by a large tax bill at the end of the year. Since I have been doing this we have gotten large refunds. My greatest financial regret is that I did not save any money during my MD/PhD years – I was earning a stipend for living expenses, and making extra money by doing TA-ships and working as a waitress…but I spent it all. I saved nothing until I started residency, and even then it was only about 5% of my paltry salary. I didn't even save much during the two years I worked in urgent care and earned $125,000 a year! On the other hand, doing MD/PhD has saved me from the crushing debt burden of most physicians, and I never had any credit card debt either. But the magic of compound interest is something I truly wish I had harnessed in my 20s instead of my late 30s.Any parting words of wisdom?

I feel thankful every day that I have finally achieved the dreams I had as a young woman – working part time, in both my chosen specialties, a mother, a wife, and in the area I'd always dreamed of – close to home but not too close. I hope that by participating in this series I have offered some insights that may be able to help others do the same.And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I hope you enjoyed reading Cecilia's story!]]>

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]