investing

This is a guest post by Letizia of Semi-Retired MD. She and her husband are both physicians and financially independent, in part, from investing in direct real estate. Their website is chock full of amazing information on how to choose the right investment property.

Investing in real estate can seem overwhelming at first. Where should I start looking for properties? How do I know if a property is a “good” deal? Who can help me through the process? Real estate investing, however, is not as difficult as it first may initially appear. You know much more about real estate investing than you think you do.

Most people have had experiences with renting and buying their own apartments and homes. These types of experiences, when combined with focused reading and supportive mentors, can make a plunge into real estate investing relatively easy and successful, even for a newbie.

In this post, I cover some of the reasons that direct-ownership of real estate investments is such an attractive way to build true wealth. I also provide you with simple guidelines for how you can take the first few steps towards becoming a successful real estate investor as you work to become financially independent. By the time you’re done reading this, you will know how to start working towards achieving financial freedom for you and your family by owning your own rental properties.

Do I need to own rental properties? Can’t I just buy real estate stocks?

There are numerous ways to invest in real estate. On one end of the scale is the most passive form of real estate investment, Real Estate Investment Trusts (REITs), which are traded much like mutual funds. REITs are followed on the scale by less-passive forms including syndications and finally by direct-ownership of rental income-producing properties.

In this article, I concentrate on the direct-ownership of rental properties. I do this because this type of real estate investing will get you to financial freedom the fastest. This is not to say you should not consider more passive forms of real estate investing on the path to becoming financially independent if it suits your risk-profile, interest and/or time restrictions. Just understand that some of the benefits of real estate investing discussed below do not apply to less-passive forms of real estate activities.

Do I have time for this?

We all know women often shoulder much of the the burden of unpaid work in the household. So why should you add the responsibility of real estate investing to that load? Why not leave it to your significant other?

First, once you learn how to successfully invest in real estate, your skills and knowledge will never be lost. You will always know how to bring in money for your family using real estate investing no matter what happens. We’ve all seen the stories of women losing their significant others, becoming sick themselves and going through horrible divorces. I, myself, have been through a divorce. And like others, I had to face the question of how I was going to support myself and my family.

As doctors, we can often fall back on our jobs when things like this happen, but wouldn’t it be better if we had our jobs, $100K in semi-passive income coming in each year from our real estate properties AND we felt confident that we could run the business (and even expand it)?

Isn’t owning rental properties a lot of work?

It’s true – direct-ownership of real estate property is not 100% passive. You have to manage the property managers; you have to manage the bookkeeper. There’s work involved with buying and selling properties. However, the amount of work for the earned income is disproportionate.

You can work a couple of hours a month and earn tens of thousands of dollars. And, over time, you can make your real estate business more and more passive by putting in place systems and people to manage most of the day-to-day issues. I’d argue it’s worth learning to make money this way so you never have to make financial decisions (or family or personal decisions) out of the fear you won’t be able to support yourself and your children.

How can real estate help me become financially independent?

In my mind, there are three main reasons you should start using real estate investment properties as a vehicle to propel yourself to financial freedom.

# 1. Wealth Building

We recently analyzed our real estate portfolio and found that we, on average, have a greater than 25% return on our real estate investments. How do we do this?

- Leverage: when you own investment property, you also make money on the bank’s loaned money as well as your own. That’s the power of using leverage.

- Cashflow: cashflow is the amount of money you make each month after all the expenses are paid. It’s the rent that actually goes into your pocket. Cashflow is the extra income source that can allow you to cut back at your clinical job or allow you to weather a particularly difficult financial month (or year).

- Equity Paydown: when you buy a property right, your renters pay down your mortgage each month, thus making you money a third way: equity paydown. Equity paydown grows each year as your mortgage payments become less interest and more principal.

- Property Appreciation: by the nature of the real estate market, your investment property will usually gain market value (appreciate) over time.

- Rent Appreciation: this is the amount that you can increase rent rates per year. It usually ranges on the order of 2-3% percent per year, which, over ten years can mean that your property’s rent increases 85%!

- Forced Appreciation: in addition to market-controlled rent appreciation, you also can increase a property’s value by improving it and then increasing rents proportionally (or disproportionately), which is called forced appreciation.

And, finally, there’s tax savings, which we will discuss more below.

#2. Control

When you put your money into REITs or the stock market or even into syndications, you lose most of your control. You cannot control if the CEO of a company is going to embezzle money. Also, you cannot control if the general partners of a syndication are going to make good financial decisions. You can only hope and trust in others to manage your money well.

In comparison, when you directly own investments, they belong to you. You can control how they are managed. You are the decision-maker. In fact, you are the CEO. You can make changes that add to the bottom line, which, in this case, ends up directly in you and your family’s pocket.

# 3. Tax Benefits

The tax benefits of direct-ownership can be substantial. While these may not initially be your primary driver to get into real estate, they really should be at the top of your list. They can significantly reduce a typical physician's tax burden.

One of the main reasons the tax advantages of owning real estate is so great is because the government allows you to depreciate at minimum 1/27th of the value of your property (the building, not the land) each year. This means that over the course of 27.5 years, your property value becomes $0 (and, remember, you’ve only paid probably 20-30% down, so you’re actually collecting depreciation on the bank’s money as well as your own). What this means in practice is that you make money through cashflow each year but it looks like you are actually losing money (paper losses).

Depreciation, when combined with the write-offs you make on improvements/rehab and the fact you don’t pay payroll taxes on your earnings, means that making $100K in real estate is equivalent of making closer to $140K at your job.

How do I even start investing?

Now that we’ve covered some of the benefits of investing in real estate, let’s tackle how you can actually get started to building your business. The first step is to educate yourself. You need to understand the basics. When you are presented with a property, you can run the numbers and know if it is a good deal. It is not a good idea to rely on others to tell you if something is a good purchase since they may have competing interests.

Read and Listen

When we first started real estate investing, we found a couple of books extremely useful. Rich Dad, Poor Dad by Robert Kiyosaki gave us the “why” of why we needed to expand beyond just relying on our 1040 incomes for the rest of our lives. Then we used books like Real Estate Millionaire Investor by Gary Keller to explore the hows. Over the years we’ve also added in podcasts, like Bigger Pockets, which give us both motivation and useful information by learning about other’s stories. [ Editor's note: Also check Paula Pant's Afford Anything podcast ]

Know the Numbers

One of the keys is when you’re educating yourself, make sure you find a good cash on cash calculator (you can get ours in our Facebook Group). That way, you you can plug the numbers in for deals you come across to determine if they meet your criteria. You should have a minimum cash on cash you are willing to accept from a property. This keeps you from buying properties that are not going to bring in money each month.

Connect with Others

Another important step is to network with other investors. By networking, you have people who can connect you with their resources and offer advice when you’re not sure what to do. Experienced investors have come across a lot of weird situations. Instead of reinventing the wheel yourself and making avoidable mistakes, why not take advantage of collective experience and knowledge and help yourself grow faster with less risk?

You can find investors in a variety of ways. You might try any of these:

- Connect at meetups.

- Join local Facebook groups such as REI MD.

- Read real estate investment-focused blogs.

Build your Team

Another key step is to find yourself an investment real estate agent. This is not just any real estate agent. Instead, find someone who specializes in working with investors and who ideally owns his or her own investment properties.

In addition to finding you deals, an investor agent should be able to help you build the rest of your team like your property manager and your general contractor, since he/she has used and vetted these same people for his/her properties.

Harness the Power of Women

Now, I know I’m biased here, but I do believe that women are uniquely positioned to be successful in real estate investing. Many of us run our family’s finances. We organize the details of our family’s schedules. Plus, we do all the planning and packing when we go on trips. We manage a lot of relationships. And all of us are awesome at multitasking.

We bring all of these skills to the table when we enter the market as real estate investors looking to become financially independent. The key is just to get started in educating yourself and building your team so that you can work towards building financial independence for yourself and your family today.

Want to learn more?

Explore our blog at Semi-Retired MD or join our facebook group.

2018 is well underway. Last year, M and I had a good amount of tax advantaged retirement “pots” available to us along with some employer match and contributions:

- My 403(b) + generous employer match + contribution

- My 457(b)

- My cash balance plan

- My backdoor Roth IRA

- My solo-401(k)

- His 403(b)

- His Roth IRA

- His solo-401(k)

- My 401(k) + employer match

- My solo-401(k)

- My backdoor Roth IRA

- My HSA

- His 401(k) + employer match

- His Roth IRA (may need to backdoor it this year)

- His family HSA

- Our taxable account

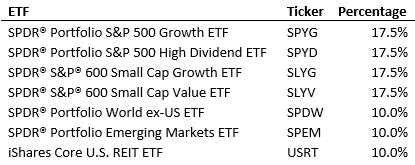

- 68% US stocks

- 17% Large cap growth, 17% Large cap value

- 17% Small cap growth, 17% Small cap value

- 24% International stocks

- 12% Large cap developed countries

- 12% Diversified emerging markets

- 8% US REITs

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

Last month I spelled out how we are investing our money in 2017. I mentioned there were some moving parts – namely, M was unemployed and we knew, at the time, that I was (newly) pregnant. Now, M has a job (yay!) and looks like this pregnancy will stick, so now we can do some real projections for 2017. Our asset allocation will remain the same.

This year our total “retirement” contributions will consist of:

This year our total “retirement” contributions will consist of:

- $18,000 my 403(b)

- $20,800 employer match + contribution into my 403(b). Currently 20% vested. 40% vested as of August 1, 2017 so actually $8,320

- $18,000 my 457(b)

- $5,500 my Roth IRA

- $18,000 his 403(b). No matching at this time

- $11,000 his Roth IRA (his first! For 2016 and 2017)

- Other sources:

- A very modest amount ~$1,000 into my solo-401(k). Yes this blog likely won't lose money this year 🙂

- ~$5,000 his solo-401(k) – he has some 1099 income this year

If you work for a large healthcare provider, you may have access to a 457(b) retirement account in addition to a 401(k)/403(b). Are you using it? Maybe yes, maybe no. You might want to use your hospital's 457(b).

Here's why:

The Benefits of Your Hospital's 457(b)

- Tax benefits! With your hospital's 457(b), you can invest an additional tax deferred $19,000 annually (in 2019). This escalates to $24,000 annually if you are over 50. Why do this? This lowers your taxable income. Like a 401(k), you pay income tax when you withdraw. Some 457(b)s even offer a Roth option.

- Flexibility! In addition, you can withdraw this money before age 59.5. This is great if you are planning early retirement. Why? Unlike the 401(k)/403(b)/and most IRAs, you'll have access to your money earlier.

Understanding The Types of 457(b)s

There are 2 types of 457(b)s and it's important to know which type your employer offers. There are governmental (or public) and non-governmental (or private) 457(b)s.

Governmental 457(b) Options

If you have a governmental 457(b), this is a “no-brainer”. You should use it if you need more tax advantaged space to save in. Of course, this also depends on if the plan costs and fund choices are agreeable. Public 457(b)s can be rolled over into an IRA or 403(b)/401K(k) when you leave the job.

Private 457(b) Options

Private 457(b)s are different story. The money you deposit technically belongs to your employer and can be used to pay off employer's creditors. This is only an issue if your hospital goes under. A good way to see if your hospital is afloat is to check their credit rating. I know this sounds scary but as far as I know, no one has lost their 457(b).

Exploring Your Hospital 457(b) Plan Options

The next step is to find out what the distribution options (if there are any) are when you leave the job.

Some plans make you take out one lump sum on separation. This is a lousy option, and I would hesitate using it.

You want multiple options. Preferably, you can defer distribution until retirement age and take money over time to control your taxable income. The main “con” of a private 457(b) is that you can only roll it into another private 457(b). Another catch is this. Your new private 457(b) would have to accept rollovers, and they don't have to.

Your best bet is to always get a copy of your employer's 457(b) plan as details can differ widely.

Final Thoughts on Your Hospital's 457(b) Plan

A 457(b) is a way to have access to your money before age 59.5 besides a taxable account

Your retirement savings plan should include different types of accounts to diversify. A 457(b) is a way to have access to your money before age 59.5 besides a taxable account.

I am using my hospital's private 457(b) account. I almost maxed it out last year ($16K) and will be maxing it out this year. My 457(b) plan is low cost and has a limited fund list but does include some basic Vanguard funds. Fortunately, the distribution options are very flexible so upon leaving this job, I can defer distribution until retirement age.

Since this post went live, I left the hospital job. I chose to cash out my 457(b) despite being able to leave it there indefinitely. Why? I wanted total control over the money. Yes I paid income taxes on it. I promptly deposited the check into my Vanguard taxable brokerage account. With the changing and unstable landscape of medicine, I do not want to depend on the hospital staying afloat.

No matter where you are in your career or where you are on your retirement journey, inquire about your 457(b) plan that your hospital offers. You might be able to get your hands on some serious tax-time benefits and add more flexibility to your retirement plan.

Does your job offer a 457(b)? Do you use it? Why or why not?

First, a bit of (short) investing history.

I invested $1,000 into a Roth IRA during my third year of residency (2015). This account is at Vanguard and I initially invested all of it in their 2045 Target Retirement Fund. I had no idea how to invest my money but I knew that Vanguard was a good place to start.

My first (and current) attending job (started September 2015) gave me access to a 403(b) and a 457(b) plan. They have a limited fund list, but have some low cost Vanguard funds. Again, I still had no idea how to invest, but luckily, they automatically selected a Vanguard Target Fund based on your age. I managed to contribute close to $16K for 2015. I did not really understand what a 457(b) was and read some “bad” things about it, so I decided to figure that out later.

In 2016 I maxed contributions to the 403(b) ($18,000) and started receiving a generous employer match (about $16.5K in 2016). Takes time to fully vest but I am currently 20% vested. I almost maxed out the 457(b) plan as well – about 16.5K (more in an upcoming post about how and why I ultimately decided to use this). I also funded both my 2015 and 2016 Roth IRA via the backdoor, although I fell a little short for my 2015 contribution at $4,000.

I read more about index funds and how to create an asset allocation. After tinkering with things a few times, I finally “set it and forget it:”

- 55% US stocks:

- VIIIX: Vanguard Institutional Index Fund Institutional Plus Shares 0.02%

- VIEIX: Vanguard Extended Market Index Fund Institutional Shares 0.12%

- 20% International stocks:

- VFWSX: Vanguard FTSE All-World ex-US Index Fund Institutional Shares 0.11%

- 10% Small cap value:

- VISVX: Vanguard Small-Cap Value Index Fund 0.2%

- 8% REITs:

- VGSIX: Vanguard REIT Index Fund Investor Shares 0.26%

- 7% Bonds:

- VBMPX: Vanguard Total Bond Market Index Fund Institutional Plus Shares 0.05%

I hold the small cap value and REIT fund in the Roth IRA. The rest are in the 403(b) and 457(b). I have yet to open a regular old taxable account.

How did I do? Well, turns out it's not that easy to really know:

This is a screenshot from Personal Capital. I use this to get a nice “overview” of my investments and it has some nice graphics and tools to play around with. On the upper left you'll see the “You Index.” This is NOT the actual portfolio performance though, it's the performance if you had held your funds from the starting point of the graph. It's still useful as a rough guide though. You'll also notice that the S&P 500 finished at 9.54%, but this doesn't take into account dividends re-invested. The S&P 500 finished at 11.96% with dividends re-invested.

This is a screenshot from my 403(b) plan. 17.59% ! But I checked this on 1/9/16, so it's not exactly all of 2016 but close enough. My 457(b) returned 8.4%. My Vanguard account's return was 11.8%. My best guess is that overall, based on portfolio % (the bulk of my money is in my 403b), I clicked in around 14%. But the range is probably 13-15%. Not bad for a very new investor.

My allocation will likely change in 2017 (planning on getting rid of the bonds, for example) and I'm going to switch to ETFs in the Vanguard account.

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]