2018 is well underway. Last year, M and I had a good amount of tax advantaged retirement “pots” available to us along with some employer match and contributions:

- My 403(b) + generous employer match + contribution

- My 457(b)

- My cash balance plan

- My backdoor Roth IRA

- My solo-401(k)

- His 403(b)

- His Roth IRA

- His solo-401(k)

- My 401(k) + employer match

- My solo-401(k)

- My backdoor Roth IRA

- My HSA

- His 401(k) + employer match

- His Roth IRA (may need to backdoor it this year)

- His family HSA

- Our taxable account

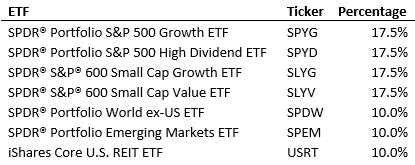

- 68% US stocks

- 17% Large cap growth, 17% Large cap value

- 17% Small cap growth, 17% Small cap value

- 24% International stocks

- 12% Large cap developed countries

- 12% Diversified emerging markets

- 8% US REITs

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

Get the bestselling book - Defining Wealth for Women.

Recent Posts

239: What They Never Taught You About Money in Med School

Med school taught you how to diagnose disease-not how to create financial freedom. In this episode, I’m pulling back the curtain on the mindset shifts that completely changed my money philosophy-and my life. Spoiler: it’s not about how much you save or what you invest in. It’s about getting clear on what you actually want,…

238: Black Friday Hacks for High Earners: How to Shop Smart and Stack Points Like a Pro

It’s Black Friday season-are you ready to rack up serious points while scoring deals? In this episode, I break down my personal strategy for stacking points with Rakuten, maximizing perks from premium cards like the Amex Platinum and Chase Sapphire Reserve, and why NOW is the best time to apply for a new card. I…

237: Rethinking Wealth: Why Financial Flexibility Beats Retirement Planning

Most financial advice boils down to this: Grind for 30+ years. Max out your 401(k). Hope it all works out at 65. Yeah… no. In this episode, I sit down with Austin Dean, founder of Waystone Advisors, to explore a better way to think about money-one that prioritizes financial flexibility now, not just retirement later.…