Marriage & Children

Investing in Your Romantic Relationship May be One of the Most Powerful Decisions That You Ever Make

Editor's Note: This is a guest post by a fellow Wealthy Mom MD, Dr. Ali Novitsky. She is the CEO of Lifecoachingforwomenphysicians.com. She is a certified life and weight loss coach, board-certified pediatrician, board-certified neonatologist, blogger, national speaker, and host of the podcast, “Life Coaching for Women Physicians.” Dr. Ali runs The Life Coaching Society, a monthly membership experience for women physicians to prioritize their themselves in a supportive community setting.

Let’s face it, relationships can get complicated…if we let them. You see, we have the power to simplify our relationships by understanding a few key concepts. It is in this simplification that we can find peace and happiness.

Before we go on, I do want to make one important point. Not all relationships are meant to survive. There are some situations where drugs, alcohol, emotional abuse, physical abuse, and ongoing affairs may be involved. These factors may prevent any further relationship investment. And this is 100% acceptable. The beauty is that YOU GET TO DECIDE.

The concepts that I am about to share will allow you to think about your relationship in a whole new way. The goal is for you to see what a true investment in your relationship looks like. I will also provide real strategies for you to start using today. Sound too good to be true? Read on.

“Why Does My Partner Get on My Nerves?”

If you’ve ever found yourself frustrated with your significant other, the first concept that is essential to understanding your frustration is appreciation of “The Manual”. I did not invent the concept of The Manual – I learned about it during my training at The Life Coach School with Brooke Castillo. And- it has changed my marriage.

Let me elaborate. I always believed that I had a great marriage. We started as friends, we fell in love, we then started dating, and the rest is history. But let me back up. No relationship is perfect. Sometimes I would get frustrated when I started to think that Mark should be acting in a certain way.

I came to appreciate that my line of thinking: “Mark should be acting in a certain way” caused me to feel FRUSTRATED. With this frustration, I was short-tempered with Mark. I perceived Mark’s behaviors as him not prioritizing our relationship or undervaluing me and started to have negative thoughts about myself. I can remember thinking, “I’m not important.” And, as I result I believed that Mark SHOULD act differently so that I could feel important.

The Manual is an invisible script that lists certain expectations that we have for another person. Here is the problem. When this person does not meet these expectations (Spoiler Alert: Usually they won’t), we become disappointed. By keeping a Manual for another person, you are releasing all of your power. Why? Because you are allowing the other person to make you feel a certain way or not feel a certain way.

So what can we do? We can literally throw away The Manual. That’s right- toss that bad boy in the trash. When we release the expectations we have for another person, we cannot be disappointed. By throwing away The Manual, we are saying, “I love you exactly the way you are.”

Sound too good to be true? Throwing away The Manual is 100% effective, however, holding onto this script is our tendency. I challenge you to make this investment, guaranteed to be worthwhile.

Investing in Unconditional Love with a Positive Mindset

If we throw away the Manual, then we are able to love the other person unconditionally. Practicing unconditional love is the second tool I want to offer for you to use as you create your relationship portfolio.

I want to explain unconditional love. When we feel love, it is not the other person that is sending this feeling to us via radiofrequency. The feeling of love is generated from within us. We feel love when we think thoughts about the other person that is allowing us to feel love.

Here is an example. If you think the thought, “My spouse shows up everyday at work so he/she can provide for our family,” you may feel loved. Do you see how you are generating the feeling of love because you are thinking certain thoughts about the other person?

You can choose to feel love anytime you want. When you choose to feel love, then your actions will reflect that feeling of love. Your result will be that you truly appreciate your spouse for his/her hard work which will allow you to generate more and more unconditional love. This investment will benefit everyone.

"You can choose to feel love anytime you want. When you choose to feel love, then your actions will reflect that feeling of love." -Dr. Ali Novitsky MD Share on XMaybe you are having a hard time accepting the concept of unconditional love. I understand. Perhaps your significant other does something that really bothers you. Let me give you an example. Perhaps your spouse makes it a point to comment on other attractive people constantly. You find this hurtful.

Communicate More Effectively by Setting Boundaries

Let me introduce you to investment number 3. Setting a boundary. Setting a boundary is something that most of us do not do. This boundary, when set appropriately, will allow you to communicate a rule to your partner. When you set a rule verbally, you do not have an invisible Manual, but instead a clear guideline of what you expect from the other person.

It is very important that you understand how to set a boundary. If the boundary is not set properly, then you will dig a deep hole. Why? Because you will not be taken seriously.

To set a boundary, here are the exact steps to follow. Your partner says, “did you see that beautiful woman who just walked in, she is unreal.” You will then say, “when you make comments about other women in front of me, it is hurtful.” Your next statement should go as follows. “If you continue to make these comments in front of me, I will walk away from you.”

Remember…if your spouse continues to comment on other women, then you must stick to the boundary you set and walk away. By investing in boundary setting, you truly simplify things. You are being 100% open about what you expect. This will increase your feeling of empowerment in your relationship. This feeling of empowerment is because you believe that you are standing up for yourself- and you are. Setting a boundary is increasing your perceived value in the relationship. Now that’s an investment.

What is Your Partner’s Love Language?

What about love language? The 4th worthwhile investment in your relationship is understanding your partners love language. Here is why this investment is so important: By understanding your partner’s love language, you are opening up the channels for communication. How so? When you invest in showing your partner his/her love language, they will think thoughts that make them feel loved.

Here is an example. Let’s say that partner A’s love language is physical touch. Partner B’s love language is giving gifts. If partner B recognizes that partner A likes to be touched, and he/she provides physical touch, then partner A will feel love.

Partner A may be thinking, “my significant other cares about my needs.” The love that partner A feels will very often result in actions that will make partner B feel love. If partner A recognizes that partner B likes gifts and brings home flowers, partner B will feel love because he/she is thinking, “my significant other cares about my needs.”

Do you see how understanding your partners love language sets the stage for great communication? Why? Because it eliminates some of the barriers that would prevent good communication.

The next investment is probably the most difficult one. It may feel like a risky investment because you will need to put your ego aside and allow yourself to be vulnerable.

Rewrite Your Story by Letting Go of Pain from the Past

Investment Tip #5 is letting go of pain from the past. If we decide that our relationship is worth keeping, then we have to be willing to let go of the past. If we do not let go of the past, then we will carry resentment and not be able to move on to a better place.

It may seem impossible to let go of the past in certain situations. So, how do you even start? The first step is to have an honest and open conversation with your significant other so you both can express your side of the story.

The next step is to process. Processing all of this information can take days, weeks, months, or even longer. In fact, you may need to invest in professional help through therapy or life coaching to guide you through this process.

When the time is right, the strategy is to rewrite the story. You will rewrite the story in a way that allows you to release resentment. This release will allow you to glide into the future with hope. This investment is a powerful tool in saving your relationship.

I do think it is important to know that if you do not feel that you will ever be able to rewrite the story, then what you may need is time. On the other hand, you may decide that the story should not be rewritten. This is strong evidence that you may be ready to move on.

Scheduling Time for Your Relationship Every Week Will Pay Off

Finally, the 6th investment is making time. Scheduling dedicated time to your relationship is similar to contributing a fixed amount of money every pay period into a retirement account. Every time you commit to special 1:1 time, you are inviting intimacy into your relationship. Over time, this intimacy builds and you have comfort in knowing that you are accumulating collateral.

We are all very busy. You may be thinking that setting time aside may feel impossible for you. I want to encourage you that it is quite possible. The trick to making this happen is to simply put it on the schedule. I highly recommended making time once per week to connect with your significant other. My best advice is to keep it simple.

Start small. You do not need to make these investments all at once. Decide which investments speak to you. Most importantly, open your mind and consider how a shift in your thoughts can bring high dividends to your relationship everyday.

To learn more about Dr. Ali Novitsky, check out Lifecoachingforwomenphysicians.com and The Life Coaching Society, a monthly membership experience for women physicians to prioritize their themselves in a supportive community setting.

Listen to Carrie & I discuss prenups over at the Hippocratic Hustle!

You have life insurance. You have disability insurance. But do you have divorce insurance? Probably not. But why? Last time I checked, the divorce rate isn't zero. Thankfully, doctors enjoy relatively low divorce rates–in the 25% range–but still, that isn't zero. In fact, you're much more likely to get divorced than become disabled or die over the next year.

Whether you realize it or not, you sign a legal contract when you get married. You also agree to your state's “one size fits all” prenuptial agreement if you don't have your own (aka a finely tailored suit). While prenups may still feel taboo, it’s time to start talking about them.

Here are 10 things that you need to know about prenups now.

# 1. Marriage is a Legal Contract

When you say, “I do”, you’re probably not thinking about marriage as a transaction. This isn’t the day of dowries, after all. But marriage is a legally binding contract. Because of that, marriage comes with certain rights and financial perks. Rights can vary a bit by state, but generally a marriage contract creates rights that include filing joint tax returns, inheriting property after a spouse’s death, and receiving a spouse’s benefits (Social Security, pension, etc.) after their death. Financial perks include unlimited gifting to each other, spousal Roth IRA and sharing the federal estate tax limit. Marriages also create marital property. That means that the property and income that you earn while married may become property of your spouse. How that share of marital property is determined is based on your state.

# 2. Marriage is State Specific

Location matters in real estate. It matters in marriage as well. Different states have different laws and rights surrounding both marriage and divorce. Different states have different requirements when it comes to getting married. Some states may require witnesses; others have periods of wait time between requesting a license and when it is finalized. What happens when you’re not legally married? Cohabiting is on the rise with more people holding off on officially tying the knot. While many people believe the myth that cohabiting together automatically creates a common law marriage, common law marriages are actually recognized by very few states and vary widely by state. Just like marriage varies by state, so does divorce. While divorce is often talked about as a 50-50 split, the way in which property is divided in the event of a divorces depends on the state in which the couple lives. Nine states are community property states where property is split in half, and the other states are equitable distribution states. In the case of equitable distribution, the court will decide on how property is split.

# 3. Divorce is a Weapon Of Mass Destruction

Marrying the right person can be hugely advantageous. This isn’t just about love and happiness, although those are supremely important, too. Marrying a spouse that you are compatible with not just emotionally, but mentally and financially, can have huge benefits. When your relationship is strong, you can work harder and more effectively toward goals, and you’re more likely to be able to weather any storms. While doctors are less likely to get divorced than other professionals, divorce does happen. And to borrow the words of The Happy Philosopher, divorce can become a weapon of mass destruction. Certainly, divorce can be devastating emotionally. It can ripple throughout your family and friends. It can also destroy your finances (like it did for this physician), which is why a prenup is actually to the advantage of both partners.

# 4. Understanding Alimony

In the event of a divorce, alimony can comes into play. This is especially true if one spouse is the primary breadwinner, which is a typical dynamic in doctor households. Alimony is intended to provide maintenance and support. Unfortunately, states will look at total income instead of the couple's actual spending to determine how much alimony will be due. If the court decides that you have to pay your former spouse alimony, it is either paid out in one lump sum or on a continuing basis. The new tax law makes alimony less palatable. Couples can also reach an agreement on alimony without going to court; but it is only valid if both parties agree.

# 5. Attorney Fees and Then Some

While you may have seen divorces advertised for as little as a few hundred dollars, most divorces become quite costly. An older Forbes estimate stated that divorces that become highly contested can cost $15,000 or even $30,000. Divorce becomes so costly if it is a particularly litigious battle, and that cost is primarily due to legal fees. In many cases, both parties involved in the divorce will retain lawyers. With divorce lawyers' hourly rates starting at $50-$75 an hour but easily clocking in at upwards of $300 an hour, it is easy to see how quickly these bills can mount. In addition to paying for lawyers, there is also a trial fee that has to be paid as well. The longer the divorce proceedings, the bigger the bill.

# 6. One Size Fits All?

Like clothes, a one-size-fits-all plan can often be a bad fit and an even worse idea. Without a prenup, you are at the mercy of two things: your state and the divorce court you end up in. In addition to deciding how your marital property will be divided based on the state you live in, a judge will also make other considerations, many of which will be based on precedents. That means that other people’s marriages and divorces could influence yours. If no two marriages are the same, neither are divorces. Try as we might, this one-size model just isn’t a good fit.

# 7. A (Cheap!) Finely-Tailored Suit

A prenup is like a finely tailored suit in that it provides a custom fit for your relationship. The key difference between this metaphoric suit and a real custom suit is that the metaphor is actually the real bargain. Divorces are messy, and without a prenup, you are really at the mercy of many different factors: legal teams, judges, state laws, precedents, and your former partner. Sometimes splits are amicable, but sometimes they are far from it. A prenup will spell out how assets should be divided in the event of a divorce, which should minimize the amount of court time and the legal fees.

# 8. Prenups ARE Romantic!

Romantic love is a modern concept. And people can and should marry for love. But there is nothing romantic about being reckless. While whirlwind romances look good on the big screen, they’re often not in real life. Taking some time to thoughtfully plan out your marriage and discuss your dreams, goals, and ambitions help put a solid foundation under your relationship. Crafting a prenup lets your partner know that you are hoping for the best for them while you are together and in the event that you break up. By crafting a prenup in advance, you and your partner are able to make decisions based on what is truly best for each of you instead of in the heat of the moment during a divorce. Calmer emotions and cooler heads prevail when it comes to finances, and planning for prenup is no exception.

# 9. A Worthy Investment

While discussing divorce doesn’t seem particularly romantic, it’s actually a really important way to invest in your marriage. But a prenup is just the beginning when it comes to investing in your marriage. In addition to being a contract, a marriage is a choice and a commitment that you and your partner make every day. Being married is hard work. Whether it’s taking time to go on dates or do small things for the other person or investing in couples counseling before situations get difficult, there are many ways to strengthen your marriage and keep it healthy. It isn’t always easy, and it isn’t always cheap. But it’s an investment that will pay dividends.

# 10. It’s Not Too Late

While the ideal time to read this post would be before you tie the knot, it’s actually not too late if you’re already married. In addition to prenuptial agreements, courts also recognize postnuptial agreements. A postnup functions similarly to a prenup in that it is a document that outlines how your assets will be divided in the event of divorce, but it is created after you are married. Speaking with a legal expert will help you understand how both prenups and postnups work in your state.

Final Thoughts on Prenups

When we talk about people being underinsured, we often think about homeowners insurance or auto policies. The truth is one of the biggest ways we are underinsured is actually related to marriage. A prenup isn’t setting your marriage up to fail. It’s a plan to keep you and your partner on the same page financially and to show your partner that you want the best for both of you if things don’t work out. Instead of thinking of it as taboo, maybe it’s time to start thinking of prenups as romantic.

Since the engagement, everyone has been asking, “So, when's the wedding?” When most people think of engagements and weddings, the legal aspect of marriage is not the first thing that comes to mind. But saying “I do” is a legal contract. That's one of the reasons why we are happily engaged but not planning to be married anytime soon.

The fact that marriage is a legal contract isn't the only factor shaping our decision. In fact, here are the reasons in no real order:

- Marriage penalty tax

- M is divorced and has a child from a previous marriage

- Neither of us really feel like blowing money on a wedding

I have 6 figure student loan debtWe are trying to start a family

Marriage as a Legal Contract

Marriage is a legal contract and nothing more. People add the other stuff– mainly the religious part (we aren't particularly religious but our parents are). Don't get me wrong. I fully respect the institution of marriage and the commitment and all that it entails. It's just that legal marriage isn't the necessity it was for women as it is today.

The Marriage Penalty Tax Does Exist

Most people think you get a tax break by getting married. It depends.

Most people don't realize that the married filing jointly tax brackets are not double the single brackets. Depending on how much you and your spouse make, you may actually pay a marriage penalty tax. This mainly occurs when you both make a similar income. The marriage bonus mainly applies to couples where one spouse makes a lot less or is a stay at home parent.

Note: Since this post went live, there was a major overhaul in the tax code in 2018. The “penalty” is much smaller now.

The Divorce Rate Is Not Zero

Then there is the possibility of divorce. Divorce rates are going down and are lower among doctors (but higher among female physicians), but most of us still have a 30%-ish chance it won't work out.

Would you sign a contract that said things don't work out in 30% or more cases in which case you may lose half of your retirement and possibly a % of your future income? Of course not!

But that's what a marriage contract is. For some reason, all logical reasoning goes out the window when it comes to the marriage contract and nobody thinks they will be in that 30%.

Of course, there are lots of benefits to being married – spousal Roth IRA, unlimited gifts to each other, and double the federal estate tax limit to name a few.

Division of Property

Divorce laws are state specific and how they “split things up” falls into two categories – community property and equitable state. In a community property state (Alaska, Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin), any assets (and debts) acquired during the marriage are considered to be equally owned by both parties. In an equitable state, the more common type, anything acquired during the marriage is considered the property of the spouse that earned it.

Spousal Support

Then there is spousal support or alimony. In some states, while a divorce is in process, you may have to pay pendente lite support, or basically, alimony until the divorce is finalized and then pay actual alimony. Alimony laws vary by state in terms of how much and how long. Any high income earner should seriously consider a pre-nuptial agreement prior to marriage.

Blending Families Can Be Complicated

Bring in kids from a previous marriage and that can complicate things more. Laws are also state specific for child support and generally do not consider the income of a new spouse. No matter what your new family looks like, blended family finances are important to consider carefully.

Final Thoughts on Marriage As a Legal Contract

Marriage means different things to different people. It also means something in the eyes of the law.

Before you rush down the aisle, it's important to consider how marriage will impact your finances and family.

Ask yourself questions like:

- Do we need a prenup? (yes!)

- Who else would be impacted by our marriage?

- Do we understand how marriage could impact our taxes?

You can also check out this checklist for blended family finances to get the conversation started. And, consider delaying marriage or not getting married. Unmarried couples are becoming more commonplace now.

While these discussions might not seem romantic at first, it's another way to commit to your future together.

What do you think? Did you consider marriage as a legal contract before getting married?

When it comes to money and building wealth, the gift tax is often misunderstood. Let's drill down to the bottom of this "gift tax" and find out everything you need to know.

What is a Gift Tax?

The 2023 annual gift tax limit is $17,000 per person or $34,000 per married couple. What do these limits actually mean? It means that a person can give away $17,000 to anyone and to as many people as they would like without having to file IRS form 709 with their taxes.

The reason there is a gift tax is to prevent wealthy folks to give away large swaths of their money to avoid estate taxes at death. Gifting, however, is still a great way to reduce your estate tax limit if you happen to have that much money. The 2023 federal estate limit before incurring taxes is $12.92 million per person or $25.84 million per married couple. It’s also important to note that married couples can share this estate limit. When one partner dies, the other partner may have their $12.92 million plus whatever the other partner didn’t fully use.

What is a Gift?

So you understand the general premise of the gift tax, but there's another important piece of the puzzle: understanding how the IRS defines a gift. A gift is anytime there is a transfer of cash or property without receiving something of equal or fair market value in return. Many of us give gifts to friends, family, co-workers, and staff. But we don't generally buy gifts that cost more than $17,000 (if you do, let me know how I can be friends with you!). The gift limit generally applies toward family members. If Allison gives her son Tim a home that is worth $200,000, then she has given him a gift of $200,000.

While this scenario is unlikely, it is becoming more common for parents to help children with affording homes. Here's another scenario in which the gift tax matters: If Allison sells Tim a home for $50,000, but it is worth $200,000, then Allison gave Tim a gift of $150,000. Another gift scenario that many folks may not be aware of are loans to friends and family that are interest free or below the IRS Applicable Federal Rate. The IRS views these as gifts, not loans. So if you would like to loan money to a friend or family member, you must charge them a minimum amount of interest and report it on your taxes.

Married Couples and the Gift Tax

Married couples, rejoice! One notable perk of being married is the ability to give each other unlimited gifts to your spouse. This only applies, though, if your spouse is a U.S. citizen. If your spouse is not a U.S. citizen, then you are limited to giving them $175,000 a year (in 2023). But wait! Maybe you've heard there's a limit. This limit doesn't involve gifts between spouses, but rather when one spouse or the couple gives a gift to someone else. Here's how it works: The $34,000 per married couple gift limit comes into play when the gift comes from one spouse's bank account but is from the couple. For example, Carol and Jim are married. Carol gives $20,000 to her daughter Janet. $20,000 is over the $17,000 gift limit for an individual. So that would be an issue. However, since Carol is married, the gift can be from the couple and falls within the $34,000 limit. You are supposed to file this "split gift" on IRS Form 709.

Notable Exceptions to the Gift Tax

There are exceptions to the gift tax limit. Phew! Here's some of the most common exceptions: We all know that donations to qualified non-profit organizations don't incur a tax. So do gifts to political organizations. Payments made directly educational institutions for tuition for private school, college etc. are also exempt from the gift limit. Another notable exception is direct payments for medical care. To recap, these exceptions include:

- Gifts to non-profit organizations

- Gifts to political organizations

- Tuition

- Direct payments for medical care

Children and the Gift Tax Limit

The gift limit mainly comes into play for us when it comes to funding our children's education. Many of us contribute to a 529 plan to pay for college. Did you know that your contributions to a 529, ESA, and perhaps a UTMA are all subject to the annual gift limit? One exception to the annual limit is the ability to frontload your child's 529 with 5 years worth of contributions. This means you can contribute $85,000 (5 x $17,000) or $170,000 if married (5 x $34,000) at once. You won't be able to contribute again for 5 years. Note: That this means you have used up the gift limit for all gifts, such as funding an ESA, UTMA, etc.

You're Unlikely to Pay the Gift Tax

Very few of us will ever need to worry about actually paying a gift tax. Even when you go over an annual limit and file IRS Form 709, all it means is that you are reducing your federal estate limit by the amount you over-gifted. In other words, a gift tax is not calculated until you die. In which case, you won't care about owing anything anyway.

What does this actually look like? Let's suppose that you gave your daughter Susan $50,000 and filed Form 709 for the $33,000 that was over $17,000 limit. This means that your federal estate limit is now $11.58 million MINUS $33,000. Clearly, there is still plenty left!

Final Thoughts on The Gift Tax

Tax law is complicated. The rumors and myths that swirl around it muddy the waters even more. However, most of us can breathe a sigh of relief. It would be unlikely for the gift tax to apply to us. Still, arming yourself with accurate information and making sure you know the exceptions to the gift lax laws should help you see through the speculation around gift taxes.

Editor's Note: This is a guest post by a fellow Wealthy Mom MD, Dr. Monica Lee. She is a practicing OB-GYN in southern California. She has a 7-year-old son with autism. In her spare time, she loves to go skiing and reminisce about her idealistic undergrad days at Stanford.

Special needs families not only earn less but have much higher health care, non-health care and education costs. This means we have to be especially careful with our money. Not to mention a severely disabled child will not be able to work and provide for him/herself in the future and will need a large nest egg to survive. It is important to explore all resources that can help our children thrive and for parents to cope and save.

According to a 2012 Pediatrics study: On average, mothers of children with autism spectrum disorder or ASD earn 35% ($7,189) less than the mothers of children with another health limitation and 56% ($14,755) less than the mothers of children with no health limitation.

According to another 2014 Pediatrics study: After adjusting for child demographic characteristics and non–ASD-associated illnesses, ASD was associated with $3,020 (95% confidence interval [CI]: $1,017–$4,259) higher health care costs and $14,061 (95% CI: $4,390–$24,302) higher aggregate non–health care costs, including $8,610 (95% CI: $6,595–$10,421) higher school costs.

This list is especially useful for those living in southern California but may be generalized to other states, which may have parallel programs.

1. Get an official diagnosis from a neurologist or a psychologist.

In California, you can get a diagnosis through a psychologist at the Regional Center. They provide a lot of resources including respite care, Medi-Cal, therapy, parent training, and special discounts to Disneyland.

2. See a pediatrician and be referred to a neurologist or developmental pediatrician for a medical diagnosis or other underlying diagnoses.

You will need to obtain occupational therapy, speech therapy, applied behavioral analysis (ABA) therapy. Not all health insurance carriers will cover these therapies, especially ABA. Call your insurance provider to ask if they do. If they do not, switch to a plan that does.

Of note, Kaiser began covering ABA after they lost a $93 million lawsuit in 2013. They are now complaining about the costs of autism therapy so watch for changes and delays in getting therapy.

3. See a therapist/marriage counselor/psychiatrist.

There will likely be some sort of mental fallout from the diagnosis, stress, and disbelief. Some data suggests 80% of couples with special needs kids end in divorce. Don’t be a victim, be proactive.

4. Figure out as a team how to tell the rest of your family.

It will be difficult. You will also have to decide how public you want to make the diagnosis of autism to work colleagues, acquaintance, friends. I feel like I made the mistake of being too open with his diagnosis and have received a lot of backlash. I felt my son was always blamed for things that were not his fault because he couldn’t defend himself.

5. Start a nest egg for all the time off, extra health care, and for your child’s future.

Know about the ABLE act and how to save in a tax-advantaged account for people with disabilities.

6. Go to support groups.

Meet people in the same boat and exchange tips. Meetup.com and Facebook are good places to start.

7. Read blogs about autism.

Here’s a list of some good ones to check out.

8. Get acquainted with what your school system has to offer kids with special needs.

Read about the Individualized Education Plan (IEP). Your child will have to undergo one every year and it will determine how s/he will be educated. Know your rights. Hire a special education attorney to make sure you get what you need. Many special needs attorneys conduct seminars to get your business, these can be quite informative and a way to get to know the attorney.

9. Hire an advocate if you are overwhelmed with what to do.

Here is an example of where to start.

10. Find a special needs estate planning attorney to craft a special needs trust.

Your child will likely receive state benefits in the future and you do not want any money you leave him/her to interfere with this.

11. Apply for Medi-Cal/Medicaid.

It will come in handy for many reasons. You may downsize your job since you are under more stress than other parents. Then at least your child’s insurance is taken care of. Also, if you get Medi-Cal, you can then qualify for respite care and In-Home Supportive Services in California.

12. Apply for respite care or IHSS.

Speak with your regional center specialists. Depending on your child’s abilities/needs, they will provide special funds for you to hire a babysitter to give you a break.

If your child is so severely disabled that you need to work part-time (<39 hrs) to take care of him/her, then you can apply for In-Home Supportive Services (IHSS) where the government pays you to stay home to take care of your child.

13. Take advantage of discounts available to families that have a member with disabilities.

For example, SoCal Gas has the CARE program which gives families 20% off their bill. Kidspace museum has free sensory mornings for special needs kids.

14. Most of all take care of yourself!

Having a child with autism can be very difficult. And unless you take care of yourself and stay mentally and physically fit, then your child will suffer.

You want to keep your child safe. It’s every parent’s first instinct. From bumps and bruises to Stranger Danger and developmental milestones, we think about all of the different ways that we can protect our children. Yet, many of us overlook an easy way to keep our children financially safe: a credit freeze for kids

What is a Credit Freeze?

A credit freeze basically prevents people from accessing your credit report. While this move may not provide foolproof identity protection, it will certainly slow down the efforts of identity thieves. How? Without access to your credit report, it becomes much more difficult to open new accounts in your name.

When your credit is frozen, you are still able to obtain credit reports. You can also temporarily lift the freeze if you need access to your credit report. Essentially, a credit freeze is a financial safeguard.

What are the Benefits of a Credit Freeze for Kids?

Most adults can appreciate the importance of protecting our identities. After the Equifax data breach, online security marched to the forefront of most of our minds. Even though many of us doubled down on protecting ourselves, freezing our children’s credit might have slipped our minds.

It’s understandable. Children don’t use their credit, so we don’t have to give it much thought as parents. However, that is precisely why it can be so beneficial to freeze your child’s credit.

Any kind of identity theft is problematic. Child identity theft is deeply troublesome because it can go undetected for years, even decades. As a result, children are the most vulnerable identity theft targets. In fact, a Javelin Strategy & Research Study found that over one million kids were the victims of identity fraud in 2017.

By freezing your child’s credit when they are young, you have one more tool to keep their identity safe. It can help you proactively protect them while avoiding the time, hassle, and cost that comes with restoring someone’s identity. Additionally, when it is time to have their credit unfrozen as they get their first job, plan to purchase their first car, or need to access their credit for some other reason, it’s an important teachable moment.

Steps to Freeze Credit for Kids

When you consider what easy targets children are for identity theft, a credit freeze is an easy choice. Unfortunately, the steps to freeze kids’ credit can be cumbersome. Here’s how you might go about freezing your child’s credit:

Know The Three Credit Bureau

In order to properly freeze your child’s credit, you need to contact each of the credit bureaus. While Equifax and Experian are both probably household names, TransUnion may not be. It is important to remember that you must work with all three credit bureaus.

Gather Up the Documentation

Freezing your child’s credit requires you to provide information about you and your child. To stay organized during this process, you will want to gather your personal documentation and your child’s documentation before you begin filling out any of the forms.

Documentation you may need includes:

- A copy of a government ID

- A copy of your Social Security card

- A piece of US mail with your name and address on it (utility bill, bank statement, insurance statement, etc.)

Documentation your child may need includes:

- A copy of his or her birth certificate

- Foster care certification – if applicable

- A court order for guardianship – if applicable

- A copy of his or her Social Security card

You will also be required to provide your addresses for the past two years.

Fill Out the Forms

After you have gathered up all of the documentation, you are ready to work with each of the credit bureaus. It is vital to remember that you need to contact each bureau. Some people mistakenly assume that since they only check their credit reports with one bureau, that one is enough in this case, too. It is not.

Experian has specific paperwork for you to complete. Once they receive the paperwork, they indicate that they will place the freeze on the credit report within three days. Equifax has its own separate paperwork for you to complete, and TransUnion requires you to send a written request along with the required documents. As you work through this process, you will want to make sure that you are paying close attention to the different requirements specified by each credit bureau.

My Experience Freezing My Son’s Credit

In case you didn’t notice, freezing your children’s credit can be a complicated process. Each bureau has a different set of requirements and parents are left hoping for the best. This process can take up your precious time and add unnecessary stress to your life.

Since I was the victim of failed identity theft, it was a no-brainer to freeze my son’s credit. However, I wanted something to streamline the process and get it done right. Coincidently, one of my old roommates started Credit Parent to make freezing your child’s credit a breeze!

Instead of having to manually mail all the required documents outlined above to multiple addresses. You gather the documents ONCE, scan them, pay the fee, and voila! Credit Parent takes care of the rest. Of course, all the information is stored securely and once confirmation from the 3 agencies is obtained, Credit Parent destroys your information.

We used Credit Parent to freeze Jack’s credit. Easy peasy.

We did run into a snafu with Equifax … along with about 20% of other parents trying to freeze their child’s credit. My first few calls to Equifax were unfruitful. Thankfully, Credit Parent enlisted the help of the NY Times to uncover Equifax’s practice. A few phone calls and about a week later, I received a letter from Equifax that my son’s credit report was successfully frozen.

Want to try Credit Parent? Use code MISSBONNIEMD for a discount!

Final Thoughts on Freezing Credit for Kids

Freezing your kids’ credit is not a decision to be taken lightly. After all, their credit is something that will impact them for the rest of their lives. Because your child’s credit makes identity theft much easier, a credit freeze is often a smart money move to make. The process can also be complicated. Either carefully following the specifications from each credit bureau or by using a tool like Credit Parent, freezing and unfreezing your child’s credit is one more way you can keep them safe.

Have you frozen your child’s credit?

This is a guest post written by XRAYVSN, a practicing radiologist located in the southeast working for a large multispecialty outpatient clinic.

Ever experience a divorce or are in the process of one? You'll appreciate this post. Although physicians, fortunately, have a lower percentage of divorce than the general public, the stakes are much higher when one does occur.

The main reason is that opposing counsel often views a physician as having deep pockets with great earning potential. In fact, I would propose that even your own legal team will take advantage of your profession by charging you the maximum they can for every billable hour they can think of. I have heard of divorces in the general public that were settled for less than $500 in legal costs. That amount would be blown through with just a mere two hours of my lawyer’s time.

The Storm Is Best Endured With Your Eyes Open

If a physician’s spouse happens to be vindictive and finds the right unscrupulous lawyer, you have the makings for a perfect storm. I, unfortunately, had to endure one of the storms of the century.

No story can be fully appreciated with a little background, so I think this would be a good place to start. I am of Indian descent. Although I came to the United States when I was less than a year old, I was still immersed in the culture associated with the “old country.” My father, a physician himself, underwent an arranged marriage to my mother. In cultures that employ an arranged marriage system, it is predominantly a family decision and the betrothed have little say.

The marriage was treated almost like a business transaction and the main purpose was to solidify the two families involved. A dowry was given to the groom as a token of appreciation and the size of this dowry reflected the stature of the groom in question. My father received a small house as his dowry payment to my mother given his high standing in society as a physician. In this case, my father and mother seemed to be happily married for almost 20 years before he passed away at the age of 50 to pancreatic cancer (I was 14).

That left the rest of my childhood and young adulthood to be raised by my mother. My mother made it known very early on that she preferred for me to settle down with a “nice Indian girl.” Although I predominantly dated in college/medical school outside of my race, I never was opposed to this and thought if it worked out it would be acceptable.

Entering my final year of radiology residency is when I first noticed the pressure from my mother build up. Looking back I know she was afraid that I would start making the “big bucks” as an attending and fall into that presumed lifestyle. She believed that the likelihood of me marrying an Indian girl would, therefore, drop precipitously. She started a global search using her connections from Canada, the United States, England, India, etc. Eventually what everyone deemed a suitable girl was found.

My Match And My Future Wife

She had just finished medical school in England and her parents were looking for her to get married as well. Till this day I feel the only reason we were matched was that we were “both doctors.” Part of the arranged marriage custom was the family of the potential bride would send her birth horoscope to the family of the potential groom. This horoscope is not at all like the ones you find in the daily newspaper. It is supposedly a very detailed account created for each child the moment they are born, chronicling the stars and planet alignments, etc. An arranged marriage would only go through if the horoscopes between the two parties “matched.”

One thing that was unusual in this case was that the girl’s parents in England insisted that instead of them sending over the horoscope for us to match, that my mom would send my horoscope to them to match. A bit atypical, but we complied. Well according to the folks in England, we had a high match and were suitable to get married.

We then began communicating for a few months primarily by phone and email. The next step was her mother and her visiting the United States where we would be introduced at my home since I was currently in a radiology residency. It was supposed to be a simple meeting with no commitments but it was anything but. The pressure from both sides was intense as my family also descended into my home for the occasion.

The Divorce

Before I knew it I had agreed to be “registered” to her which was essentially a formal agreement of getting married and within two months of meeting her, we were indeed married. I have written extensively on my blog about how marriage was absolutely one of the worst things I have ever had to endure. Suffice it to say that I quickly realized that I had made a horrible mistake.

The reason I waited so long to file for divorce, which I eventually did after being married 7 years, was because of my daughter. However, after seeing how miserable I was becoming and after a friend told me that I was doing more harm to my daughter by staying in an unloving marriage than divorcing, I decided to take the plunge. It was then I seemed to have awakened a vindictive beast in my wife. She then hired an unscrupulous, small-town lawyer who encouraged my wife to create as much destruction and turmoil as possible.

Between the two of them, I was always on the defense, defending my name and reputation against the wild and unfounded accusations. This bled over into multiple court jurisdictions including chancery court, juvenile court, civil court, and even federal court. I lost track of the number of full-day hearings I had to sit through. All the while the meter was running full tilt from my legal team as well as hers.

The divorce took 13 months to finalize and just a couple of months shy of my birthday. I lost track of the number of full-day hearings I had to sit through. It was the lowest point emotionally and financially in my life as any savings I had were wiped out to feed the ongoing legal costs. Some of the accusations I had to defend made me sick to my stomach. Knowing I was completely innocent but still feeling like everyone viewed me as a monster in the courtroom because of the lies the opposition put out there was difficult to sit through. It was only years later that my wife’s mental state deteriorated to the point where it was noticeable to the casual observer and she was appropriately diagnosed. But by then the damage had already been done.

A Divorce Is a Costly Ordeal – Mine Was $4M

I estimated that I had to spend over $300k of legal costs just for my defense. The judge also made me contribute $100k to my ex’s legal fees. I wish I could say that I was free and clear of my ex-wife the day the judge signed the divorce decree but alas this was not the case. My ex-wife and her lawyer still wanted more money and their greed caused them to file a $4 million dollar civil lawsuit and requested a jury trial. I wrote about that ordeal in detail here.

The result of this fiasco of an arranged marriage was irreparable damage in the relationship between my mother and me. I have never forgiven her for putting me through this and felt I was an innocent victim who only got into this situation in the first place by trying to appease my mother and not putting me first. To this day my mother still has not taken full responsibility in her part of this. She tries to make excuses and still has faith in the horoscope matching system, going as far as to say that the people in England must have made up the fact that the horoscopes matched and that is why they did not want to send the paperwork to us in the more traditional way.

It took me a long time to recover from the divorce and subsequent lawsuit, both emotionally and financially. I didn't even want to date for two years after my divorce because of the huge mistrust I felt. I am happy to say that these scars, while still present, have been buried deep down with subsequent great experiences. I have been in a long term committed relationship with a woman whom I very much love (and yes she is outside of my race).

Although it took a little longer, I was also able to recover financially. At the age of 47 many would consider me to be financially independent. I still work, however, as I am very conservative and would like to have a larger buffer in my nest egg before I consider retirement. The one thing that I discovered was that I had a lot of support from friends and co-workers during my ordeal and I leaned on them heavily to get me through the process.

Want to Share Your Story of Divorce?

Years later, when I started my blog and included the details of my divorce, I received a second outpouring of love and support which was very much appreciated. I thought it was so helpful in the healing process that I opened up my platform to others to share their stories of divorce (my Divorce and FIRE series) which would not only help them heal but also give others hope. I am always looking for my volunteers to share my story and if any are indeed interested, the details can be found here.

Many thanks to XRAYVSN for sharing with our community. If you'd like to connect with him on social media, you can on Facebook and Twitter.

Here are the 5 things every stay at home spouse needs to do to protect themselves financially:

1. Save for Retirement

Most retirement accounts are tied to a job. The only tax-advantaged retirement account available to stay at home spouses is the spousal Roth IRA. This is simply the stay at home spouse opening up a Roth IRA without needing to prove earned income. For this to work, the working spouse needs to have enough income to fund both Roth IRAs. Of course, many stay at home spouses often have part-time jobs or a side hustles. This opens up other opportunities for them. Whether they make a significant income from it or not, this will give them the ability to open and fund a solo 401(k).

2. Get Life Insurance

You may have read that life insurance is only necessary for income replacement. Therefore, conventional wisdom sometimes states that someone who does not bring in an income does not need life insurance. This could not be farther from the truth for a stay at home spouse. The stay at home spouse may not get a paycheck to stay home, but they are performing a job. In fact, they are performing many jobs. Consider this: In the event of their death, the working spouse, now widowed, will need to pay for high-quality childcare, maintain the household responsibilities, and perform the additional mental load of maintaining all logistics. And let’s be honest. I doubt the working spouse will want to return to work immediately after a tragedy. The surviving family may also require support in the form of therapy as well. Obviously, when you consider this perspective, life insurance is a no brainer. The stay at home spouse needs enough term life insurance to cover the cost of the above situation. Additionally, life insurance can also give the surviving spouse more choice. For instance, the spouse who worked full time outside the home might want the ability to go part-time since now there is one less spouse to help with the family. A.L, a physician and mother, said:

My late husband got term life insurance early as a resident. We got an amount that was supposed to get me through the rest of med school and residency. Now, it will be college funds for my 3 kids. I feel SO lucky we had it in place when he was diagnosed (and ultimately passed) with his brain tumor.

3. Get It In Writing

The biggest financial risk of being a stay at home parent is divorce. As a result, the decision to have one partner become a stay at home parent must be a mutual decision. Often, couples are already married when they come to this decision. It is important for the stay at home spouse to have protection against divorce. Being out of the workforce for years poses a real financial risk. For some fields, leaving is career suicide. He or she is sacrificing peak earnings potential and forgoing career advancement. They are also giving up building up Social Security savings and retirement contributions. A postnuptial agreement is a must for couples who choose to have a stay at home spouse to protect that spouse. And yes, that will probably mean an alimony provision. To better understand what exactly a working partner is sacrificing by staying home, the Center for American Progress put together this calculator that can help these conversations focus on numbers, rather than emotions.

4. Understand Disability Insurance

Most people have disability insurance tied to their employer. Additionally, most doctors should have private own occupation disability insurance. Stay at home spouses cannot purchase disability insurance unless they have earned income such as a home business. (Note: A quick google search finds one company offering such a policy, but it seems rare otherwise). But, if they had a private policy before staying at home, they can keep it. Also, once a spouse is out of the workforce for 10 years, he or she may not be eligible for Social Security disability insurance. This is another reason why a postnuptial agreement is a must for stay at home spouses.

5. Hone Skills & Consider Part-Time Work

Another important thing to remember with the finances of stay at home spouses is that the situation can change over time. As the kids get older and spend more time in school and activities, the stay at home parent will have more time to pursue outside interests. Those interests might be a hobby, a part-time job, or a side hustle. This is a great way for the stay at home parent to flex their brain in new ways and maybe even bring home some income. Remember if your stay at home partner does decide to monetize their side hustle, they have the option of opening that solo 401(k).

Final Thoughts on Finances of Stay at Home Spouses

We often talk about financial protection in terms of paychecks. But what do you do when your job doesn't come with a paycheck? Stay at home spouses perform vital roles for their families, which is why it is so important to give special consideration to their finances. Making these five considerations will keep your stay at home spouse protected financially. Do you have tips to share about stay at home spouses?

life and disability insurances. But do you have a will? Would your spouse and loved ones know what to do when you pass? Do they know how to access your accounts and other important documents? That's why you need a legacy binder. Death planning is, unfortunately, the high priority item that rarely gets done before your loved ones need it. It's probably due to a combination of thinking you will have plenty of time to get to it and avoiding thinking about your demise.

Start Your Legacy Binder with a Letter of Instruction

Your loved ones will reel from your death. Hopefully, you are adequately insured so they can take enough time to grieve and sort out your matters (and pay for counseling). Do you want them to be mired in tracking all your accounts, passwords, and other important paperwork? I'm guessing no. Make those logistics the easy part of dealing with your death. How? I recommend creating at the minimum a “Letter of Instruction.” This is an informal document (not the will) to guide the executor of your estate and your loved ones on important information that is in addition to your will. You can create this document yourself to ground your loved ones in all of the essentials.

What goes in a Letter of Instruction?

Make sure it includes the following information:

- Legal documents. Specify the location of all important legal documents they may need to handle your estate. These include the will (the original copy), social security card, birth certificate or passport, marriage and/or divorce papers, property deeds, automobile titles, etc.

- Financial information. Provide a list of all your financial accounts and account numbers: bank accounts, brokerages, retirement accounts.

- Passwords to your accounts. Make sure to include passwords for financial information, email, social media. I highly recommend using a password manager such as LastPass. This is what we use. In case you didn't know, Facebook allows you to name your legacy contact.

- Burial instructions. Tell your loved ones the exact details, including the name of the cemetery and plot location. Or if you desire to be cremated, be sure to include instructions as to how you want your ashes distributed. If you are a veteran, you may wish to look into being buried at a National Cemetery.

- Contacts. A list of family members (and your relationship to them–basically a family tree) and friends you would like to be notified of your death. Phone numbers and addresses are helpful in addition to email addresses.

- Policies. List all life insurance policies. Keep a copy of the policy page and the beneficiary designations. We use LastPass to store all our important policy pages.

- Tax information. Give the location of recent income tax returns and any necessary accounting information.

- Debts. Make a list of any outstanding debts.

- Professional contacts. Provide contact information for your CPA, attorney, insurance agents, etc.

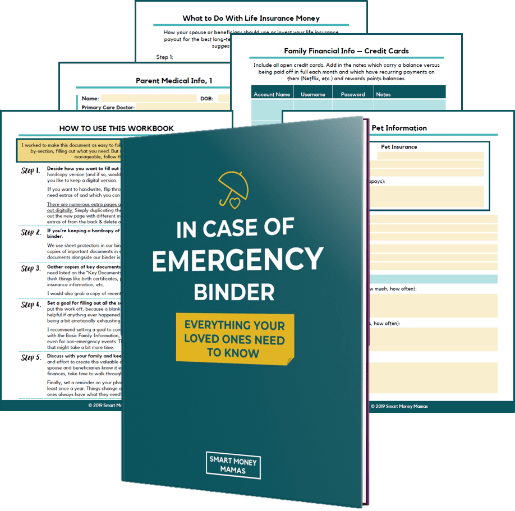

The In Case of Emergency Binder

If you're like me, you'd be more likely to do this with a fill-in-as-you-go workbook:

Chelsea of Smart Money Mama's developed this In Case of Emergency Binder (ICE) for her own family to get organized in the event of, well, an emergency. Emergencies include not only death, but a natural disaster or severe illness. I purchased her ICE binder last year and, of course, have been slow to finish this important document. Only a few weeks ago did I finally get in touch with an attorney about having our estate plan documents reviewed since we moved states over a year ago.

Make this one of your family's financial goals for 2019. And once it is completed, store this document in your estate plan binder and digitally. LastPass is not only a password manager for your whole family but it can store digital documents securely.

Final Thoughts on the Importance of a Legacy Binder

Whether you purchase a pre-made legacy binder, work with a legal professional to create one, or design your own, get it done. Not next year, not in the next six months. Make a commitment to yourself and your family to start your legacy binder right away. No one wants to think about their death, but it is a fact of life. A legacy binder protects your loved ones and should offer you the ultimate peace of mind knowing that your wishes will be respected and your loved ones will be cared for after you're gone.

Is your family prepared in the event of your untimely death? If not, get started!

Life Hacks post. She blogs at PracticeBalance.com about finding balance as a physician mom. She and her husband are financially independent. You can read her interview here. The other day, my 2 year old daughter asked, “Who gave us this house?” We both paused and looked at each other. “Um… No one. We bought it with our own money that we made ourselves.” This is the first time we had talked to her about anything related to money, and I’m sure it won’t be the last. As she grows up, she’ll no doubt deal with the marketing of products directly to her, comparisons to friends, cases of the “I wanna’s”… then ultimately management of her own earnings and debts.

Always creating and learning

Unlike some families where money is a taboo subject, we hope to have many money conversations with our daughter as she matures, because financial responsibility is very important in our family. We’ve worked hard over our adult years to become financially independent and free from any debt or mortgage, which has allowed us to both work part time. When I was a young girl, I never felt that my family was in a state of lack. But I also never grasped the mathematics side of money, the finiteness of it. That all changed when I became a mother. Although my husband had been equating money with life energy for many years at that point, I didn’t see it until I had this being in front of me that I wanted to spend all my time with. I had spent years, tears, money, and life energy to have her (due to infertility), yet she was priceless. Any time at work was suddenly time away from her.

One of the lessons I really want to teach my daughter is the idea of value. Value is relative and individual, as one person’s prized possession can be another’s throw-away item. Likewise, the way we prefer to spend our time (which ultimately equates to money) can vary drastically from person to person. I cringe when I hear people use the words, “We can’t afford it.” Kind of like saying, “I can’t eat that cupcake” or “I don’t have time to do ______”, it’s rarely true in a literal sense. You can if you want to, but you choose not to, for whatever reason. It’s a mistake made often by people in all financial situations, both wealthy and poor.

What harm is done in saying “we can’t”? It sets a tone of scarcity vs. abundance. The scarcity mindset keeps us from feeling we have choices or control over our financial situation. It places issues in a negative light, such that we make decisions out of fear and compare ourselves to others. On the flip side, being valueist means that we see the potential abundance in things. We make decisions from a place of optimism, because again, anyone can afford anything they inherently value.

Taking time to find the rainbows

Affording anything, however, must come with financial sacrifice in other areas of our lives. We’ve all seen examples of people driving around in very fancy cars despite meager earnings. I’ve been to third world countries where a family shack contains a large screen TV. Everything we buy is a choice and is conversely a choice in the opposite realm (against saving or spending on something else). How much is an extra hour a day with your child worth to you? Is it worth not having a cleaning lady, taking a 30% pay cut, moving to a smaller house? In addition, there are degrees of choice here; you can choose to NOT buy the nicest item you can afford. The common belief that everyone buys the nicest things “they can afford” leads to a false evaluation of success based on material goods.

Of all the things I value, time with my family sits at the top of the list. I hope someday my daughter will understand this concept when she wants me to buy her something that I choose not to buy. The best thing we can do is to live our lives in alignment with our respective values and provide an example for our children.

Don't miss out on future blog content, join my email list!

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]