Physician Wellness and Financial Literacy Conference aka the “White Coat Investor Conference” in Park City, UT. I got to meet WCI and many “online” friends that I had interacted with on Facebook, Messenger, and on the WCI Forums.

Jim opened the conference with “The State of Physician Financial Literacy.” He implored physicians to create the job we want now where we can work for a long time. Career longevity is more important vs. trying to “retire/reach FI ASAP.” As the conference unfolded we had two great lectures by my friend Nisha Mehta on physician burnout and what we can do about it. What I took away from the conference was to start an inquiry into what my ideal life would look like if money was not an issue. What changes can I make now to get there? (After all, I will not be FI for at least a decade.) And how feasible is it to create my ideal life now vs. “when I reach FI?“

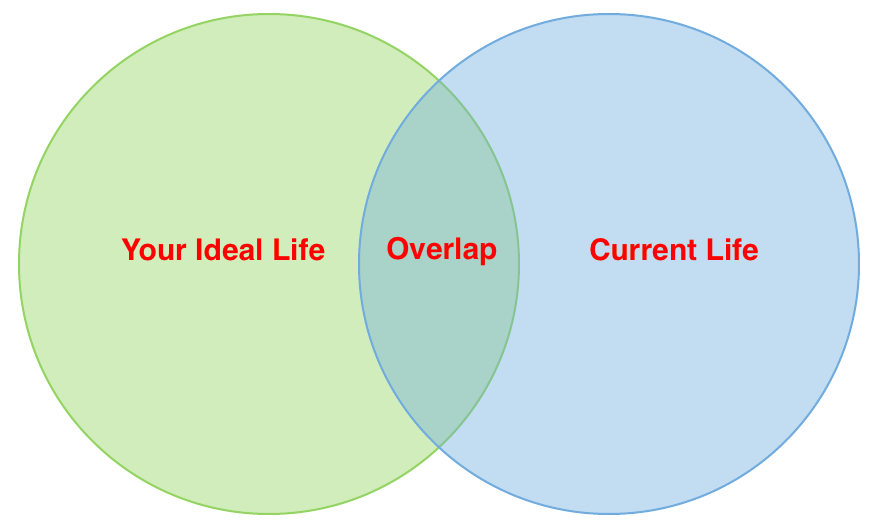

I subsequently stumbled upon this post by WCI where he presented a Venn Diagram as a visual to visualize the discrepancy between your actual life and ideal life. Obviously the higher the overlap the happier you will be. 60% is the % overlap to “be happy.”

Like WCI, I started thinking what my ideal life would like (the green circle on the left):

Like WCI, I started thinking what my ideal life would like (the green circle on the left):

- See patients 3 days a week with no weekends or holidays

- Walk to work or commute less than 15-20 minutes

- Start the work day after Eggy gets up and be home in time to play with him for a few hours before he goes to bed (and when he is older, start work after he goes to school and be able to pick him up from school)

- See no more than 4 patients an hour and run on time

- Work out 3 days a week

- Cook most meals for my family

- Have the freedom to take trips with my family 2-3 times a year

- Work on my blog ~ 10 hours a week to keep up with regular blog posts and such

- Since my current and ideal life has M & Eggy in it, I'd like M to also work 3-4 days a week and home by 4-5pm if he wishes to work that is.

- See patients 4 days a week with no weekends or holidays – Almost there!

- Commute 30-40 minutes by car – This is a HUGE improvement from my old job where the commute was 1-2 hrs each way

- 3 days a week I work 7-3pm – so I am up around 5:30am. Eggy gets up around 7:30am. 1 day a week I work 10-6pm so I get to spend part of the morning with him.

- The job is new so I am not fully booked yet but will likely schedule 6 patients an hour and I do generally run on time

- I work out 1-2 times a week

- Cooking has become almost non-existent

- We probably have the freedom to take trips but they need to be scheduled in advance and M's job isn't as flexible as mine

- Right now I struggle to put in regular time into the blog

- Right now, M works too much and works too late and for someone who isn't a physician is “on-call” quite a bit

Get the bestselling book - Defining Wealth for Women.

Recent Posts

239: What They Never Taught You About Money in Med School

Med school taught you how to diagnose disease-not how to create financial freedom. In this episode, I’m pulling back the curtain on the mindset shifts that completely changed my money philosophy-and my life. Spoiler: it’s not about how much you save or what you invest in. It’s about getting clear on what you actually want,…

238: Black Friday Hacks for High Earners: How to Shop Smart and Stack Points Like a Pro

It’s Black Friday season-are you ready to rack up serious points while scoring deals? In this episode, I break down my personal strategy for stacking points with Rakuten, maximizing perks from premium cards like the Amex Platinum and Chase Sapphire Reserve, and why NOW is the best time to apply for a new card. I…

237: Rethinking Wealth: Why Financial Flexibility Beats Retirement Planning

Most financial advice boils down to this: Grind for 30+ years. Max out your 401(k). Hope it all works out at 65. Yeah… no. In this episode, I sit down with Austin Dean, founder of Waystone Advisors, to explore a better way to think about money-one that prioritizes financial flexibility now, not just retirement later.…