Money

aunched a blog series where I interview other women physicians about their finances. This week, Chief Mom Officer interviews me as part of her “Six Figure Breadwinning Moms” series:

What’s the top three pieces of advice you’d have for someone just starting out in the workforce, struggling with their career, or just looking to improve how they handle their money?

- Live within your means. When your income increases, don’t increase your lifestyle in proportion. You lived on lesser income before, you can still do it.

- Learn the basics of personal finance and read at least one financial book a year. No one will care more about your money than you.

- The more money you have saved and invested wisely, the more choices you will have in life now and later.

Read the full interview here.

I also want to let you all know that Dr. Carrie Reynolds and I launched our bi-monthly podcast where we discuss all things finances. Dr. Carrie Reynolds @ Hippocratic Hustle (where she interviews female docs who are up to awesome things). You can find her podcast on iTunes. Our inaugural episode is here or search for “Hippocratic Hustle” on iTunes or you favorite podcast app. We discuss finance topics in a conversational way where we weave in our own experiences. We hope you enjoy it! We definitely are having recording them :).]]>

I am super excited to launch this series to the blog! The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our first female physician rockstar – Michelle.

Tell us about yourself:

I’m a 41 year old dual boarded family medicine physician and psychiatrist who is currently working full-time in administration in a community mental health position in Southern California. I am 9 years out of residency and my husband, a full time hospitalist, is 11 years out. We are raising our three young children (2, 5, 8) with considerable support from family, childcare and a housekeeper. I feel very lucky to have a stable and loving family unit since there was a time that my life was pretty chaotic. I had the unfortunate experience of getting married and divorced within a year during the first year of medical school. On the upside my ex and I shared no assets and no kids, so I was lucky to get a fresh start when I met my current husband “on the rebound” as they say. This time though I wanted to be really, really sure so we dated through medical school and residency before getting married. We started our family when I was just out of training at age 31. We soon found out that starting a family though with two overworked, somewhat old physicians isn’t always a romp in the sheets. We ended up needing IVF to conceive each of our three babies. The cost of IVF was staggering since it wasn’t covered by insurance. We learned early on in our attending careers that we were not going to be the stereotypical rich doctors. Between a combined total of $300K in student debt and baby-making costing $25K a pop, our finances were tighter than our incomes would suggest. We could have made the decision to move to a low cost area, but both my husband and I are committed to paying our sun tax to live in this beautiful city. To do so, we’ve had to embrace that budgeting and planning our finances is part of the deal. I’ve packaged our story here pretty neatly but there were many twists and turns to get us to where we are today. Having said that, I’m very happy with many of the life choices we made along the way. I’m a dual-trained FM/Psych physician and healthcare integration is all the rage these days. There have been many good career options for me and now I’m in a fairly well paying administrative position (for public sector work.) Although I’ve lost much of my idealism of my early years, most days I feel like I’m doing the best I can to contribute to my community and serve patients that are usually largely underserved.Did you graduate with student loans? How much & what are the interest rates?

I went to a private college on a partial athletic scholarship. The other half was fully supported by my parents. I had no debt out of college. I paid for a state medical school using loans and really wish I had been more mindful to take out less. i graduated with $130K in loans. I was one of the lucky ones to come out at the right time and consolidate to a 2.8% interest rate with T.H.E loans which were great to work with.How fast (or not) are you paying them off?

I chose a 30 year payment plan which in retrospect was ridiculous. I thought with interest rates so low I should do it that way and could always pay ahead. I wasn’t motivated to pay ahead until recently. On the upside working in the non-profit sector has afforded me many loan repayment opportunities. I’ve had 50K paid back tax free by State loan repayment and over the next 2 years will have another 15K paid back. I’ve stopped paying and just keep applying for loan repayment programs.Financial aspects of kids

When did you have them?

As I mentioned above we started having kids just after residency. I’ve done okay on my career trajectory however my maternity leaves have delayed raises and I lost out on advancement opportunities I really wanted. I was actually told by the COO (and she is female!) “We thought of you for that position, but then I figured with your young kids the timing wasn’t good.” I think she was trying to be thoughtful, but boy did that make me mad!Are you planning to fund their college expenses?

We have a Utah 529 plan for each of our three kids. We started funding them are early ages, but we really wish we would have started them even before they were born. We’d like to fully fund the equivalent of state tuition, but we are funding our retirement as the priority. We’re adding extra as we can to get to our goal.What are your child care expenses?

We spend a small fortune on childcare and extra help with everyday household upkeep. I’m possibly the least domestic person I know and I outsource everything I can. We have hired a woman who helps with the kids and the general household upkeep for 23 hours a week. I’m just a doctor and a mom. I definitely don’t keep house. I have arranged my life to dedicate my time to the roles I enjoy most. It costs an arm and a leg, but it is worthwhile so that I get the downtime I need. Our kids also go to daycare. I love the structure and consistency of the hours of daycare. I love that the kids have a social group and can make friends there.Are your kids in private or public school? What is the cost including after care if needed.

Our kids are in public school. We choose our home based on where there are good schools. The housing prices are higher but at least that money is invested in the house. I’ve never had a good sense that private school gave any real life advantages so I figure we’ll only consider private school if there is some special consideration along the way for one of our kids.Financial aspects of marriage

Are you married?

I joke around and say that my first marriage didn’t stick. It was over in a blink while my head was buried in my books while my ex-husband was off with one of his co-workers. I left the situation as fast as I could and just took a few belongings off to my own apartment on campus for $125 per month that my family paid for a few months, so I could sort it all out. That was the best decision of my life right there. I lost everything to gain everything I have now. I met my current husband in medical school – I've made a much better selection!Did you get a pre-nuptial or post-nuptial agreement?

We didn’t. We had no assets.

Do you and your husband agree on finances?

My husband and I were both raised in fairly affluent (upper-middle class) communities. However there was big difference in the way our parents talked about money. My husband's parents basically never wanted their kids to be worried about money and wanted their kids to know that they would always support them. My father-in-law lost his father at the age of 13 growing up in Iran and found himself fending for himself at a young age. Fortunately he was taken in by other family members, but the fear of poverty was something he never wanted his own kids to experience. My father by contrast, was very frugal and rarely spent money on extras though we knew we had money and lived in a nice area, with a nice house and good schools. I was told not to order a drink with dinner at restaurants since that was too expensive. I was told many times “We don’t have enough money for that.” So needless to say, my spending patterns are very different from my husband. It was never much of an issue because we both made good salaries and didn’t really understand or see that we weren’t saving for our future or the futures of our kids. It wasn’t until I sort of randomly fell upon our female physician finance Facebook group that I started learning how little I knew. We had been working with a fee-based Financial Advisor up until that point and not once had she pointed out that our spending patterns were awful and not once was she clear with us that we needed to save more than we were. Various members posted some links to the White Coat Investor and I’d have to say that was a pivotal moment in my financial life. At that time I ordered the book and really have been on a learning journey since. This is sort of where the rubber hit the road for my husband and I. Up until that point his spending didn’t worry me since I figured “We are doctors, we make good money, what’s to worry about.” I started learning about personal finance and then I started getting very concerned that my husband and I were not going to be able to retire until age 90 and our children would get little to no support for college. My husband wasn't very interested in personal finance and to this day he is not. We do have a very good relationship and he trusts my intelligence and general ability to navigate life. So when I started to explain that we were woefully behind in our retirement and college savings, he did believe me. The trouble is that he wasn’t very interested in changing his spending. So I started reading some articles about how to get your spouse on board with finances. I was able to get him to agree to once a month couples meeting about our finances. During the meeting I’d outline our finances and show him the various calculators showing where we needed to be. He started understanding that where we needed to make some changes. He still had no real interest in reading or doing our budget, etc. I asked him how did he think he could cut back his spending and he said “Well, when the money is gone I always stop.” Fortunately, he didn’t have an issue with credit card debt. So from this we came to the agreement that I’d manage our finances and that we’d get him a pre-paid debit card. We put a fixed amount of spending money on the card each month and when it is done he stops. All other family spending are driven by our budget which I created and maintain (shout out to the world’s best budget software YNAB!!) In 5 months time from starting YNAB and my husband’s debit card we were funding a lot more in our retirement accounts, contributing more to college accounts and our cash reserve has quadrupled. I think my husband secretly likes the security of knowing we are on track financially and that our kids will be well supported in college. [Wow! How inspiring is this!]If you are divorced – what have you learned financially from this, and what advice would you give to unmarried women planning to marry?

I learned that I was extremely lucky to have family support to get me out of a bad situation. My advice to all women married or not is never be in a situation where you don’t have your own access to emergency funds. I was a first year medical student living off of loans and had no emergency pot set aside for me to access.Are you the breadwinner?

No, we are equal financial partners.Have you experienced a financial catastrophe?

See my first marriage & divorce, above.

General Finances

What’s your FI (financial independence) number?

FI #: $4 million. My goal is to reduce our lifestyle consumption in hopes for the number to be lower. I want to live more simply but haven’t yet achieved that.Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

For years, I thought “handles the finances” meant who does the bills. And that answer would have been my husband. He still “does the bills” which these days means he sets up the accounts for automatic payments. These days though I understand finances so much better than I used to. I don’t manage the autopay as a part of doing the finances, but I can comfortably say that I do 90% of our financial planning. My husband does the taxes. We had a financial advisor for about 3 years and although I can credit her with introducing me ideas, I would have been way ahead of where I am now had I learned the information on my own or used a fee-only FA rather than a commission based FA that I used.What is your net worth?

Well, let me go peak at Personal Capital! If I take out my 529s, we have $500K not including equity in our home. The approximate the equity we have in our home minus the mortgage would probably be an additional $250K.How are you saving for FI/retirement?

My husband has a pension plan, 403(b) and 457(b). For years, we didn’t know that he wasn’t maximizing his space. When I looked last year and figured out that he wasn’t, we changed that to maximize the $36K (plus his pension contribution.) We are not yet funding Roth IRAs. We have his funds invested in a low fee target fund which is his lowest fee option. We make the allocation more aggressive by pushing out the retirement day. I currently have a pension plan, 401(a) and a 457(b). I am contributing $9K yearly to the pension, $41K into my 401(a). I’m not yet utilizing my 457(b) or funding a Roth IRA.One thing you wish you knew:

I wish someone would have told me that there are more bad FA than good ones. I really wish I would have found a good one from the start. I also wish someone would have told me that learning about this doesn’t make you greedy and money centric. It just means that you’ll be independent and not a burden to your children in future years to come. That’s not a selfish thing.Do you have insurance?

We have solid life insurance and umbrella insurance, but really have been risky about not taking out disability insurance. Our rational is that if my husband gets disabled we could manage on my incomes (which is realistic, finally.) And if I get disabled we can live on his. If we both get disabled we’re screwed. I feel comfortable without it for myself (even if I ended up single again) since I’m non-clinical and have an office job. Most office job folks just use their employer's disability insurance. My job isn’t any different than a lawyer or or other professional so I just don’t feel strongly about having job-specific policy now that i’m non-clinical.What does FI/retirement mean to you? What does it look like?

FI means that I don’t have to work any more. I imagine that when I hit this number I will reduce my hours to just the amount that I feel like working. Then I imagine I will want to stop all together if my kids have kids. I’m hoping to be a stay-at-home-grandma if my kids would like help with raising their own kids since I was a working mom. I’d love to be present for my grandkids and support the careers of my children.Do you give to charity? If so, where and why?

Not much just here and there for work and school fundraising events.Any parting words of wisdom?

We all carve out time in our busy lives for our priorities. I wish learning personal finance would have been higher on my priority list at a younger age. I had the notion that somehow learning about money was only of the money-hungry, superficial types. I wanted to be above that. In retrospect that was so naive.And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I loved reading Michelle's story and I hope you did too. I was totally inspired about reading how she was able to take control of her and her husband's finances and get on track for financial freedom.]]>

Eggy on the way, we've had to do some estate planning. I'll be honest: I found trying to understand and interpret estate planning and legalese way more challenging than learning personal finance. If you feel the same way, then you'll want to stay tuned for my series on estate planning in “plain English” starting with this post. Today, I'm going to discuss the estate plan basics and define some basic terms you need to become familiar with.

The Vocabulary of Estate Plan Basics

Below, you will find some of the most frequently used terms in estate planning. In addition to breaking them down in simplified English, there are also helpful links for additional reading.

Know Your Situation

Before we dive into the estate plan basics, the first thing you need to do is take inventory of yourself. Specifically, you need to understand your personal situation. Who exactly are you looking to protect? Someone who is single is going to have a very different estate plan than someone who is married with a blended family.

Let's start with me for an example. Our situation is more complicated than the common “(first) marriage with kids” scenario, meaning first marriage, no prior divorce and all the kids are theirs.

Our situation: We are not married. I've never been married. M has been married before and has a son from that marriage. Eggy will be our first child together. We do plan on getting married, just not in the near future.

We just finished drafting wills, power of attorney, living wills and healthcare proxies with a lawyer in NY. Please note and keep in mind that estate laws are state specific and some or all documents will need to be updated/redone if you move states and as your reach life milestones.

Last Will & Testament

All couples with minor children need a Last Will & Testament or Will. Why? Because in the Will you name a guardian in the (highly) unlikely event both you and your spouse pass before your kid(s) are adults. Otherwise the court makes that decision for you!

So, if you don't have a Will (and both spouses each need their own wills, they generally mirror each other), then you are basically saying you're OK with having the court decide guardianship for your minor children. I am pretty sure you wouldn't be OK with this.

You can also name a backup guardian in case the first named guardian cannot carry out the duties.

Executor

Your executor is also named in your Will. That is the person who will carry out the wishes of your Will. If you're single (kids or not), you'll want a Will unless you have little to no assets or only assets that bypass probate (discussed below).

Intestate

If you die without a Will, this is called intestate, and your “stuff” will be divided up according to state law.

Probate

Most Wills will needs to go through probate. Probate is the name of the legal process for settling a testator's (the deceased) estate.

The probate process involves a probate court, your named executor and a lawyer.

A lot of things do not need to go through probate, however. You may have heard that it is “good” to avoid probate. Probated wills incur costs against the estate – court fees, lawyer fees, executor fees (if applicable) and time.

Every state's probate process is different so you'll want to become familiar with the general probate process in your state. Retirement accounts (401(k)s, 403(b)s, IRAs, Roth IRAs, etc) DO NOT go through probate unless no beneficiary has been named. The same is true for bank accounts and life insurance proceeds.

Beneficiaries

Definitely make sure you have named your beneficiaries correctly. This is not as straightforward as it sounds.

For 99.9% of us, our spouse will be the primary beneficiary for all of these. In fact, if your spouse is not the primary beneficiary of your 401(k) (or a similar work qualified retirement plan), then you need notarized permission from your spouse to do so.

Let's say you have 2 children named Amy and Tom for the next example. The secondary or contingency beneficiary is logically 50/50 split between your two children.

Let's go a bit further and say Amy has 1 child and Tom has 2 children.

If, at the time of your death, Amy has passed as well, then guess what? All of it goes to Tom and Amy's child is effectively cut out of the estate. This is probably not what was intended. The intention was for Amy's share to pass on to her kid.

Per Stirpes

In order to do this, you need to name Amy and Tom and add the phrase per stirpes after their names. Per stirpes means that items are distributed to each family branch. Some states do this slightly differently so be sure to understand your state law on this.

Final Thoughts on Estate Plan Basics

Hopefully, the first post in this estate plan series took out some of the guesswork behind vocabulary that is often used with estate plan basics.

A much needed addition to the official documents is a “crib sheet” for your loved ones such as In Case of Emergency binder. In the meantime, check out this great book on estate planning:

![]()

[ Disclaimer: Please note that some of the links above are affiliate links. This means that I may receive a commission if you purchase through one of my links. I highly recommend all of the products & services because they are companies that I have found to be helpful and trustworthy. I use many of these products & services myself. ]

View from my previous apartment in Williamsburg, Brooklyn, NY on Christmas Eve[/caption] It's definitely easier to attain financial independence (FI) faster when you live in a LCOL (low cost of living) with a high income. Is it out the window when you live in a HCOL (high cost of living) – like Brooklyn, NYC (where I live) or the San Francisco Bay Area? Of course not. But some thing(s) need to give if you want to reach it in a reasonable amount of time. So, how are we able to put away > $80,000 a year towards FI, pay down loans aggressively, be able to afford child care in this expensive city AND still be able to enjoy life? 1. We keep housing costs as low as possible This is probably the largest ticket item for those of us in a HCOL. A modern (meaning it includes a dishwasher and laundry in-unit) 2 bedroom apartment in a great part of Brooklyn will be a minimum of $4,000 for likely < 1,000 sq. ft. Manhattan? Try $5,000 and likely much more for any decent neighborhood. What about buying? Try $1 mill for a tiny 1 bedroom (again, if you're lucky) and upwards to $2 million+ for a 2+ bedroom apartment. That doesn't include the monthly maintenance fee. Want a parking spot? Extra.

“If you will live like no one else, later you can live like no one else.” – Dave Ramsey

I am not a huge fan of Dave Ramsey, but his basic mantras will serve most people very well. M and I live in a tiny apartment (730 sq ft). M owns this apartment and luckily bought in the early 2000s for a whopping down payment of < $20,000. No, there isn't a missing zero. It is a true two bedroom, one bathroom apartment. We have a dishwasher and our own laundry – which in NYC is a luxury. With the upcoming baby (and our bonus son that we have sporadically during the school year), many have told us that we have to upgrade. Nope. My brother and I attended high school living in a similar apartment (sharing a room). This won't be “forever” but we are doing our best to stay here until my student loans are paid off by end of 2020 or earlier. We will finish paying off M's car loan (I drive to work) in the next month or so leaving just the mortgage on his end. We street park (free). Our total housing costs (mortgage + taxes + condo fee) is ~5% of our 2017 annual gross income.

2. We chose a financially like-minded partner

Aka choose your spouse wisely. OK, so we didn't exactly do this on purpose, but sorta (at least on my end)? About 1-2 months into dating M, I asked him about his finances. Specifically, I asked him how much money he had in his retirement accounts and what debt(s) he had. I also knew that he wasn't a big spender. As things became more serious we discussed our shared financial goals for the present and future. We did this before we got engaged.

2. We make savings automatic

My 403(b) and 457(b), and his 403(b) contributions are automatically deducted from our paychecks. We never see the money. Since these are all pre-tax contributions, we don't really miss it vs. not doing this automatically and seeing if “we can afford to save.” We do our best to fund the Roth IRAs early in the year so we don't miss it and are not tempted to spend the money instead.

3. We (mostly) stick to a budget

I use YNAB to budget. I haven't added M's expenses yet but I am able to track our overall spending in eMoney (web based software we use with our FA). I've been using YNAB for over 2 years now. I was a spendaholic and this is my rehab.

4. We don't buy (much) stuff

We aren't minimalists, but we both agreed that stuff does not make us happy. We also don't have room for the stuff anyway (see above).

5. We have decided on the 1-2 things we really enjoy and don't hesitate to spend on it

Luckily, we both really enjoy eating out & cooking good food and traveling. Sure, we could nix all vacations and eat rice and beans until loans are paid off but it's important to enjoy life now too. We do try to meal plan for the week and we generally bring lunch to work. We budget for all of this.

[caption id="attachment_1137" align="aligncenter" width="402"] Lots of wristbands to get into Panorama 2016[/caption]

Lots of wristbands to get into Panorama 2016[/caption]

Another thing we both really enjoy is attending live concerts of our favorite bands (mainly indie pop/rock/some electronic). Luckily, NYC is almost always a stop on anyone's tour. Not to mention home of some of the big summer festivals. Confession: I have not paid for a single concert since M & I met. One of the big perks of M's job is free (and VIP) access to almost any concert we want to go to. We attended Panorama last summer. In the past several months, we have seen the Shins, the xx, Sigur Ros, Frightened Rabbit, M83, Tame Impala, Sia, the 1975s, Mumford and Sons, and Flume to name a few.

Bottom line – we live well below our means.

How are you making it in a HCOL? Comment below.

]]>

Last month I spelled out how we are investing our money in 2017. I mentioned there were some moving parts – namely, M was unemployed and we knew, at the time, that I was (newly) pregnant. Now, M has a job (yay!) and looks like this pregnancy will stick, so now we can do some real projections for 2017. Our asset allocation will remain the same.

This year our total “retirement” contributions will consist of:

This year our total “retirement” contributions will consist of:

- $18,000 my 403(b)

- $20,800 employer match + contribution into my 403(b). Currently 20% vested. 40% vested as of August 1, 2017 so actually $8,320

- $18,000 my 457(b)

- $5,500 my Roth IRA

- $18,000 his 403(b). No matching at this time

- $11,000 his Roth IRA (his first! For 2016 and 2017)

- Other sources:

- A very modest amount ~$1,000 into my solo-401(k). Yes this blog likely won't lose money this year 🙂

- ~$5,000 his solo-401(k) – he has some 1099 income this year

M and I are pleased to announce that we are expecting a baby boy this fall. We have nicknamed him “Eggy” – it means baby in Korean. As you know, you cannot exactly plan when you become pregnant. Honestly, we were not sure if things would happen au naturel due to my age so IVF was a possibility. Luckily my current job includes 3 cycles of IVF as a benefit but it is still not 100% covered. I know many ladies who have spent a small fortune on getting pregnant. So here are a few things I have learned, financially, about trying to get pregnant and trying to plan for leave and childcare:

- Insurance coverage: Make sure you know what your insurance plan will cover and not cover and what deductible you'll need to meet, if any. Even if your insurance says “maternity is covered,” it may not cover all the tests. My costs: $40 (co-pay for the first visit only) is what my total out of pocket costs will be, including the delivery. This assumes I use an ob-gyn within my health system (I am) and that I deliver at one of their hospitals (I plan to).

- Maternity Leave: Think about how long you'll want to take for leave and what leave, if any, will be paid. This is a highly personal decision, but I have yet to meet someone who said they took too much time off. Unfortunately, paid maternity leave is not the norm in the U.S. If you have unpaid leave at least you'll have approximately 9 months to save up for this. My leave: I get 6 weeks paid leave (at my base salary) or 8 weeks (c-section). I can also use unused vacation. I will have at least 2-3 weeks of unused vacation to get to at least 8 weeks paid. I am taking at least 3 months off. So that means at least 1 month unpaid, possibly more. Since I only really need ~60% of my take home base salary, this won't be a huge burden on us and we will have more than enough saved to cover this unpaid time.

- Maternity clothes: Unless you only wear stretchy pants and dresses, you'll need at least a few staples. I do wear scrubs a few times a week to work so I did not have to buy a whole new work wardrobe. Gap Maternity is pretty inexpensive and I was able to use a 20-40% off coupon when ordering online. It also helps that it'll be mostly warm weather during my pregnancy so I can keep wearing dresses.

- Baby stuff: I am totally cool with second-hand everything. And due to space limitations of an NYC apartment, we definitely do not want too much “stuff.” Between a baby shower, a very excited grandmother-to-be, M's sister's hand me downs – we should have most of the basics for almost free. I have even scored a free Mamaroo and Ergo carrier already. I won't be shopping at baby boutiques for clothes.

- Post-partum help: If you don't have family around you may want to look into outsourcing certain things (clean and cook, etc) so you can focus on mothering. Baby nurses and night nannies are common in NYC – definitely a luxury – but a savior when you're sleep-deprived. Post-partum doulas are also a great idea, especially for first time moms, to show you the ropes, help you ease into breastfeeding (most are breastfeeding certified counselors), and help you take care of you while you recover from delivery. The U.S. is a bit strange in that moms are expected to recover and go back to work ASAP. Too bad there aren't any post-partum spas here like Korea. My plans: M will take 2 weeks off to help. I'm planning on hiring a post-partum doula for a few sessions for the above reasons. After 2 weeks, I'll be with my mom for a few weeks – letting her carry out a Korean tradition of taking care of a new mom. Slightly modified as I'll be able to shower :).

- Childcare: This blog is geared towards female professionals, so most of us probably won't be stay at home moms. I'd be lying if I said I wasn't worried about the cost of childcare! The going rate in my neighborhood is ~ $17/hr for a nanny. At this time, I prefer having a nanny for the first 6-12 months after I return to work. The convenience of someone coming to us vs. one of us packing up the baby and walking to a daycare (at least a 10-15 min walk – won't be fun during winter). Also, babies and kids often get sick in daycare and although M's work is more flexible, we don't want to deal with that. Right now, we are planning to have a nanny for 40 hours a week over 4 days and my mom for 1 day a week and for backup. We are *gulp* preparing to spend at least $3,000 a month in childcare. Unfortunately, daycare isn't much cheaper and with the convenience and flexibility of a nanny, this was a no brainer for us. After 6 months or so, we will reassess.

- Saving for college: It's never too early to start saving for a little one's college. You may recall that I started a 529 last year in anticipation of starting a family. I get a small state tax break for funding one so it was a no brainer to get started.

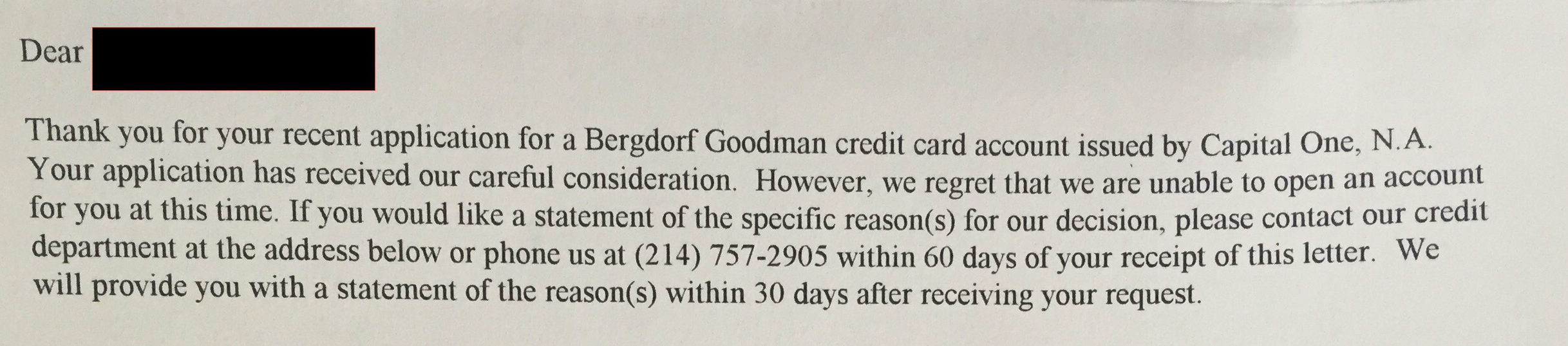

I was almost a victim of identity theft.

I did not apply for this card:

For those of you not familiar with Bergdorf Goodman – it is a high-end luxury department store in NYC – think Gucci, Prada, Chanel. Unfortunately, not a place I will be shopping at anytime soon.

I checked on Credit Karma and there it was – a hard inquiry on Equifax dated around the same time of the above letter from this department store. I also found another hard inquiry that I did not initiate. I took this opportunity to thoroughly review what accounts are open and make sure they were actually mine. Phew – all good. But I did find 3 old store cards that I haven't used in years. I went ahead and closed them.

I then froze my credit at all 3 agencies – Equifax, Transunion, and Experian.

What does freezing credit do? It prevents unauthorized use of your credit to open credit cards, mortgages, etc. unless you/they have your pin. This pin is issued when you freeze your credit. When you need to open a new card or mortgage you simply unfreeze or thaw your credit. Best if you call the bank or institution and find out which agency they will use first so you only need to thaw one agency. There may be a fee to thaw – but negligible compared to the headache and time needed to undo fraudulent activity.

So, even if someone does get your information they will not be able to open any lines of credit without this pin. Guard this pin! You will not be able to do anything without it. Make copies, upload to a secure cloud etc.

Freezing your credit has no impact on your credit score. Freezing and thawing credit is also state specific in terms of how long it will stay frozen and fees to freeze or thaw.

Check out this excellent freeze/thaw guide for links and info on how to easily freeze your credit. Please note that freezing credit does not affect a theft's ability to steal and use your actual credit card. Thankfully, this is much easier to deal with.

And, don't forget to freeze your children's credit! Yes the thieves are even going after them.

If you're eligible, you can take things further and obtain a pin from the IRS so that no one else can file in your name. Yes it happens, and I can assure you this is a much bigger PITA to deal with. Unfortunately, at this time, you need to be eligible to obtain one:

- You receive CP01A Notice containing your IP PIN, or

- You filed your federal tax return last year as a resident of Florida, Georgia or the District of Columbia, or

- You received an IRS letter inviting you to ‘opt-in' to get an IP PIN.

I am not eligible at this time. Hopefully the IRS will soon let anyone obtain a pin to protect themselves.

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]