personal finance

This is a repost of last year's financial tips, updated for 2019!

Can you believe the year is almost over? With just a few short months to tie up most financial loose ends, here are some year end financial tips you'll be sure you won't want to miss.

Check out the companion podcast (from 2018) over at the Hippocratic Hustle!

Be Sure To Max Out Tax Advantaged Retirement Accounts

… If that was one of your financial goals.

You may be surprised to learn that we no longer max out all of my available tax advantaged accounts as of this year. Our 2019 goals for tax advantaged retirement accounts were to max out our HSAs and Roth IRAs and get the free match from our employers.

Hopefully you've already set up your work retirement accounts to max out along the year (aka dollar cost averaging). Or better yet, you front loaded them and are done for the year! Here are the accounts you may want to double check:

Work retirement accounts

Work retirement accounts such as 401(k), 403(b), and 457(b) generally have a deadline of by your last paycheck of the year. It can also take 1-2 pay cycles for any changes you make to your contributions–so do this ASAP if you need to increase your contributions. Don't forget to reset this in January unless you want to front load the accounts.

Roth IRA

Don't forget to fund your Roth IRA! Most physicians will need to backdoor it. You do have until Tax Day in April 2020 to fund it, however, it is cleaner if you do the IRA contribution & conversion this calendar year. This is due to how you fill out Form 8606 with your taxes.

Here's the short version of how Form 8606 works: You report the contribution to the traditional IRA on the tax year (2019), but you report the conversion (from traditional IRA to Roth IRA) in the actual year you did it. So for example, if you wait till January 2020 to backdoor for tax year 2019, you'll have to report this transaction on Form 8606 in 2019 and 2020. Not a big deal, but you'll need to keep track of that or make sure your CPA does for you.

Solo-401(k)

Are you self employed or do you have a side hustle? There are two things to know:

- You have until 1/15/20 to contribute your employee contributions.

- Then, you have until tax day April for the employer contributions for the solo-401(k).

If you don't have a solo-401(k) but want to, you have until 12/31/19 to open one – so get on it!

SEP-IRA

If you're a procrastinator, then you'll need to open a SEP-IRA. You have until tax day extension in October 2020 to open and fund one for tax year 2019.

HSA

If you're lucky to have access to a Health Savings Account (HSA) and are using it as a Stealth IRA, you have until Tax Day in April 2020 to fund one. Most folks will fund one via paycheck through work. I self fund it and contributed to it in one lump sum at Lively. Don't forget to invest the money inside the HSA as well. Lively custodies with TD Ameritrade.

Take Advantage of Tax Loss Harvesting

Tax Loss Harvesting (TLH) is a way to capture losses in your taxable or regular brokerage account to reduce your tax burden. The current limit of losses you can claim on your tax return is $3,000. You can carry forward losses > $3,000 to use into future tax returns as well.

Speaking of investments, make sure you know when to rebalance your portfolio. I recommend doing this once a year and definitely not more than twice a year. Pick an annual date to do this.

Be Smart About Charitable Donations

The new Tax Law (as of 2018) makes it more difficult to itemize deductions since the standard deduction is much higher. Hopefully no one donates just for the tax write off. The best way to donate and get a tax break is to lump your donations every other year (or more) so that you are able to itemize deductions.

A great way to do this is to open and fund a Donor Advised Fund (DAF). Why? You take the tax write off the year you contribute to the fund, then you're free to donate to any charity you'd like without having to keep track and save receipts for tax day. You can also donate anonymously very easily via a DAF.

Use FSA Money

Don't forget to use up your Flexible Spending Account(s). Some plans will let you carry forward up to $500 to the following year. However, most of the plans are “use it or lose it.” Your plan can also offer a two and a half month grace period (March 15).

Bottom line – read the fine print of your FSA plan. The same applies for Dependent Care FSA plans. I wonder where the lost money goes – anyone know?

Start or Review Your Estate Planning

There is no end of year deadline for this per se … however this ends up being an non-urgent item on the to-do list for many people.

Create A Will

If you're reading this and you do not have a will – what are you waiting for? Perhaps you elected a legal plan through your employer and the deadline to use it or lose it is coming up. If you are married and/or have children, having a will is a must to elect a guardian in case of your early demise. Otherwise the state will pick for you.

Secure and Safely Share Account Access

Along these lines, if you or your partner passes, do you have access to his/her accounts, logins and passwords? First, you'll want to make sure you have Power Of Attorney. This is not valid upon death but many things can happen where you'll need access to accounts legally.

For password and secure digital document management I recommend a program like Lastpass. For most folks, the family plan will be appropriate. This allows the whole family to use Lastpass to manage passwords. Lastpass can also generate secure passwords (you're not using the same password for all your logins, right?).

You can also use it as a secure digital vault – I upload copies of important documents such as driver's licenses, passports, social security cards, life insurance policies and other insurance policies. I essentially use it as a digital death book.

For those that prefer the paper route for this, check out Mama Fish Save's ICE binder – In Case of Emergency. This is a templated PDF that guides you into documenting all the things you'll want your loved ones to have access to when you pass.

Smart End Of The Year Financial Tips

Make a plan to implement these tips before the end of the year. That way, you'll finish 2019 strong. With only a few short months left in this calendar year, make today the day that you get started.

You can also sign up to grab your guide to the 4 Steps to Creating Wealth. After all, who doesn't want to start the year wealthier?

Join the Wealthy Mom MDs Facebook Group to continue the conversation!

This is a guest post from my fellow woman physician blogger, Dr. B.C. Krygowski. She's a palliative medicine physician who discovered FI & Frugality as a way of life. She blogs at bckrygowski.com, and she has ten tips that any high-income earner should try out to add more frugality to their lives.

# 1. Look into Home Exchange.

Home exchange saves me serious money because I can swap homes and cars with other families for overseas vacations.

# 2. Schedule a half-day to sit down and figure out your priorities.

Do you say you want to be mortgage-free more than anything, yet you continue to take four (or more) exotic trips a year? Your life actions say something different than your words. Maybe consider cutting the exotic trips down to one or two a year and put the money you’ve saved towards paying off your mortgage instead.

# 3. Track your expenses.

Doing this helped me to find acceptable, but less expensive ways to achieve the same quality of life.

# 4. Commit to one month of decluttering your house.

Seriously, this is guaranteed to make you spend less money. You’ll be horrified at all the stuff you toss, give away or donate during a one-month declutter binge. In the future you will stop buying so much stuff.

# 5. If you have an Aldi near you, learn to embrace Aldi.

Shopping at Aldi helped us slash our food bill The trick is to stock the car with bags and quarters so you can get a shopping cart and bag your own groceries. Aldi saves us time too: it’s the quickest grocery store to get in and out of. They also now deliver with Instacart.

# 6. Learn to cut hair—don’t be afraid, you can do this!

When my husband started to read Mr. Money Mustache, he went to Walmart and bought a color-coded, foolproof hair trimmer. It came in a plastic container with instructions. I discovered that after a few tries I could cut men’s hair. I estimate this $22 investment saved us about $6,000 over the years of cutting not only his but our two boys hair. Plus it’s saved us time because I don’t have to wrestle the kids into the car.

# 7. Stop shopping.

Send your significant other into the store instead. My husband goes in with a list and only exits the store with what’s on the list. It’s like he has blinders on when it comes to impulse purchases.

# 8. Embrace the Instant Pot.

Not only will this fantastic device save you time, but oodles of money too!

# 9. Learn how to store food properly, so you waste less.

I have to admit though, I’m a visual person, so the mushrooms kept going bad when we’d put them into brown paper bags. Out of sight, out of my epicurean mind. I’ve taken to propping them on their side on the shelves at eye level, so they’re the first things I see when I open the fridge door.

# 10. Periodically examine your expenditures sheet with your significant other.

This falls under “What are your goals/priorities?” We sit down a few times a year to examine our spreadsheet and analyze where we should spend not only less but also more money.

Girlfriends, I have faith in you taking control of your finances—you got this!

Yours,

Final Thoughts on Frugal Tips for High-Income Earners

It's easy to fall into the trap of allowing a high income to dictate high spending. You certainly don't have to use all these tricks all of the time. However, by making frugality a priority in your life as B.C Krygowski does, you'll be surprised how much money you can save and invest without feeling like you're making huge sacrifices.

Join the Wealthy Mom MDs Facebook Group to continue the conversation!

Did any of these frugal tips surprise you? What do you do as a high-income earner to keep more money in your bank accounts each month?

2018 Me Has A Conversation With 1998 Me: Me on Money, Investing, Family, and Career – Part 1

This is a guest post by “Vagabond MD,” well known to those in the physician personal finance community. He is a 53 year old radiologist who recently emerged from burnout and currently works part time. He is married an attorney and has two children – one in college and one in high school.

2018: Dude, you were a total idiot for buying that fancy Euro car right out of training, on credit (of course!), before receiving your first paycheck. Bad on you!

1998: Hey, man, give me a break. I always wanted one and could finally afford one.

2018: No way, you could not afford it. You could afford the payments, not the car. Big difference.

1998: Nobody buys cars outright. Everyone makes payments, right?

2018: Well, the last six cars you (I) purchased were with a check.

1998: Really? Wow, I must have made a lot of money and saved some of it, too.

2018: About a year ago you read, “The Millionaire Next Door”, and it changed your life.

1998: True dat. I was on course to be a UAW (Under Accumulator of Wealth), and I turned that ship around.

2018: Keep turning it, bro. Here’s something else you should know. This investment and mutual fund “hobby” you are enjoying is actually making you poorer, not richer.

1998: How can that be? I am researching and discovering the stocks and funds and trading strategies that are going to make me wealthy by the time I am your age.

2018: Dude, you were a total idiot for buying that fancy Euro car right out of training, on credit (of course!), before receiving your first paycheck. Bad on you!

1998: Hey, man, give me a break. I always wanted one and could finally afford one.

2018: No way, you could not afford it. You could afford the payments, not the car. Big difference.

1998: Nobody buys cars outright. Everyone makes payments, right?

2018: Well, the last six cars you (I) purchased were with a check.

1998: Really? Wow, I must have made a lot of money and saved some of it, too.

2018: About a year ago you read, “The Millionaire Next Door”, and it changed your life.

1998: True dat. I was on course to be a UAW (Under Accumulator of Wealth), and I turned that ship around.

2018: Keep turning it, bro. Here’s something else you should know. This investment and mutual fund “hobby” you are enjoying is actually making you poorer, not richer.

1998: How can that be? I am researching and discovering the stocks and funds and trading strategies that are going to make me wealthy by the time I am your age.

2018: No, that’s what you think. But not how it works. You would be much better off learning about index funds and low cost buy-and-hold investing and shoveling as much excess income into these funds as you can. Forget about the hot manager (Van Wagoner), the value manager (Whitman), and any investment that begins with the word, “Janus”.

1998: Index funds, at Vanguard, with that weird Bogle guy, right? Nobody really believes that crap. Van Wagoner Emerging Growth was up 74% last year. I want some of that action!

2018: Van Wagoner Funds have been dead and gone for over 15 years. That kind of investing never works in the long run. Hardly anyone even remembers yesterday’s star managers. Everyone with half a brain is using index funds…and they really do work to build wealth, over time.

1998: Hard to believe, but okay, if I drop the investment hobby, what should I do with my free time?

2018: Study Italian Renaissance art, cook meatless paella, and learn to do some stuff around the house. All of them are more enjoyable and will serve you better than trying to pick future investment winners.

1998: Meatless paella? Am I still a pescatarian?

[caption id="attachment_2498" align="aligncenter" width="300"]

2018: No, that’s what you think. But not how it works. You would be much better off learning about index funds and low cost buy-and-hold investing and shoveling as much excess income into these funds as you can. Forget about the hot manager (Van Wagoner), the value manager (Whitman), and any investment that begins with the word, “Janus”.

1998: Index funds, at Vanguard, with that weird Bogle guy, right? Nobody really believes that crap. Van Wagoner Emerging Growth was up 74% last year. I want some of that action!

2018: Van Wagoner Funds have been dead and gone for over 15 years. That kind of investing never works in the long run. Hardly anyone even remembers yesterday’s star managers. Everyone with half a brain is using index funds…and they really do work to build wealth, over time.

1998: Hard to believe, but okay, if I drop the investment hobby, what should I do with my free time?

2018: Study Italian Renaissance art, cook meatless paella, and learn to do some stuff around the house. All of them are more enjoyable and will serve you better than trying to pick future investment winners.

1998: Meatless paella? Am I still a pescatarian?

[caption id="attachment_2498" align="aligncenter" width="300"] Meatless Paella[/caption]

2018: Yes, but now you are cheating because the word, “pescatarian” will not be known to you for a few more years.]]>

Meatless Paella[/caption]

2018: Yes, but now you are cheating because the word, “pescatarian” will not be known to you for a few more years.]]>

Fire Your Financial Advisor course.

Part 1 covered the license designations an FA can and should have.

Part 2 covered how FAs should get paid.

Part 3 – What's the difference between a financial advisor and planner?

Part 4 – How to find and vet a financial advisor

Part 5 – I fired my financial advisor

Johanna and I separated after about two years of working together. Before I go into why, I thought I would first discuss why a financial blogger would hire one in the first place. I mean, if I am giving information shouldn't I know what I am doing and not need one?

Why I Hired a Financial Advisor

Curiosity … and blog research!

I noticed that the other finance blogs were mainly (perhaps all?) staunch DIY and anti-FA. Curiously, many also give advice about financial advisors yet have never worked with a true financial advisor or planner. So, I became curious and thought working with one would be great research for my blog and I may learn a thing or two!

Afraid to make any more big mistakes

I finished residency at age 38 with ~$200,000 in student loans and barely $1,000 in retirement accounts. That was a huge hill to climb. I could not afford to make any more big financial mistakes if I ever wanted to “retire”.

Combining finances

Things were getting serious with M. Although I felt pretty comfortable managing my own money, managing our money made me feel a bit uneasy as making mistakes would now affect two instead one.

What I Loved About Having a Financial Advisor

During the time that I worked with a financial advisor, I actually realized there were some great benefits. Here's what I loved:

Systematically going over our financial houses

The part of reviewing finances that takes the longest (at least for us) is gathering lots of important documents, scanning them, then uploading them into a secure website for them to review. These include all of our insurance policies, retirement plans, etc.

Our planner made sure we were adequately insured. Perhaps one of the most important things we accomplished was getting our estate plan done: wills, power of attorneys, and health care proxies. Too often this becomes a non-urgent to-do item that never gets done and then it is too late.

Advice (duh)

Johanna and her team had their work cut out for them. Their brand new clients get engaged then pregnant and then decide to move cities with new jobs. All of this happened within half a year!

I was unemployed for about 16 weeks during my maternity leave. Additionally, I was freaking out about not bringing in any money while I watched my checking account only go down. Lots of impulse shopping on amazon.com didn't help either. Perhaps it was all postpartum hormones but Johanna had to talk me down a few times. Having someone you trust say “you will be ok” is and was priceless.

The big picture

We discussed our goals and dreams. After all the information gathering, we received snazzy reports and graphs comparing different scenarios (renting vs. buying, etc). I also learned that we would and could reach financial independence a lot sooner than I thought.

Why I Fired My Financial Advisor

I guess you could say I am a true DIYer. Honestly, I love creating and updating spreadsheets with our numbers. I love crunching the numbers. And I am comfortable managing our money.

Our FA custodied some of our accounts and I did not like not being able to manage them myself. I suspect most people who hire FAs want to delegate these tasks. And perhaps lastly, I drank the FIRE Kool-Aid. We are currently optimizing and minimizing our expenses to reach FIRE. All of these factors combined meant that it was time for me to fire my financial advisor.

What Should You Do?

There are two schools of thought when it comes to money. Some people prefer to DIY their own finances. Other people choose to work with financial advisors.

There are so many variables to consider when choosing which path to take. If you do decide to work with an advisor, make sure you pick an advisor that you can trust. Working with a fee-only financial advisor is one way to ensure that your planner has your best interests in mind. Also, remember that your relationship with that advisor doesn't have to last forever.

What did you think? Were you surprised that I fired my financial advisor? Have you worked with a financial advisor? What worked and didn't work?

2018 is well underway. Last year, M and I had a good amount of tax advantaged retirement “pots” available to us along with some employer match and contributions:

- My 403(b) + generous employer match + contribution

- My 457(b)

- My cash balance plan

- My backdoor Roth IRA

- My solo-401(k)

- His 403(b)

- His Roth IRA

- His solo-401(k)

- My 401(k) + employer match

- My solo-401(k)

- My backdoor Roth IRA

- My HSA

- His 401(k) + employer match

- His Roth IRA (may need to backdoor it this year)

- His family HSA

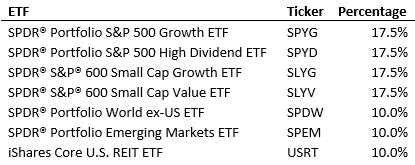

- Our taxable account

- 68% US stocks

- 17% Large cap growth, 17% Large cap value

- 17% Small cap growth, 17% Small cap value

- 24% International stocks

- 12% Large cap developed countries

- 12% Diversified emerging markets

- 8% US REITs

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

have to work for money. Traditionally, FI was equivalent to “retirement.” Retirement meaning you stopped working all together usually around the age of 65 or so. Think days at the golf course, river cruises in Europe, and a drink with a little umbrella in hand. Now, the definition of retirement is evolving and FI seems more fitting now since it includes the traditional definition and more.

You've arrived.

RE = Retire Early

RE is pretty self-explanatory. What counts as RE depends. In the non-physician world the famous RE folks are in their early 30s:

- Mr. Money Mustache retired at age 30

- Financial Samurai retired at 34

Early 30's would be exceedingly difficult for a traditional physician who begins attending life at age 30. I guess you'd have to be a Dr. Doogie Howser to do that. Physician on Fire is almost there as he recently announced that he is going part-time at the age of 41. I think a physician who can “retire” at age 45-50 is considered RE.

FIRE = Financial Independence, Retire Early

FIRE is a special club. You've officially arrived if you're a member. Not only can you not work for money if you don't want to but you've attained this at an age much earlier than anyone else. This is a popular goal to strive for.

FF = Financial Freedom

Isn't FF and FI the same thing? Maybe. If you're a splitter (vs. a lumper) then FF is one step beyond FI. It's FI + generous wiggle room. It's a bit naive to think you know and can predict your expenses 20 or even 30 years into the future. Things may go as planned, but often, they do not. Your wants will most certainly change. Health care costs are nebulous and completely unpredictable. A health crisis can easily eat up several 100s of thousands of dollars for things like home health care or a long-term care facility. A family member may need help and maybe you'd like to be in a position to help them and not derail your goals either.

Stay tuned for the second part of this post – how to determine your FI or FF number and more!

What's your FI number? Are you FI, RE, FF, or FIRE? Comment below!

View from my previous apartment in Williamsburg, Brooklyn, NY on Christmas Eve[/caption] It's definitely easier to attain financial independence (FI) faster when you live in a LCOL (low cost of living) with a high income. Is it out the window when you live in a HCOL (high cost of living) – like Brooklyn, NYC (where I live) or the San Francisco Bay Area? Of course not. But some thing(s) need to give if you want to reach it in a reasonable amount of time. So, how are we able to put away > $80,000 a year towards FI, pay down loans aggressively, be able to afford child care in this expensive city AND still be able to enjoy life? 1. We keep housing costs as low as possible This is probably the largest ticket item for those of us in a HCOL. A modern (meaning it includes a dishwasher and laundry in-unit) 2 bedroom apartment in a great part of Brooklyn will be a minimum of $4,000 for likely < 1,000 sq. ft. Manhattan? Try $5,000 and likely much more for any decent neighborhood. What about buying? Try $1 mill for a tiny 1 bedroom (again, if you're lucky) and upwards to $2 million+ for a 2+ bedroom apartment. That doesn't include the monthly maintenance fee. Want a parking spot? Extra.

“If you will live like no one else, later you can live like no one else.” – Dave Ramsey

I am not a huge fan of Dave Ramsey, but his basic mantras will serve most people very well. M and I live in a tiny apartment (730 sq ft). M owns this apartment and luckily bought in the early 2000s for a whopping down payment of < $20,000. No, there isn't a missing zero. It is a true two bedroom, one bathroom apartment. We have a dishwasher and our own laundry – which in NYC is a luxury. With the upcoming baby (and our bonus son that we have sporadically during the school year), many have told us that we have to upgrade. Nope. My brother and I attended high school living in a similar apartment (sharing a room). This won't be “forever” but we are doing our best to stay here until my student loans are paid off by end of 2020 or earlier. We will finish paying off M's car loan (I drive to work) in the next month or so leaving just the mortgage on his end. We street park (free). Our total housing costs (mortgage + taxes + condo fee) is ~5% of our 2017 annual gross income.

2. We chose a financially like-minded partner

Aka choose your spouse wisely. OK, so we didn't exactly do this on purpose, but sorta (at least on my end)? About 1-2 months into dating M, I asked him about his finances. Specifically, I asked him how much money he had in his retirement accounts and what debt(s) he had. I also knew that he wasn't a big spender. As things became more serious we discussed our shared financial goals for the present and future. We did this before we got engaged.

2. We make savings automatic

My 403(b) and 457(b), and his 403(b) contributions are automatically deducted from our paychecks. We never see the money. Since these are all pre-tax contributions, we don't really miss it vs. not doing this automatically and seeing if “we can afford to save.” We do our best to fund the Roth IRAs early in the year so we don't miss it and are not tempted to spend the money instead.

3. We (mostly) stick to a budget

I use YNAB to budget. I haven't added M's expenses yet but I am able to track our overall spending in eMoney (web based software we use with our FA). I've been using YNAB for over 2 years now. I was a spendaholic and this is my rehab.

4. We don't buy (much) stuff

We aren't minimalists, but we both agreed that stuff does not make us happy. We also don't have room for the stuff anyway (see above).

5. We have decided on the 1-2 things we really enjoy and don't hesitate to spend on it

Luckily, we both really enjoy eating out & cooking good food and traveling. Sure, we could nix all vacations and eat rice and beans until loans are paid off but it's important to enjoy life now too. We do try to meal plan for the week and we generally bring lunch to work. We budget for all of this.

[caption id="attachment_1137" align="aligncenter" width="402"] Lots of wristbands to get into Panorama 2016[/caption]

Lots of wristbands to get into Panorama 2016[/caption]

Another thing we both really enjoy is attending live concerts of our favorite bands (mainly indie pop/rock/some electronic). Luckily, NYC is almost always a stop on anyone's tour. Not to mention home of some of the big summer festivals. Confession: I have not paid for a single concert since M & I met. One of the big perks of M's job is free (and VIP) access to almost any concert we want to go to. We attended Panorama last summer. In the past several months, we have seen the Shins, the xx, Sigur Ros, Frightened Rabbit, M83, Tame Impala, Sia, the 1975s, Mumford and Sons, and Flume to name a few.

Bottom line – we live well below our means.

How are you making it in a HCOL? Comment below.

]]>

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]