Bonnie Koo

View from my previous apartment in Williamsburg, Brooklyn, NY on Christmas Eve[/caption] It's definitely easier to attain financial independence (FI) faster when you live in a LCOL (low cost of living) with a high income. Is it out the window when you live in a HCOL (high cost of living) – like Brooklyn, NYC (where I live) or the San Francisco Bay Area? Of course not. But some thing(s) need to give if you want to reach it in a reasonable amount of time. So, how are we able to put away > $80,000 a year towards FI, pay down loans aggressively, be able to afford child care in this expensive city AND still be able to enjoy life? 1. We keep housing costs as low as possible This is probably the largest ticket item for those of us in a HCOL. A modern (meaning it includes a dishwasher and laundry in-unit) 2 bedroom apartment in a great part of Brooklyn will be a minimum of $4,000 for likely < 1,000 sq. ft. Manhattan? Try $5,000 and likely much more for any decent neighborhood. What about buying? Try $1 mill for a tiny 1 bedroom (again, if you're lucky) and upwards to $2 million+ for a 2+ bedroom apartment. That doesn't include the monthly maintenance fee. Want a parking spot? Extra.

“If you will live like no one else, later you can live like no one else.” – Dave Ramsey

I am not a huge fan of Dave Ramsey, but his basic mantras will serve most people very well. M and I live in a tiny apartment (730 sq ft). M owns this apartment and luckily bought in the early 2000s for a whopping down payment of < $20,000. No, there isn't a missing zero. It is a true two bedroom, one bathroom apartment. We have a dishwasher and our own laundry – which in NYC is a luxury. With the upcoming baby (and our bonus son that we have sporadically during the school year), many have told us that we have to upgrade. Nope. My brother and I attended high school living in a similar apartment (sharing a room). This won't be “forever” but we are doing our best to stay here until my student loans are paid off by end of 2020 or earlier. We will finish paying off M's car loan (I drive to work) in the next month or so leaving just the mortgage on his end. We street park (free). Our total housing costs (mortgage + taxes + condo fee) is ~5% of our 2017 annual gross income.

2. We chose a financially like-minded partner

Aka choose your spouse wisely. OK, so we didn't exactly do this on purpose, but sorta (at least on my end)? About 1-2 months into dating M, I asked him about his finances. Specifically, I asked him how much money he had in his retirement accounts and what debt(s) he had. I also knew that he wasn't a big spender. As things became more serious we discussed our shared financial goals for the present and future. We did this before we got engaged.

2. We make savings automatic

My 403(b) and 457(b), and his 403(b) contributions are automatically deducted from our paychecks. We never see the money. Since these are all pre-tax contributions, we don't really miss it vs. not doing this automatically and seeing if “we can afford to save.” We do our best to fund the Roth IRAs early in the year so we don't miss it and are not tempted to spend the money instead.

3. We (mostly) stick to a budget

I use YNAB to budget. I haven't added M's expenses yet but I am able to track our overall spending in eMoney (web based software we use with our FA). I've been using YNAB for over 2 years now. I was a spendaholic and this is my rehab.

4. We don't buy (much) stuff

We aren't minimalists, but we both agreed that stuff does not make us happy. We also don't have room for the stuff anyway (see above).

5. We have decided on the 1-2 things we really enjoy and don't hesitate to spend on it

Luckily, we both really enjoy eating out & cooking good food and traveling. Sure, we could nix all vacations and eat rice and beans until loans are paid off but it's important to enjoy life now too. We do try to meal plan for the week and we generally bring lunch to work. We budget for all of this.

[caption id="attachment_1137" align="aligncenter" width="402"] Lots of wristbands to get into Panorama 2016[/caption]

Lots of wristbands to get into Panorama 2016[/caption]

Another thing we both really enjoy is attending live concerts of our favorite bands (mainly indie pop/rock/some electronic). Luckily, NYC is almost always a stop on anyone's tour. Not to mention home of some of the big summer festivals. Confession: I have not paid for a single concert since M & I met. One of the big perks of M's job is free (and VIP) access to almost any concert we want to go to. We attended Panorama last summer. In the past several months, we have seen the Shins, the xx, Sigur Ros, Frightened Rabbit, M83, Tame Impala, Sia, the 1975s, Mumford and Sons, and Flume to name a few.

Bottom line – we live well below our means.

How are you making it in a HCOL? Comment below.

]]>

Last month I spelled out how we are investing our money in 2017. I mentioned there were some moving parts – namely, M was unemployed and we knew, at the time, that I was (newly) pregnant. Now, M has a job (yay!) and looks like this pregnancy will stick, so now we can do some real projections for 2017. Our asset allocation will remain the same.

This year our total “retirement” contributions will consist of:

This year our total “retirement” contributions will consist of:

- $18,000 my 403(b)

- $20,800 employer match + contribution into my 403(b). Currently 20% vested. 40% vested as of August 1, 2017 so actually $8,320

- $18,000 my 457(b)

- $5,500 my Roth IRA

- $18,000 his 403(b). No matching at this time

- $11,000 his Roth IRA (his first! For 2016 and 2017)

- Other sources:

- A very modest amount ~$1,000 into my solo-401(k). Yes this blog likely won't lose money this year 🙂

- ~$5,000 his solo-401(k) – he has some 1099 income this year

M and I are pleased to announce that we are expecting a baby boy this fall. We have nicknamed him “Eggy” – it means baby in Korean. As you know, you cannot exactly plan when you become pregnant. Honestly, we were not sure if things would happen au naturel due to my age so IVF was a possibility. Luckily my current job includes 3 cycles of IVF as a benefit but it is still not 100% covered. I know many ladies who have spent a small fortune on getting pregnant. So here are a few things I have learned, financially, about trying to get pregnant and trying to plan for leave and childcare:

- Insurance coverage: Make sure you know what your insurance plan will cover and not cover and what deductible you'll need to meet, if any. Even if your insurance says “maternity is covered,” it may not cover all the tests. My costs: $40 (co-pay for the first visit only) is what my total out of pocket costs will be, including the delivery. This assumes I use an ob-gyn within my health system (I am) and that I deliver at one of their hospitals (I plan to).

- Maternity Leave: Think about how long you'll want to take for leave and what leave, if any, will be paid. This is a highly personal decision, but I have yet to meet someone who said they took too much time off. Unfortunately, paid maternity leave is not the norm in the U.S. If you have unpaid leave at least you'll have approximately 9 months to save up for this. My leave: I get 6 weeks paid leave (at my base salary) or 8 weeks (c-section). I can also use unused vacation. I will have at least 2-3 weeks of unused vacation to get to at least 8 weeks paid. I am taking at least 3 months off. So that means at least 1 month unpaid, possibly more. Since I only really need ~60% of my take home base salary, this won't be a huge burden on us and we will have more than enough saved to cover this unpaid time.

- Maternity clothes: Unless you only wear stretchy pants and dresses, you'll need at least a few staples. I do wear scrubs a few times a week to work so I did not have to buy a whole new work wardrobe. Gap Maternity is pretty inexpensive and I was able to use a 20-40% off coupon when ordering online. It also helps that it'll be mostly warm weather during my pregnancy so I can keep wearing dresses.

- Baby stuff: I am totally cool with second-hand everything. And due to space limitations of an NYC apartment, we definitely do not want too much “stuff.” Between a baby shower, a very excited grandmother-to-be, M's sister's hand me downs – we should have most of the basics for almost free. I have even scored a free Mamaroo and Ergo carrier already. I won't be shopping at baby boutiques for clothes.

- Post-partum help: If you don't have family around you may want to look into outsourcing certain things (clean and cook, etc) so you can focus on mothering. Baby nurses and night nannies are common in NYC – definitely a luxury – but a savior when you're sleep-deprived. Post-partum doulas are also a great idea, especially for first time moms, to show you the ropes, help you ease into breastfeeding (most are breastfeeding certified counselors), and help you take care of you while you recover from delivery. The U.S. is a bit strange in that moms are expected to recover and go back to work ASAP. Too bad there aren't any post-partum spas here like Korea. My plans: M will take 2 weeks off to help. I'm planning on hiring a post-partum doula for a few sessions for the above reasons. After 2 weeks, I'll be with my mom for a few weeks – letting her carry out a Korean tradition of taking care of a new mom. Slightly modified as I'll be able to shower :).

- Childcare: This blog is geared towards female professionals, so most of us probably won't be stay at home moms. I'd be lying if I said I wasn't worried about the cost of childcare! The going rate in my neighborhood is ~ $17/hr for a nanny. At this time, I prefer having a nanny for the first 6-12 months after I return to work. The convenience of someone coming to us vs. one of us packing up the baby and walking to a daycare (at least a 10-15 min walk – won't be fun during winter). Also, babies and kids often get sick in daycare and although M's work is more flexible, we don't want to deal with that. Right now, we are planning to have a nanny for 40 hours a week over 4 days and my mom for 1 day a week and for backup. We are *gulp* preparing to spend at least $3,000 a month in childcare. Unfortunately, daycare isn't much cheaper and with the convenience and flexibility of a nanny, this was a no brainer for us. After 6 months or so, we will reassess.

- Saving for college: It's never too early to start saving for a little one's college. You may recall that I started a 529 last year in anticipation of starting a family. I get a small state tax break for funding one so it was a no brainer to get started.

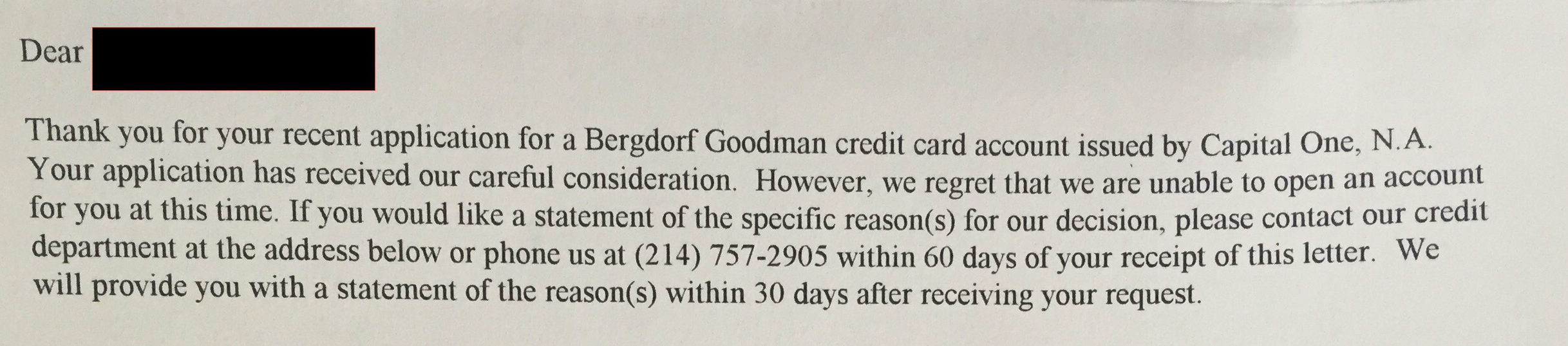

I was almost a victim of identity theft.

I did not apply for this card:

For those of you not familiar with Bergdorf Goodman – it is a high-end luxury department store in NYC – think Gucci, Prada, Chanel. Unfortunately, not a place I will be shopping at anytime soon.

I checked on Credit Karma and there it was – a hard inquiry on Equifax dated around the same time of the above letter from this department store. I also found another hard inquiry that I did not initiate. I took this opportunity to thoroughly review what accounts are open and make sure they were actually mine. Phew – all good. But I did find 3 old store cards that I haven't used in years. I went ahead and closed them.

I then froze my credit at all 3 agencies – Equifax, Transunion, and Experian.

What does freezing credit do? It prevents unauthorized use of your credit to open credit cards, mortgages, etc. unless you/they have your pin. This pin is issued when you freeze your credit. When you need to open a new card or mortgage you simply unfreeze or thaw your credit. Best if you call the bank or institution and find out which agency they will use first so you only need to thaw one agency. There may be a fee to thaw – but negligible compared to the headache and time needed to undo fraudulent activity.

So, even if someone does get your information they will not be able to open any lines of credit without this pin. Guard this pin! You will not be able to do anything without it. Make copies, upload to a secure cloud etc.

Freezing your credit has no impact on your credit score. Freezing and thawing credit is also state specific in terms of how long it will stay frozen and fees to freeze or thaw.

Check out this excellent freeze/thaw guide for links and info on how to easily freeze your credit. Please note that freezing credit does not affect a theft's ability to steal and use your actual credit card. Thankfully, this is much easier to deal with.

And, don't forget to freeze your children's credit! Yes the thieves are even going after them.

If you're eligible, you can take things further and obtain a pin from the IRS so that no one else can file in your name. Yes it happens, and I can assure you this is a much bigger PITA to deal with. Unfortunately, at this time, you need to be eligible to obtain one:

- You receive CP01A Notice containing your IP PIN, or

- You filed your federal tax return last year as a resident of Florida, Georgia or the District of Columbia, or

- You received an IRS letter inviting you to ‘opt-in' to get an IP PIN.

I am not eligible at this time. Hopefully the IRS will soon let anyone obtain a pin to protect themselves.

- Part 1 covered the license designations an FA can and should have.

- Next, Part 2 covered how FAs should get paid.

- Then, Part 3 explored what real financial planning is.

- In Part 5, I discuss why I fired mine.

Today is Part 4 – How to find and vet a financial planner. I will also share how I found and vetted mine.

How to Find a Financial Advisor

You want to find a financial advisor, but you've got a question. Where do I start?

A personal recommendation is always helpful, but you'll still need to do your own vetting.

Step 1 – Do Your Initial Vetting

If you're convinced that a fee-only FA is the only way to go, a good place to start is NAPFA – the National Association of Personal Financial Advisors. They are a leading organization of fee-only advisors. Now, just because someone isn't listed here does not mean they are not good. To make the list, members must:

- Be CFP’s

- Sign a pledge to serve as their clients’ fiduciary

- Submit a financial plan for review and approval (they are not rubber stamped)

- Complete 30 hours of approved CE annually

Now, what if there isn't anyone in your location?

In my opinion, your FA does not need to be local. You can conduct meetings in the comfort of your own home via video conference. Personally this seems much more convenient than scheduling in person meetings, but I do understand that some folks prefer the one-on-one meetings.

Many FAs also have a blog or a podcast. This is a great way to peruse their content and to see if their philosophy and personality meshes with you.

Step 2 – Review Form ADV

Let's say you have a few names of FAs. After browsing their website and reviewing their fee structure and what is included, you're now ready to for the next step. Review their Form ADV. Form ADV is the informational document that the SEC (Securities and Exchange Commission) requires all investment advisors to file and update annually. It contains a lot of information and you'll need to know what to look for.

My former FA wrote an excellent post on how to decipher a Form ADV. Go ahead, take your time to read it. Did your potential FA pass?

Step 3 – Set Up a Consultation

Now you're ready to set up a consultation. Almost all FAs will conduct a consultation for free. This is your chance to “meet” (virtually, phone call, or in person) and get your other questions answered.

Step 4 – Take Your Time

After this meeting you should have enough information to make a decision. Take your time – this decision will affect you – your net worth, positively or negatively.

What I Did to Find a Financial Advisor

Now that you know the basic steps, you're probably wondering how I found my financial advisor. I first heard of Johanna through the White Coat Investor Forums. I was a semi-active member and found her posts not only helpful but she clearly knew what she was talking about. When I found out she was going to be in NYC for a conference, I private messaged her if we could meet.

At that time, I was not really thinking of hiring her let alone any FA. But I wanted to take the opportunity since she was in town. So M and I got to meet her in person at one of my favorite bars in Brooklyn, Hotel Del Mano.

Afterwards, she sent us a copy of Nick Murray's Simple Wealth, Inevitable Wealth. I skimmed it. Then I had questions.

At this time, I did not know what a Form ADV was (nor did I know such a thing existed), but I knew that fee-only was the way to go.

I emailed her these questions:

Are you a fiduciary?

Yes and we sign a statement to that effect for every client.

Is the portfolio you recommend to your clients (I know you rec 1/6 each to 6 categories) also YOUR personal allocation?

We use this portfolio for myself, Michelle, my mom and my sons, along with the rest of our clients. I would not recommend something that I wouldn’t do for my own family.

How long have you been recommending this?

For the last 7 years, at least.

How long have you been doing this allocation for yourself?

Almost that long. Like some, I had trouble giving up on funds that I was in love with (YACKX, in particular). I finally got rid of the others except for YACKX and just worked it into the portfolio as part of my LC Value funds. As I tell Michelle, we eat our own cooking here and practice everything we tell our clients. (Well, I’m better at planning for my clients than I am for myself, but that’s a different story, kind of like the doctor who can’t quit smoking).

And what is the past performance of this?

I looked up the client who has been with us the longest and her average annual return is 10.31%. Of course, this has been during a bull market, with only 1 down year (2015 although 2016 hasn’t been exactly fabulous so far) so I can’t take a lot of credit. We don’t benchmark and we tell our clients to expect about 8% during the long term and to have no expectations during the short term (next 5 years).

How did you handle 2008?

I began my business in 2008/2009 (had only the CPA firm before that) and so I had only my own and kids’ funds in the bear. I did nothing different. However, I didn’t hear Nick Murray speak for the 1st time until (I think) 2009, and my world changed at that point.

Personally and for your clients, how did you handle clients who panicked and sold?

N/A.

Did you lose a lot of clients during this time?

N/A. Btw, I was investing for myself in the dot.com crash in 2000. I made all of the mistakes that could be made on my own account during that crash. Truthfully, I am so thankful that I have not done anything like that for our clients and never will. Unlike many investment advisors, we don’t experiment with our clients’ accounts.

Can you talk about the last 2 clients that left and why?

The only large client we have lost (about $400k) was 1.5 years ago. She decided to use the trust department of a bank because her family’s trust was there and she wanted to consolidate. A couple of years ago, a client (<$100k) moved to Edward Jones because her cousin owns the office. Because we handle SIMPLE plans for a few CPA clients, employees periodically leave and cash out, but it is a relief to lose a small account. We only handle these plans because the business owners have large accounts and as a convenience for them.

Tell me about a client that you let go and why?

I don’t know of any we’ve let go. We are extremely careful about who we work with and try to ensure that they deselect themselves by educating them on what we do at the beginning of a relationship.

Who is your ideal client?

Flat-fee doctor planning clients. We just started this model about 6 months ago and it is proving pretty popular. I like this (rather than our AUM model that the clients who started with us before this year are under) because it focuses on the plan and it doesn’t focus on performance, which is aligned with our values. Since we model the stock market, returns are going to be similar to long-term market returns.

How many do you take on a year?

Can’t say at this point. I’ve been bad about enforcing minimums in the past and we are going to have to let some clients go in the next year to focus on doctors. We are planning ahead to add another team member next year.

What will happen if something happens to you?

(Michelle is 16 years younger and the main reason I asked her to work with me and eventually become partner was for succession planning.

How long have you been doing this?

See above. I had been making recommendations to clients as a CPA for many years, but sending them to brokers. The reason I decided to become a CFP was because I did not like the way our CPA clients were treated and the results. I thought I could be a better advisor than what they were getting. When I first began, I did not know what fee-only was or how important it was to be a fiduciary. I found out soon after starting and knew I’d found my home (same as with Nick Murray).

Have you been sued by a client or have had any legal action against you from a client?

Never.

What is the average size portfolio you manage?

Around $75k because of all the SIMPLE accounts. Our sweet spot is $400k – $750k.

Smallest?

Because of the SIMPLEs, a few hundred dollars.

Largest?

Around $3M. Please note that the size of the portfolio is really not an issue except for AUM clients. With flat-fee planning, we concentrate on your plan and build a portfolio that will sustain the plan rather than the other way around. A portfolio is not a plan – big difference. Think about it – some people prefer to invest in their businesses or real estate as part of their retirement. Their stock market portfolios will be smaller, but they will not be “smaller” clients (actually more complicated).

What is the average length of a time a client stays with you?

I don’t have those figures. If we took out the SIMPLE accounts (which I have nothing to do with), it is pretty much since they have begun with us.

Are you able to provide any references that would be willing to talk to me?

Maybe. I guard my clients’ privacy and have only asked once for someone to give a referral. The prospect decided to keep managing his own money at the time (although he took a recommendation I made that kept him from making a huge mistake) so I bothered a busy client business owner needlessly.

I know you are not the biggest fan of Vanguard, so which funds do you prefer and why?

The funds we prefer are those that stick to the terms of their prospectuses and have really good managers. The prospectus is the rule book for how a fund manager or committee is to allocate the dollars that flow into and out of the fund and run the fund. Because we have such definite terms on our client portfolio allocation, it is important that we can trust the manager to play by the rules he was hired to follow. Not all do.

Have they outperformed similar funds in Vanguard?

I have no idea and I don’t care. We are not in a performance game. If we can mirror long-term market performance, using behavior management (which is most important – proper investing is really quite simple), then our clients will be quite successful. I hate to keep saying this, but low-cost funds do not guarantee you a successful portfolio.

The cost is but one aspect of investing. Yes, if everything else is equal, we will choose the lower cost fund. But a fund can’t simply hire a manager and tell him/her to keep the costs down and expect the fund to perform up to its peers. I think that is overemphasized on WCI and is actually a detriment to the investing results of many doc’s. It sets up a false premise – that cost is 90% of results. The examples that are given of the long-term extra costs of a fund that has a quarter of a point more cost over 20 years assume everything else is equal. It never is.

My job is not to outperform. Instead, my job is to ensure that our clients build optimal wealth over the long term given their resources, goals, and life events. It is a bit more complicated than “Let’s go to Vanguard and choose low-cost funds.” We use a few Vanguard funds, but I am not of the opinion that Vanguard is the absolute best fund family to the mutual exclusion of all others. That’s just not rational.

Does working with you/firm also include discrete events like death of a spouse? buying a home? etc? Or is that extra?

Clients never pay extra unless there is a reason to change the engagement and prices don’t go up without notice. Being someone’s financial planner means that I am integrated into his/her life. Everybody has a different path.

I mentor several people and was telling a young man yesterday that it is important to have processes that make planning consistent, keeps us accountable, and surpasses our clients’ expectations while maintaining the individual experience for each client. So, yes, specific life events are what I am here for. Everyone is unique – we don’t do cookie cutter planning here. Not every doctor is paying down student loans.

And finally, is there anything else you think I should know about you?

Like I yelled at my dog this morning? Seriously, there probably is. I’m not hiding anything, but I don’t know what else to tell you right now – may think of something later.

I will tell you that I’ve seen a lot of the crap that passes for financial planning out there and you could do a lot worse than to hire someone who has 35 years of experience as a CPA combined with 9 as a CFP who is also fee-only and works with doctors. I’m not even sure if I’ve run across myself before.

Actually, here’s something: you won’t work exclusively with me. You would work mostly with me, but you would also meet sometimes with Michelle. She trains clients how to use our software, eMoney, and handles all investing functions. And that’s a good thing because we back each other up. You should also know that we custody with TD Ameritrade (which is not the same as TD Bank).

Here is Our Process page. I’ve also attached a draft copy of our Expanded Agenda page. It’s not ready to go online yet but I thought you might find it useful to read. That’s it for now. Thanks for asking some good questions. I haven’t proofed for errors, so please be lenient lol. Let me know if you have any other questions.

This is a guest post by Liz Stapleton. She is a recovering attorney and freelance writer focusing on personal finance, entrepreneurship, and issues facing lawyers. Since starting her personal finance blog, Less Debt More Wine in 2014, Liz has paid off all of her credit card debt (over $10k), raised her credit score from 640 to 800+, and paid off one of her many student loans.

I had written a post already on my own save vs. pay off loan debacle. Liz does a nice job guiding you on how to make your decision.

What to do when you want to save for your future, but you are still paying for your past?

After spending so many years in school to get a professional degree, chances are you are already behind on saving for retirement. At the same time, along with a big shiny degree, you have a ton of student loan debt that will hamper your ability to save.

The problem is time. As you know from your student loans, interest can make a big difference in what you owe, or in the case of saving what you earn. The longer your money is in a retirement account, the more time it will have to grow.

Unfortunately, the same goes for your debt, the longer you have it, the more you pay. So which should you focus on first?

Why You Should Prioritize Debt Repayment

I recommend prioritizing debt repayment for two reasons but also with some exceptions. First, the interest rate on your debt is likely higher than the amount of interest you would earn on any investments. Second, if you are on an income-driven repayment plan and are planning on loan forgiveness, you may be in for a big tax bill.

Debt Usually Costs You More

Interest rates for debt can vary widely. Student loans for professional degrees usually range from 6% – 8%. The return on retirement investments usually ranges from 5% – 8%. However, that is over the long term, and you never know what is going to happen with the market.

For example, if you have a student loan (one of many I’m sure) with a current balance of $50,000 and an interest rate of 8%, you are paying $4,000 in interest in a year. If you were to max out a 401(k) retirement account, meaning you contributed $18,000 and earned interest at 6%, you would earn $900 from interest.

While $900 is nothing to sneeze at, to prioritize saving at a lower or even equal interest rate would require you to pay to save.

Loan Forgiveness through Income-Driven Repayment Plans isn’t Forgiveness

As the current law stands, any forgiven amount after the repayment terms ends for income-driven repayment plans such as Income-Based Repayment, Income-Contingent Repayment, PAYE, and REPAYE is considered taxable income.

This means that if worst case scenario, your monthly payment does not even cover the amount of interest that accumulates each month, then your loans could be growing. If your loans grow for 20-25 years, you are going to be taxed as if you made potentially hundreds of thousands more.

There is one exception to the loan forgiveness tax bill, and that is Public Service Loan Forgiveness (PSLF). Under PSLF after 120 qualifying payments, your loans are forgiven and not considered taxable income.

Why You Shouldn’t Forgo Saving for Retirement Entirely During Debt Repayment

While it’s likely a good idea to prioritize debt repayment now, it doesn’t mean you shouldn’t set aside some money for retirement. There are three reasons you should save for retirement while paying off debt.

First, time is money, the longer your money sits in your retirement account, the more compound interest you will earn. Second, you could potentially save free money; many employer-sponsored retirement accounts offer matching contributions. Third, saving for retirement could lower your tax liability.

When it comes to compound interest, every little bit counts

Let’s say you put $100 per month towards retirement savings. If your investment of $1200 earns a conservative 5% then at the end of the year it will become $1,260. If you stopped contributing that $1,260 would turn into $1,531 after five years. In 15 years it would become $2,494, doubling your money. If you had kept contributing just $100 a month, you would have saved $28,389 after 15 years.

Even if you aren’t maxing out your retirement contribution during debt repayment, just a small monthly contribution done consistently can go a long way.

You Never Want to Lose Out On Free Money

If you have an employer-sponsored retirement account such as a 401(k), you should educate yourself on any matching contributions they are willing to make. For example, my old company used to match a 5% contribution 100%. If I put in $5, my company would put in $5. I essentially doubled my money just be contributing to my retirement account.

You Could Pay Less in Taxes

While it is true that you can deduct up to $2,500 of the interest you pay on your student loans from your taxes [Editor's note: Almost all doctors are over the income limit for this deduction]. You can lower your taxable income even more by saving for retirement. While there are lots of different retirement accounts (401k, 403b, TSP, IRA, Roth IRA, etc.), some of them are pre-tax contributions.

Pre-tax contributions allow you to put money that has not been taxed aside for your future in a retirement account. The government will tax those funds when you withdraw the funds from the account. If you make $75,000 per year and you put a total of $5,000 of pre-tax dollars into your 401(k) you will be taxed as if you earned $70,000.

The Exceptions to Prioritizing Debt Repayment

There are some circumstances where you might want to prioritize saving for retirement over paying off debt. For example, if your debt interest rates are in the 2%- 3% range your money might be better-used saving. Alternatively, if you can afford the loan’s standard repayment plan then paying that standard monthly payment and saving more for retirement will likely put you ahead on savings, without losing too much money to interest on your debt.

What do you think? Comment below.

]]>

I had written a post already on my own save vs. pay off loan debacle. Liz does a nice job guiding you on how to make your decision.

What to do when you want to save for your future, but you are still paying for your past?

After spending so many years in school to get a professional degree, chances are you are already behind on saving for retirement. At the same time, along with a big shiny degree, you have a ton of student loan debt that will hamper your ability to save.

The problem is time. As you know from your student loans, interest can make a big difference in what you owe, or in the case of saving what you earn. The longer your money is in a retirement account, the more time it will have to grow.

Unfortunately, the same goes for your debt, the longer you have it, the more you pay. So which should you focus on first?

Why You Should Prioritize Debt Repayment

I recommend prioritizing debt repayment for two reasons but also with some exceptions. First, the interest rate on your debt is likely higher than the amount of interest you would earn on any investments. Second, if you are on an income-driven repayment plan and are planning on loan forgiveness, you may be in for a big tax bill.

Debt Usually Costs You More

Interest rates for debt can vary widely. Student loans for professional degrees usually range from 6% – 8%. The return on retirement investments usually ranges from 5% – 8%. However, that is over the long term, and you never know what is going to happen with the market.

For example, if you have a student loan (one of many I’m sure) with a current balance of $50,000 and an interest rate of 8%, you are paying $4,000 in interest in a year. If you were to max out a 401(k) retirement account, meaning you contributed $18,000 and earned interest at 6%, you would earn $900 from interest.

While $900 is nothing to sneeze at, to prioritize saving at a lower or even equal interest rate would require you to pay to save.

Loan Forgiveness through Income-Driven Repayment Plans isn’t Forgiveness

As the current law stands, any forgiven amount after the repayment terms ends for income-driven repayment plans such as Income-Based Repayment, Income-Contingent Repayment, PAYE, and REPAYE is considered taxable income.

This means that if worst case scenario, your monthly payment does not even cover the amount of interest that accumulates each month, then your loans could be growing. If your loans grow for 20-25 years, you are going to be taxed as if you made potentially hundreds of thousands more.

There is one exception to the loan forgiveness tax bill, and that is Public Service Loan Forgiveness (PSLF). Under PSLF after 120 qualifying payments, your loans are forgiven and not considered taxable income.

Why You Shouldn’t Forgo Saving for Retirement Entirely During Debt Repayment

While it’s likely a good idea to prioritize debt repayment now, it doesn’t mean you shouldn’t set aside some money for retirement. There are three reasons you should save for retirement while paying off debt.

First, time is money, the longer your money sits in your retirement account, the more compound interest you will earn. Second, you could potentially save free money; many employer-sponsored retirement accounts offer matching contributions. Third, saving for retirement could lower your tax liability.

When it comes to compound interest, every little bit counts

Let’s say you put $100 per month towards retirement savings. If your investment of $1200 earns a conservative 5% then at the end of the year it will become $1,260. If you stopped contributing that $1,260 would turn into $1,531 after five years. In 15 years it would become $2,494, doubling your money. If you had kept contributing just $100 a month, you would have saved $28,389 after 15 years.

Even if you aren’t maxing out your retirement contribution during debt repayment, just a small monthly contribution done consistently can go a long way.

You Never Want to Lose Out On Free Money

If you have an employer-sponsored retirement account such as a 401(k), you should educate yourself on any matching contributions they are willing to make. For example, my old company used to match a 5% contribution 100%. If I put in $5, my company would put in $5. I essentially doubled my money just be contributing to my retirement account.

You Could Pay Less in Taxes

While it is true that you can deduct up to $2,500 of the interest you pay on your student loans from your taxes [Editor's note: Almost all doctors are over the income limit for this deduction]. You can lower your taxable income even more by saving for retirement. While there are lots of different retirement accounts (401k, 403b, TSP, IRA, Roth IRA, etc.), some of them are pre-tax contributions.

Pre-tax contributions allow you to put money that has not been taxed aside for your future in a retirement account. The government will tax those funds when you withdraw the funds from the account. If you make $75,000 per year and you put a total of $5,000 of pre-tax dollars into your 401(k) you will be taxed as if you earned $70,000.

The Exceptions to Prioritizing Debt Repayment

There are some circumstances where you might want to prioritize saving for retirement over paying off debt. For example, if your debt interest rates are in the 2%- 3% range your money might be better-used saving. Alternatively, if you can afford the loan’s standard repayment plan then paying that standard monthly payment and saving more for retirement will likely put you ahead on savings, without losing too much money to interest on your debt.

What do you think? Comment below.

]]>

Simple and absolutely delicious – rigatoni with fresh tomato sauce and eggplant – @ Planeta Winery, Sicily.[/caption]

Do you like to travel? We love to travel. Our “splurge” is travel and food – best if we combine the too. We budget for two big trips a year. We consider it pivotal to our happiness. We are not into budget travel anymore – too old for penny pinching like staying in hostels and such.

Last year we went to Sicily and Los Angeles + OC + Santa Maria wine country. I went to Toronto and Paris + Reims with girlfriends. I traveled to Washington, DC twice for CME conferences.

You may have heard about the Chase Sapphire Reserve Card. It came out last fall and instantly became the hot new travel card. I already had the Chase Sapphire Preferred and had racked up over 50,000 points. The Sapphire Reserve offered 100,000 bonus points so I opened one last September. Now, they offer 50,000 points, which is still a great deal. I'm not a credit card churner, but for folks who travel, a travel credit card is definitely worth having. This is assuming you won't go into credit debt. I pay the cards in full every month and leverage the credit to accumulate points. I rarely use cash.

You may balk at the $450 annual fee. The fee is really $150. You get $300 in travel credit (taxis, flights, hotels). You also get a credit for global entry. So the first year, the fee is essentially $0. I already have global entry which includes TSA Pre-Check. Dining and travel spending accumulate triple points. You also get Priority Pass Select membership. This is not that useful but better than no lounge access. Centurion lounge access with the Amex Platinum (M's travel card) rounds things out nicely.

[caption id="attachment_1009" align="aligncenter" width="268"] On the never ending journey for the perfect croissant – @ Du Pain et Des Idées, Paris, France[/caption]

One of the ways we are able to budget two big trips a year is by using one trip combined with CME. Many doctors have a CME fund with their job. It isn't quite enough to fully fund a pricey CME trip since the funds are also for my licensing and society fees.

Back in January, we went to Hawaii (Big Island and Kauai). I attended a conference on the Big Island. I used points for my round trip flight. M used his Amex Platinum points for his flight. The CME fund paid for hotel, rental car and most of our meals during the conference. We paid for the Kauai part on our own.

I have since accumulated > 150,000 points on the Sapphire Reserve card. We prefer to visit Europe during shoulder season if possible (less crowded). Last year, we went to Sicily in April. Weather was great and we barely ran into any tourists, let alone any Americans. Lodging was definitely cheaper since it was off-season and thankfully, food is quite reasonable (and delicious!) there. I managed to have a cannoli every day. Flights and hotels are often cheaper too during shoulder season. Not quite shoulder season but we just booked a trip to Paris in May. I booked 2 round-trip direct flights and 4 nights hotel for $94. The rest were paid with points. Our only expense will be food and local transportation. We won't be as frugal food-wise as Physician on Fire was on his recent trip there.

How do you make travel more affordable? Comment below.]]>

On the never ending journey for the perfect croissant – @ Du Pain et Des Idées, Paris, France[/caption]

One of the ways we are able to budget two big trips a year is by using one trip combined with CME. Many doctors have a CME fund with their job. It isn't quite enough to fully fund a pricey CME trip since the funds are also for my licensing and society fees.

Back in January, we went to Hawaii (Big Island and Kauai). I attended a conference on the Big Island. I used points for my round trip flight. M used his Amex Platinum points for his flight. The CME fund paid for hotel, rental car and most of our meals during the conference. We paid for the Kauai part on our own.

I have since accumulated > 150,000 points on the Sapphire Reserve card. We prefer to visit Europe during shoulder season if possible (less crowded). Last year, we went to Sicily in April. Weather was great and we barely ran into any tourists, let alone any Americans. Lodging was definitely cheaper since it was off-season and thankfully, food is quite reasonable (and delicious!) there. I managed to have a cannoli every day. Flights and hotels are often cheaper too during shoulder season. Not quite shoulder season but we just booked a trip to Paris in May. I booked 2 round-trip direct flights and 4 nights hotel for $94. The rest were paid with points. Our only expense will be food and local transportation. We won't be as frugal food-wise as Physician on Fire was on his recent trip there.

How do you make travel more affordable? Comment below.]]>

Do you give to charity? I'm embarrassed to say that I only very recently started giving. And it's not that much. But I am happy, maybe a tiny bit proud, that I finally started.

When I was a resident, I said “I'll give when I'm an attending.” That seemed logical – I wasn't making a lot and had student loans accumulating interest every day. Then I became an attending. Then I said “I'll give once I don't have so many loans” or “I'll give once I get some financial footing.”

Somewhere along the way I discovered Farnoosh Torabi's So Money podcast. I started with her inaugural podcast with guest Tony Robbins. One part really got to me:

People say, “When I'm rich, I'll give, they're lying. If you won't give a dime out of a dollar, there's no way you're gonna give a 100 million out of a billion, you're lying to yourself. But if you can do it today, the biggest thing that giving does, is it teaches your brain there's more than enough.

Right after I listened to that podcast, I made my first donation – I pledged to give a small amount quarterly to my alma mater Barnard College and specifically earmarked the funds for financial aid. I received generous financial aid in the form of grants and work-study and hope that my small contribution (which I will definitely increase soon) will help someone else attend.

For 2017 I made a modest goal to start with 1% of my base salary towards charity. Yes, this isn't a lot, but I am starting somewhere and hope to slowly increase as a % of my base salary. I made a separate category in YNAB as well.

I have also given small amounts to:

- Camp Discovery – a summer camp for kids with severe skin diseases

- KACFNY aka Korean American Community Foundation of NY

You'll notice my medical school is missing from the list. That will have to wait until the loans are paid off. I think that just only makes sense :).

Do you give? Why or why not? Who/what do you give to?

Dealing with student loans is difficult. Being a doctor with student loan debt can be particularly challenging. 76% of doctors graduate with debt, and the median is $192,000. This is a guest post by Travis Hornsby, creator of Student Loan Planner, where he offers one-on-one student loan advice. As female physicians with student loans, if you need help navigating them, contact him.

I got into helping people understand their student loans thanks to my beautiful and brilliant fiancée Christine. She’s a urogynecologist, and like most physicians, she was more focused on learning and caring for her patients than understanding arcane federal student loan rules. Unfortunately, female physicians earn less than their male counterparts. To help tip the scales back in favor of people like Christine, here’s how to maximize student loan strategy as a female physician.

I got into helping people understand their student loans thanks to my beautiful and brilliant fiancée Christine. She’s a urogynecologist, and like most physicians, she was more focused on learning and caring for her patients than understanding arcane federal student loan rules. Unfortunately, female physicians earn less than their male counterparts. To help tip the scales back in favor of people like Christine, here’s how to maximize student loan strategy as a female physician.

Tips for Female Physicians with Student Loans

First things first. Women doctors are more likely to be employees. That's a big advantage when it comes to student loans. About three-quarters of all women in medicine work as employees instead of in private practices. That means women are more likely working at not for profit hospitals than men. That’s why female physicians need to know about Public Service Loan Forgiveness (PSLF) like the back of their hand. Under PSLF, A doctor must work for 10 years in a not for profit setting. Most hospitals qualify. You must receive your actual paycheck from a not for profit entity too. Occasionally I’ve seen some hospitals that pay their physicians out of a private sector entity. That would cause you to lose your PSLF eligibility. Make sure that doesn’t happen to you when you become an attending. Your residency counts towards this 10-year period until PSLF forgiveness. If you play your cards right, you could pay $300-$500 a month on your loans during this period, which all counts towards the 10 years required under PSLF. Virtually all physicians who manage their loans the optimal way will graduate residency with 3-7 years of credit towards the 10 years they need. What happens when you become an attending?Keep Your Payments Low to Maximize Forgiveness

Under current rules, you can use either PAYE or IBR to cap what you must pay on your student debt. That means if you owe $150,000 in med school loans but start out at $200,000 as an attending, you can keep your payments at no higher than the standard 10-year monthly amount you had to pay when you left med school. Using this cap to your advantage, you could conceivably train for several years to become a surgeon, then cap your payments on 10-year standard repayment plan. That would allow you to pay a fraction of what you originally borrowed for medical school. A lot of my clients make payments based on the Income Based Repayment plan (IBR). If that describes you, you’re probably paying too much on your student debt. You should look into switching to Pay As You Earn (PAYE) or Revised Pay As You Earn (REPAYE). The reason? You get to pay 10% of your income instead of 15% as with IBR.Make Sure Your Loans Qualify

Only Direct Federal student loans qualify for this forgiveness benefit. That covers most loans issued after 2010. If you happen to have loans from before this that are on the older FFEL loan program, you can consolidate them into a Direct loan. That consolidation makes them eligible for PSLF, but it also resets the repayment clock to zero. Make sure your loans don’t qualify for PSLF before submitting a consolidation request. Call your loan servicer and ask them what loans qualify for PSLF. They should be able to tell you.How Would This Work in Real Life?

Here’s an Example. Meet Jane. She’s a pediatric cardiologist. Her total length of training between residency and fellowship is six years. During that period, she’ll start out at $55,000 and end up at $70,000 in salary. When she becomes an attending, she’ll start at $225,000 and get inflation level raises after that. Jane has $300,000 in student loans. She doesn’t know what to do with such a large burden, but she’s passionate about medicine. In a perfect world, here’s how she would manage her student loans.Start paying on REPAYE as soon as possible

While in residency and fellowship, Jane can pay only a few hundred a month but receive interest subsidies of thousands of dollars a year. The reason is that REPAYE covers half of the leftover interest she doesn’t pay each month. Since she’s going for tax free loan forgiveness but also wants to keep the loan balance low just in case, REPAYE is probably a great option. A possible exception to that rule of thumb is if her spouse makes a lot more money than she does and then it’s worth talking to an expert.File the PSLF Certification form

After her first payment on REPAYE during training, Jane can submit the PSLF employment certification form. She should receive a response in a couple months showing her progress towards loan forgiveness. Once she’s being tracked for the program, she should resubmit this free form every year at least to create a well-documented paper trail.Minimize Taxable Income

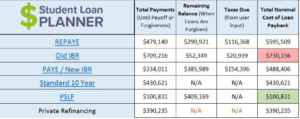

Loan servicers calculate what Jane owes every month based on her taxable income. If she will receive forgiveness on her student loans then she wants to minimize what she pays wherever possible. The best way to do that is to save in pre-tax retirement accounts. She can use a pre-tax 403b plan to put away up to $18,000 per year, which will directly reduce what she has to pay towards her student loans.Here’s What the Numbers Look Like

A few things might complicate this picture, particularly if Jane had a spouse who also earned an income. If a spouse has student debt then it doesn’t matter as much. However, if a spouse has no loans but a substantial income then it would be worthwhile to rerun these numbers using my calculator. So to review, Jane makes $55,000 at the beginning and $70,000 at the end of training. We’ll say she puts away $5,000 in her 403b during training and $18,000 as an attending. Her interest rate is 7%.

Jane borrowed $300,000, and she’s going to be able to pay just over $100,000 on her student loans and save a lot of money for retirement along the way. Student loan interest is generally not tax deductible except for a small amount at low incomes. That means over that 10 years, Jane receives a benefit worth about $20,000 annually after tax for optimizing her student loans. On a before tax basis, that benefit is more like $30,000 in salary value. That’s a great benefit considering many people enjoy working at academic hospitals over private practices.

So to review, Jane makes $55,000 at the beginning and $70,000 at the end of training. We’ll say she puts away $5,000 in her 403b during training and $18,000 as an attending. Her interest rate is 7%.

Jane borrowed $300,000, and she’s going to be able to pay just over $100,000 on her student loans and save a lot of money for retirement along the way. Student loan interest is generally not tax deductible except for a small amount at low incomes. That means over that 10 years, Jane receives a benefit worth about $20,000 annually after tax for optimizing her student loans. On a before tax basis, that benefit is more like $30,000 in salary value. That’s a great benefit considering many people enjoy working at academic hospitals over private practices.

What if Jane Wanted to Start a Family?

One cool feature of the PSLF program is that payments made while on maternity leave count towards the 10 years of payments needed for forgiveness. If Jane worked at an academic hospital, she could take off up to three months per birth and if she makes payments on REPAYE, PAYE, or IBR, she gets credit towards tax free loan forgiveness. As I mentioned, if Jane had a spouse, then that could make things a bit more complex. Keep in mind you’re married for the entire year for tax purposes once you submit your marriage certificate. I’ve met many couples who have three to four years of credit towards PSLF while they’re planning their wedding. If Jane had fallen into this category, she could probably count on at least a year for the student loan servicers to incorporate her spouse’s income into the payment calculation. If she uses PAYE once she gets married if that’s in her life plan, she can cap the required payment at no more than what’s required under the 10-year Standard plan. That capping feature allows most physicians to qualify for substantial loan forgiveness even if they’re a high-income surgeon like my fiancée.Plan for PSLF, but Prepare for an Alternative Plan Just in Case

If you’re in training right now, there’s no harm in tracking progress towards loan forgiveness on the PSLF program. If you decide to go private practice, you can refinance and get a lower interest rate with a private lender. If you decide to stay with a hospital, it will probably be a not for profit employer. You might as well set yourself up for this benefit as it’s worth tens of thousands if not hundreds of thousands of dollars. In case PSLF gets repealed, which is probably not going to happen for folks who already have loans, you’ll owe less by using an intentional strategy for loan repayment.

YNAB aka You Need a Budget. I bought this in Dec 2014 on some Christmas sale when it was still only available in the desktop version. Now it is a fancier web driven app.

Before using YNAB, I, like many, was a regular ol' excel spreadsheet gal. I made myself feel good by having all the budget categories add up nicely to my monthly paycheck. If you recall, I never saved any money and always ran out of money before the next paycheck.

My spending kind of went like this – do I have money in my checking account? Yes, I'll spend it. Meanwhile, I wasn't paying attention to the other categories I needed to set aside money for. I needed some serious help!

YNAB is not super easy to use right out of the box. I can almost promise you that you'll have some growing pains. The good news is that YNAB has a robust support center and tons of educational videos and webinars to teach you how to use their software optimally. When I switched from YNAB desktop to web version, they changed a few rules and I was emailing with their support team quite a bit.

My first few months with YNAB were interesting. I still went over budget, but each month got better and better. I slowly re-trained my spending habits. Remember that $20,000 credit card debt I used to have? Not only is it gone but I pay my cards IN FULL every month.

I can also confidently say today that I no longer go over budget and am saving quite a bit of money now (becoming an attending helped that part for sure). Learning how to use YNAB efficiently helped quite a bit as well.

Living within your budget revolves around clarity of the budget presentation and self-discipline. YNAB is a vital tool with which I feel I am able to keep disciplined and focused.

People ask all the time whether they should use YNAB vs. Mint. They are completely different programs. It really depends on what your needs are. If you are already great at spending within your means and budget (if you have one) – then Mint is a good option for you.

Mint gives you a snapshot of how you did. If you need serious help (like I did) and need to literally re-train yourself about budgeting and spending, then there is nothing better out there than YNAB.

YNAB is forward and proactive budgeting. You will know whether you can actually afford something in real time and not worry that your money will be taken away from other necessary categories. YNAB focuses on your cash flow. You can also add loans and investments for tracking purposes, but I don’t believe this function works too well. I’d recommend sticking to what YNAB was made for – cash flow. I use Personal Capital to get a more complete snapshot for all my accounts. We use eMoney with our FA as well.

I hope you're in a better place than I was when I first started YNAB. Even if you are I’d recommend checking it out. It is free for the first 34 days. Use this link to get 1 month free.

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]