Money

paid off my student loans earlier this year. But I finally took the plunge into real estate syndications, and I wanted to share how that unfolded.

Where I Started

As I mentioned, when I first got started with my financial goals and plans, I was laser-focused on my student loans. This is the first year I opened up a regular brokerage account at Vanguard. Up until now, I've been resisting all the advice to learn more about real estate and get some money in the game. Like many of you, learning about finances is a journey and requires continuing education. What's great about being in this physician finance space is having access to folks who have experience with real estate investing. But, even with offers of direct mentoring to buy my first rental property, there was also this fear of the unknown. I was filled with thoughts like, “Ugh, it seems so complicated and a lot of work,” and that kept me from taking that first step. Then I discovered real estate syndication and decided to take another look.

Real Estate Syndications for Dummies

First, what is a syndicate? A syndicate is a way for multiple investors to pool their money into an entity to purchase real estate. Why? This allows them to invest in much bigger properties than any individual investor could do on her own. Think large apartment buildings, self-storage facilities, senior resident living homes – these are examples of commercial real estate.

Sponsors and Investors in Real Estate Syndications

Syndicates consist of a sponsor and investors. The sponsor is the one person or company that has experience and manages the deal on behalf of the investors. They generally have skin in the game too, often putting up between 5-20% of the total equity. The investors are people like you and me who would like to invest in this type of real estate, but prefer to be a passive investor, or what’s called a limited partner. Syndications are generally set up as an LLC and the investor owns an interest in the LLC. Let me back up a bit, though. You may be wondering why these seem “new” – at least I did. Up until recently, general solicitation for private offerings was prohibited (meaning no public advertising of securities to investors – like through the internet). You basically had to know someone–a friend, a neighbor, and so on–who did these deals. That’s where the term “country club” equity comes from. The JOBS Act of 2012 relaxed general solicitation rules as long as certain conditions were met, including that each investor is accredited. An accredited investor is an investor who meets 1 of the following criteria:

- She has annual income of at least $200,000 for the last two years with the expectation of earning at least $200,000 in the current year or

- If she's married, they have a combined income of at least $300,000 each year for the last two years with the expectation of earning at least $300,000 in the current year or

- She has a net worth of at least $1 million, excluding her primary residence, either individually or jointly with her spouse.

As you can see, many physicians will qualify to be an accredited investor a few years after residency.

The Pros and Cons of Real Estate Syndications

Investing in real estate syndications is relatively passive, making it attractive for busy folks like us. Like all investments, however, the investor should do their own due diligence and understand what they are investing in. Another attractive feature of this type of investment is its favorable tax treatment. Real estate sponsors can use depreciation to offset income and reduce the amount of current taxes on cash distributions. The taxes can be deferred until the property is sold, at which point gains on the sale would be taxed at a lower capital gains rate versus ordinary income rates. These tax benefits are passed on to investors in a real estate syndication. Investing in real estate also provides increased diversification, given that real estate has a low correlation with other major asset classes like stocks and bonds. There are other important considerations to investing in real estate syndications. A major con is the illiquidity of the investment as the money is often tied up for several years. You cannot just sell your part of the investment if you want to. You'll have to wait until the property is sold. You also don't own any actual real estate outright; you own a share. For a real estate newbie like me, investing in syndications is the perfect introduction to real estate. Put some skin in the game and learn along the way in a relatively passive way. Trusting the sponsor is paramount. So one may ask, how do I know if I can trust a sponsor? There is no easy answer. Spend time talking to sponsors and asking about their experience in putting together deals. A vetted introduction by someone you trust is probably how most people start.

How I Got Started with Syndications

So whom did I ask when I was ready? My friend Dr. Peter Kim at Passive Income MD. He introduced me to Alpha Investing. What I love about Alpha Investing is that you'll always talk to a senior partner of the firm. They are a private group of experienced investors with strong relationships with high-quality sponsors. Alpha Investing aggregates investments from its members into a syndicate and invests into sponsor projects. This structure allows members to access exclusive real estate projects at significantly reduced minimum investments. So I jumped in. I invested in an equity deal through Alpha Investing where the sponsor acquired a $260 million high-rise 20 miles outside of the heart of Manhattan.

Are you ready to jump in? Alpha Investing is an invitation-only private capital network but readers of Wealthy Mom MD can request access here.

[ Disclosure: This blog post contains affiliate links. If you click through and use a service or purchase a product, I may receive a commission at no extra cost to you. Thank you for your support. ]

Is there anything that surprised you about real estate syndications? Have you made real estate part of your portfolio?

Most of the time I feel like I am running around like a chicken with my head cut off. Juggling being a dermatologist 4 days a week, mom to a toddler, fiancé and running this website (& podcasting !) can be challenging to say the least.

Wednesdays are my “day off” from seeing patients. I initially took Fridays off to have a 3 day weekend. But I found that with a new baby, traveling on the weekends stopped happening. I also found that many businesses and appointments I needed to do were difficult to schedule on Fridays either due to them closing early or being closed or Friday being so popular I could never get in. I also found that my patients wanted Friday appointments. I guess not too many dermatologists are open on Fridays.

So how do I spend my non-clinical week day? Here is how I spent it a few weeks ago.

6:30am Alarm goes off. I snooze too many times (Every Wednesday, my plan was to get up around 6am and do some writing for my blog before Jack wakes up. It has yet to happen.)

I finally get up around 7:30am. I make coffee.

I sit in front of my powerbook to see what I could work on writing wise by checking into Asana. I recently started using Asana to organize my whole life. Got this awesome tip from Travis of Student Loan Planner and Ryan Inman of Physician Wealth Services while I was at FinCon recently.

Jack starts cooing and babbling. He greets me standing in his crib. I change his diaper and bring him to dad who is still snoozing. They share some morning snuggles.

Jack starts cooing and babbling. He greets me standing in his crib. I change his diaper and bring him to dad who is still snoozing. They share some morning snuggles.

I make breakfast for Jack – 1 egg omelet with cheese, slices of oatmeal cake (from the Baby Lead Weaning Cookbook), sliced grapes and a cup of whole milk.

I skip breakfast as I do intermittent fasting most days.

8:45am I drop off Jack to daycare. His daycare is across the street – priceless.

I walk back home and half write a blog post, respond to some emails and comment on Facebook posts.

11:30am I head out to have lunch with Camilo of the Finance Twins. We met at FinCon and turns out we are both in Philadelphia. We chat about how we started our blogs and exchange ideas and tips for our budding businesses.

I uber back to my neighborhood for a 2:30pm dentist appointment. I get gently scolded for not flossing the back teeth. He suggests I use a waterpik.

I uber from the dentist to happy hour at Double Knot with a friend. In case you live in Philadelphia – this is the best happy hour deal in town.

I’m home by 6:30pm. Jack is eating dinner. Neither of us feel like cooking so it’s pizza night.

7:15pm Jack gets a bath. Then playtime with mom and dad. Bedtime for Jack is at 8pm.

Mom and dad time. I think I do some more work for the website but likely am just wasting time on Facebook.

Bedtime for me is around 10pm since I get up around 5:30am the next day and start seeing patients at 7am.

Hope you enjoyed this peak into a random day!]]>

This is the guest post by Travis Hornsby of Student Loan Planner. He's an expert in student loans and is married to a physician. Today, he's stopping by to discuss how PSLF might impact your career choices as a physician. Check out Travis’ ultimate (and free) student loan calculator here. If you’d like to learn more, check out how you can get student loan help here. Many new physicians are planning their lives around the PSLF program. They’re terrified if anything happens to this program, and they’re afraid of working part-time or switching jobs to a private practice. You know the old saying “don’t let the tail wag the dog”? Physicians can and should be choosing their career paths and their employers based on their passions, not their finances or PSLF. To see why, it helps to take a look at the math.

Why Physicians Should Leave Training with Lots of Credit Towards Loan Forgiveness

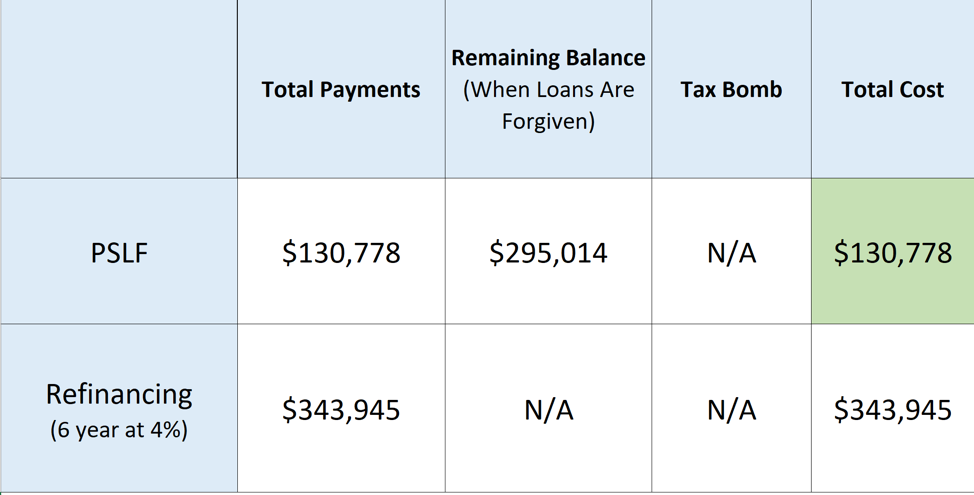

Unless you are positive you want to go to private practice, you should not refinance your student loans as a resident. The reason is because REPAYE will give you subsidies and cover part of your interest while you’re still in training. That’s why I see REPAYE being a good in-between option if you’re unsure if you want to work private practice or at a not-for-profit hospital once you’re an attending. My wife is a urogynecologist. She had a lot of issues with our loan servicer FedLoan Servicing, so we weren’t able to go for loan forgiveness. That’s one of the main reasons I started Student Loan Planner. That said, the physician graduating today should be leaving training with between three and seven years of credit towards Public Service Loan Forgiveness on average. That’s because most residencies and fellowships take place at qualifying employers.How Much is PSLF Actually Worth to an Attending Physician?

If you get a great job in private practice like Miss Bonnie MD, then pay off your debt quickly and refinance. However, pretend you are a rising OBGYN attending looking for a job. You have two options, one is a private practice paying $250,000 and the other is a giant university health care system paying $220,000. Let’s say you have $300,000 of med school loans. How much is the value of PSLF in this case? You’d spread the PSLF value over six years, since you’d be leaving training with four years of credit. Hence, the difference in payments is a bit over $213,000. Divide that by 6 (you need 6 more years as an attending to get PSLF), and you’d have an after-tax PSLF value of $35,500. You would need to adjust this for pretax salary value to see how much this benefit is worth.

To pick a round number, let’s say after adjusting for taxes, $35,500 a year in take-home pay benefit for PSLF is worth $50,000 in salary.

Hence, a $220,000 salary in the not-for-profit world would be equivalent to a $270,000 salary in private practice.

Since the private practice salary was $250,000 in this example, the extra value you get from PSLF is only about 20k a year.

Would you take a job that paid an additional 20k per year if there was something about it you didn’t like that much? Probably not.

Hence, the difference in payments is a bit over $213,000. Divide that by 6 (you need 6 more years as an attending to get PSLF), and you’d have an after-tax PSLF value of $35,500. You would need to adjust this for pretax salary value to see how much this benefit is worth.

To pick a round number, let’s say after adjusting for taxes, $35,500 a year in take-home pay benefit for PSLF is worth $50,000 in salary.

Hence, a $220,000 salary in the not-for-profit world would be equivalent to a $270,000 salary in private practice.

Since the private practice salary was $250,000 in this example, the extra value you get from PSLF is only about 20k a year.

Would you take a job that paid an additional 20k per year if there was something about it you didn’t like that much? Probably not.

Working Part-Time vs Full-Time as a Physician

Another thing to keep in mind is as a PSLF eligible physician, you don’t lose your credit if you decide to reduce your hours temporarily. You can even gain credit while on maternity leave for example (3 months per calendar year). Additionally, you could even go for the 20-25 year version of loan forgiveness if you were in a lower paying specialty and desired part-time hours for an extended period of time. If you decided to be full time again, you could pick up from where you left off on the PSLF clock. Don’t feel like if you don’t rush and get PSLF that it’s going away. It’s way too enshrined in loan promissory notes to be going anywhere in the near future.Get a Plan for Your Med School Student Debt

Miss Bonnie MD has paid off her student debt, and if you want to be like her, you’re going to need a plan. You could refinance it or go for forgiveness, but you better hope you’re making the right choice. Too many physicians are making decisions casually about the biggest financial decision they’ll make besides retirement and buying a home. Once you’ve got a solid plan in place, you can relax and focus on making your career all you want it to be. If you prefer not to spend time reading books on med school debt, then we’d certainly love to help you make a custom student loan plan. Regardless of whether you choose the Do It Yourself option or get a professional to help you, please pursue the path in medicine that you truly want. You shouldn’t feel pressure to work at a not for profit hospital just to get loan forgiveness anymore than you should work at a private practice just because it pays more money.Final Thoughts on PSLF and Med School Career Choices

Medicine is too rife with burnout and stress not to be in an employment situation where you can be happy with the results you’re getting for your patients. If that’s not the case, just make sure you know what you’re doing with your student loans and switch employers. Some huge percent of the physician workforce changes jobs in the first few years of practice. Take charge of your life and career and don’t let student debt or the promise of PSLF hold you back.]]>

if any, for your kid(s)'s education & life is a personal decision. There is no simple answer. I don't recommend doing any of these if your finances are not in order. Remember, there is no such thing as a loan for retirement. My 1 year old already has 3 accounts and about to open a 4th. Why? To take full advantage of time and compound interest of course. Here they are in order of when we opened them.

1. 529 College Fund

529s are the king of college savings accounts. You contribute after-tax money in, it grows tax free, and you don't pay taxes on withdrawal. You may even get a state tax deduction for your contribution. You can also open one before your child is born! So if you know you're going to have children and get a decent state tax break like I did when I was living in NYC, it's not bad a idea to get one going. Where should you open one? Start with your own state's plan. If you get a state tax break you'll want to find out if you're limited to using your state's plan to qualify for a deduction or not. A few states, including my now home state of PA, allow you to use any state's plan. So, I've kept mine with NY which currently offers the lowest fee Vanguard funds. We currently invest it all in the Aggressive Growth Portfolio which consists of 70% Total Stock Market Index Fund and 30% Total International Stock Index Fund. If your state offers no tax deduction then I recommend NY, Utah, or Nevada's plan. Pick Nevada if you already invest in Vanguard and want to keep things clean. Don't overthink it, just pick one. And – make sure you select the direct plan and not the plan via a financial advisor which are loaded with extra fees. There is a penalty if you withdraw money for non-educational purposes. Because of this I recommend saving something like 70% in a 529 and the rest in either a UGMA/UTMA or your regular brokerage (aka taxable account). There is a special rule allowing parents to frontload 529s above the gift tax limits. You may frontload 5 years worth (5 x $15,000 or $30,000 = $75,000 or $150,000). For those that can swing this, this is a great way to get that money growing for college.2. UGMA (Uniform Gifts to Minors Act)

UGMA & UTMA are basically savings and/or investing accounts for your children. You own the account as a custodian until junior reaches the age of majority. This age is state dependent but usually ranges from ages 18-21. Once they reach this age the account belongs to them and you lose control. Since this is an asset your child owns it will be counted for college financial aid calculations. The money can be used for anything. On the flip side, interest, dividends & capital gains are taxed. The taxation recently changed with the new 2018 Tax Law and will be taxed like trusts (15% & 20% tax above $2,600 & $12,700 respectively). Previously, the first $2,100 of unearned income (interest, dividends & capital gains ) was not taxed.3. Coverdell ESA

Huh? That's the usual response I hear when I recommend this account for children. I already discussed how great ESAs and how you can fund one despite being over the income limit (kind of like the backdoor Roth IRA). You can only contribute $2,000 a year but over time (and compound interest) you can have a sizeable chunk of cash to use for either private school and college. Although there is a new ruling allowing up to $10,000 per year withdrawals from a 529 account for K-12, not all states have adopted this. I also don't recommend doing this unless 1) you get a nice state income tax deduction (like NY) and/or 2) you frontload your 529 at or near birth. Otherwise the money just won't have much time to grow if you keep withdrawing money from it. Unlike the 529 plan, you cannot open one before your child is born.4. Roth IRA

[caption id="attachment_2545" align="alignleft" width="351"] Jack's Korean Dol outfit[/caption]

We haven’t opened a Roth IRA yet but will before the end of this year. Children can open a Roth IRA if they have earned income. Chores around the house do not count. Babysitting and working for your business do. In Eggy’s case, he’s a print model for this website.

What, you think he let me use this photo for free? Nope.

A Roth IRA for your children via a family business is a win-win situation. You pay your child for work, you get a business deduction, he/she gets earned income and can open a Roth IRA. Once inside the Roth IRA, the money is never taxed again! Better yet – until he makes a sizeable income through the family business he won't pay federal and likely no state income taxes as well!

Now, the key is to pay your child a reasonable wage for the work. It won't pass the snuff test if I paid Eggy $5,500 for a few photos on this website.

A quick reminder to stay under the gift tax limits for total contributions to your children's 529, ESA, and UGMA/UTMA accounts. Currently, the gift tax limits are $15,000 or $30,000 for married couples. So, in other words, don't contribute more than $30,000 across the 3 accounts in a year. An exception to this is the 5 year frontloading exception for 529s.

We opened and kept his 529 in NY. His UGMA and ESA accounts are at TD Ameritrade. We plan to open his Roth IRA at TD Ameritade since Vanguard does not allow minor Roth IRAs.

What do you think? Comment below!

]]>

Jack's Korean Dol outfit[/caption]

We haven’t opened a Roth IRA yet but will before the end of this year. Children can open a Roth IRA if they have earned income. Chores around the house do not count. Babysitting and working for your business do. In Eggy’s case, he’s a print model for this website.

What, you think he let me use this photo for free? Nope.

A Roth IRA for your children via a family business is a win-win situation. You pay your child for work, you get a business deduction, he/she gets earned income and can open a Roth IRA. Once inside the Roth IRA, the money is never taxed again! Better yet – until he makes a sizeable income through the family business he won't pay federal and likely no state income taxes as well!

Now, the key is to pay your child a reasonable wage for the work. It won't pass the snuff test if I paid Eggy $5,500 for a few photos on this website.

A quick reminder to stay under the gift tax limits for total contributions to your children's 529, ESA, and UGMA/UTMA accounts. Currently, the gift tax limits are $15,000 or $30,000 for married couples. So, in other words, don't contribute more than $30,000 across the 3 accounts in a year. An exception to this is the 5 year frontloading exception for 529s.

We opened and kept his 529 in NY. His UGMA and ESA accounts are at TD Ameritrade. We plan to open his Roth IRA at TD Ameritade since Vanguard does not allow minor Roth IRAs.

What do you think? Comment below!

]]>

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – Dawn.

Tell us about yourself:

I’m a 44 year old anesthesiologist living with my husband, almost 3 year old daughter, and almost 10 year old whippet dog in Salt Lake City, UT. I’ve lived in Salt Lake for 17 years, initially drawn here by a passion for rock climbing and outdoor sports, but my husband and I are originally from Arizona. We met in college and both pursued engineering degrees. After some experience working as engineers, we both decided to take different paths (he chose JD and I chose MD). I’ve been an attending anesthesiologist for over 7 years now. My practice is unique in that I am a non-academic faculty member of a large group at an academic hospital. I do all my own cases and see a wide variety of patients, but I have no call, weekend duties, research, or administrative duties. I also provide anesthesia for our university fertility clinic, a “side gig” which is near and dear to my heart because I was an IVF patient at the same clinic! I currently work two full days in the OR and 1-2 mornings a week at the fertility clinic.

Did you graduate with student loans?

My husband and I were both fortunate to have full-ride scholarships to a state university for our undergraduate degrees. He also attended the same state university for law school, where the tuition was heavily subsidized because his father works there as a professor. I attended a state university for medical school and did take out some loans, but my husband was working as a lawyer during that time so he was able to provide a majority of the financial support.

How fast (or not) are you paying them off?

Upon finishing residency, I had a relatively low amount to pay off. Despite a ridiculously low interest rate, I paid the loans in full within a few years of working as an attending.Financial aspects of kids

When did you have them?

For years my husband and I spent all our free time rock climbing and traveling, and we weren’t sure that we wanted to have children. That changed somewhere mid-residency, around the time that I turned 35. Suddenly, we felt differently about wanting to add to our family. Only I was experiencing some unusual symptoms and hadn’t had a period in over a year, all of which I attributed to the stress of being a resident. To make a long story short, I embarked on a diagnostic odyssey that lasted several months, included FMLA time, and culminated in the finding of a large pituitary adenoma. After resection (still during residency), complications, ICU stays, going on lifetime pituitary hormone replacement, and in vitro fertilization, I finally had my “miracle baby” at age 41!

Are you planning to fund their college expenses?

Although we were quite late at becoming first-time parents, we felt very mentally – and financially – prepared for the arrival of our daughter. In fact, around the time she was born, we started reading about the Financial Independence movement and realized that we were already financially independent. We were living well below our means and were used to flexible spending – being able to modulate our lifestyle and live cheaply if necessary – from many periods on the road as climbers in our twenties. In addition, we have a relatively frugal do-it-yourself type of outlook on most things.

Regarding our daughter, we opened a Utah 529 Plan at her birth, and we’ve been funding it modestly ever since. We also encourage our parents to give money to her 529 instead of giving cash (or other) gifts whenever possible.We could put more into her 529 each year, but we currently elect to fund it with the minimum yearly contribution necessary to get tax credits and invest our money in other ways. Although we see the importance of the 529 fund, we don’t plan to send her to private schools and we don’t plan to demand that she attend university. With the vast entrepreneurial opportunities brought by the explosion of the internet and social media, she could end up finding something she loves to do without a college degree. By that time, there should be a considerable chunk of $ in the account, but we hope to teach her lots of lessons about financial responsibility and value along the way. Both of us attended public schools and state universities for all of our education, and in the end, we had the same (or better) career opportunities as those who spent tens of thousands of dollars on their respective degrees.

What are your child care expenses? Are your kids in private or public school? What is the cost including after care if needed.

Although my husband and I both work part time, we spend money on opportunities for our daughter to have abundant social interactions with other children and adults. She currently attends one conventional full-day preschool daycare program two days a week and one decidedly unconventional outdoor play-based preschool two half-days a week. We love that she gets this mix of home time and away time, and we were never interested in hiring a nanny who is with her all day, every workday. Mornings when I work in the OR can be fairly hectic, so we also hired a regular babysitter who comes to our house for two hours on those mornings. She plays with, feeds and dresses our daughter before taking her to her preschool. It’s so helpful!

My husband and I both try to make our days off coincide with my daughter’s half-day outdoor preschool. That way, we get some personal time to spend alone or with each other while she’s playing in the forest. Also, we are very savvy about using our gym’s short-term daycare hours on the other days of the week. For all these permutations of childcare, I estimate that we pay about $1000-1200 per month. Every penny is worth it. Eventually as she gets older, we hope to convert all her preschool time to the outdoor play-based program, as it is more in line with our educational values. We also plan to unschool her when she reaches elementary school age, while continuing to expose her to whatever sports or artistic programs she takes an interest in.

Financial aspects of marriage

Are you married?

I’ve been married to my husband for 19 years, and we started dating near the beginning of college. We’ve truly “grown up” together and become more aligned in our values over the years.We have separate bank accounts. We dated for a long time before getting married and just never merged the accounts. There’s no regimented system, but we transfer money back and forth between accounts and take turns paying for various expenses depending on account balances. He makes more money than I do, but as an owner of his own law practice, his income is quite variable. He also allocates retirement money differently than I do, given that he is a business owner and I am a W2 employee. While we decide on big-picture money management issues together, he actually manages all of our finances in a Quicken program that combines all of our money transactions. He also does the taxes every year.

Do you and your husband agree on finances?

At first, my husband and I had very different views about spending. Overall, we agreed on the larger financial priorities, but I was much more of an emotional spender and he very logically saw money as “life energy” early on – before it was trendy. I wrote extensively about this in a recent post on my blog; my conversion to a more minimalist/valueist spending style didn’t happen until I became a mother and saw the simplicity and decreased stress that it brought to our household.Are you the breadwinner?

Interestingly, we’ve taken turns being the “breadwinner” of the household. I made the money straight out of undergrad that allowed us to buy our first home while he was in law school. Later, the tables turned when I was in medical school and he was establishing himself as a lawyer.Have you experienced a financial catastrophe?

When I was fresh out of undergraduate school working as an engineer, I made the mistake of succumbing to lifestyle inflation and spending most of my earnings rather than saving them. I elected to rent an expensive apartment and spent lots of money on clothes – things that don’t matter as much to me today. I had a 401k with corporate matching, but I didn’t even come close to maximizing my pre-tax contributions. I wish I had done this and continued to “live like a college student”, because that fund would be worth a lot more today (20 years later)! Now I make the maximum contributions to my retirement accounts and never even see the money before it’s allocated.

While I’ve been fortunate to not suffer a financial catastrophe, I have experienced a significant health crisis (see above). It changes your outlook on everything in your life – what’s important to you, how you want to spend your time, your money, etc. Because of my tumor, I no longer qualify for individual disability insurance, but we basically self-insure. We’re flexible enough in our spending to be able to deal with such a financial loss. We self-funded $50k in IVF fees over a three–year period by being financially flexible and cutting back on some unneeded expenses.

General Finances

What’s your FI (financial independence) number?

We consider ourselves FI by the 4% rule with a very reasonable yearly living amount, but neither of us are actually retired. We both enjoy our respective work in the capacity that we’re currently doing it – very part time and with ample vacation sprinkled in. The one thing we’d like to do in the near future is travel more with our daughter. My husband’s work is completely location-independent, but mine currently is not. So I might be adjusting things soon to accommodate for that. This may mean taking a sabbatical from my current position, going seasonal, or doing some locum tenens work. Also, I hope to grow my blog and social media presence, and potentially do more writing and speaking gigs.What is your net worth? How are you saving for FI/retirement?

Overall, our asset allocation is roughly 60% equities, 30% real estate, 10% cash. Simplicity is my theme word; it’s what I’m constantly striving for in many areas of my life, finances included. We are completely debt free, we self-insure for life and disability, we recently downsized our living space and also sold one of three properties. Most of our money is in the VTSAX index fund, and we don’t look at the gains and losses too frequently.What does FI/retirement mean to you? What does it look like?

I see our FI as a combination of good financial decisions, high income potential for both partners from a young age (given that we started out as engineers), and the ability to spend flexibly. Not everyone will have all of these factors in their FI equation, but figuring out your financial strengths and weaknesses can help to clarify and refine your own path to FI.

Any parting words of wisdom?

Tell readers a fun/random fact about you

When I meet people, they always want to know how tall I am. I’m 6’1” with no shoes on. And I have rock climbed in seven different countries.

And finally, where can people connect with you?

I blog at PracticeBalance.com. I’ve been writing more about money issues (mainly the mindset side of things) after meeting Bonnie this year, so check out my most recent posts and then work backwards from there to read about wellness, work-life balance, parenting, anesthesia, infertility… you name it. I’m also on Instagram @PracticeBalance, Twitter @DLBakerMD, and Facebook as Dawn Baker.

And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I'm so excited more women physicians are blogging about money and living a life of their own choosing. Definitely head over to Dawn's blog!]]>

2018 Me Has A Conversation With 1998 Me: Me on Money, Investing, Family, and Career – Part 1

This is a guest post by “Vagabond MD,” well known to those in the physician personal finance community. He is a 53 year old radiologist who recently emerged from burnout and currently works part time. He is married an attorney and has two children – one in college and one in high school.

2018: Dude, you were a total idiot for buying that fancy Euro car right out of training, on credit (of course!), before receiving your first paycheck. Bad on you!

1998: Hey, man, give me a break. I always wanted one and could finally afford one.

2018: No way, you could not afford it. You could afford the payments, not the car. Big difference.

1998: Nobody buys cars outright. Everyone makes payments, right?

2018: Well, the last six cars you (I) purchased were with a check.

1998: Really? Wow, I must have made a lot of money and saved some of it, too.

2018: About a year ago you read, “The Millionaire Next Door”, and it changed your life.

1998: True dat. I was on course to be a UAW (Under Accumulator of Wealth), and I turned that ship around.

2018: Keep turning it, bro. Here’s something else you should know. This investment and mutual fund “hobby” you are enjoying is actually making you poorer, not richer.

1998: How can that be? I am researching and discovering the stocks and funds and trading strategies that are going to make me wealthy by the time I am your age.

2018: Dude, you were a total idiot for buying that fancy Euro car right out of training, on credit (of course!), before receiving your first paycheck. Bad on you!

1998: Hey, man, give me a break. I always wanted one and could finally afford one.

2018: No way, you could not afford it. You could afford the payments, not the car. Big difference.

1998: Nobody buys cars outright. Everyone makes payments, right?

2018: Well, the last six cars you (I) purchased were with a check.

1998: Really? Wow, I must have made a lot of money and saved some of it, too.

2018: About a year ago you read, “The Millionaire Next Door”, and it changed your life.

1998: True dat. I was on course to be a UAW (Under Accumulator of Wealth), and I turned that ship around.

2018: Keep turning it, bro. Here’s something else you should know. This investment and mutual fund “hobby” you are enjoying is actually making you poorer, not richer.

1998: How can that be? I am researching and discovering the stocks and funds and trading strategies that are going to make me wealthy by the time I am your age.

2018: No, that’s what you think. But not how it works. You would be much better off learning about index funds and low cost buy-and-hold investing and shoveling as much excess income into these funds as you can. Forget about the hot manager (Van Wagoner), the value manager (Whitman), and any investment that begins with the word, “Janus”.

1998: Index funds, at Vanguard, with that weird Bogle guy, right? Nobody really believes that crap. Van Wagoner Emerging Growth was up 74% last year. I want some of that action!

2018: Van Wagoner Funds have been dead and gone for over 15 years. That kind of investing never works in the long run. Hardly anyone even remembers yesterday’s star managers. Everyone with half a brain is using index funds…and they really do work to build wealth, over time.

1998: Hard to believe, but okay, if I drop the investment hobby, what should I do with my free time?

2018: Study Italian Renaissance art, cook meatless paella, and learn to do some stuff around the house. All of them are more enjoyable and will serve you better than trying to pick future investment winners.

1998: Meatless paella? Am I still a pescatarian?

[caption id="attachment_2498" align="aligncenter" width="300"]

2018: No, that’s what you think. But not how it works. You would be much better off learning about index funds and low cost buy-and-hold investing and shoveling as much excess income into these funds as you can. Forget about the hot manager (Van Wagoner), the value manager (Whitman), and any investment that begins with the word, “Janus”.

1998: Index funds, at Vanguard, with that weird Bogle guy, right? Nobody really believes that crap. Van Wagoner Emerging Growth was up 74% last year. I want some of that action!

2018: Van Wagoner Funds have been dead and gone for over 15 years. That kind of investing never works in the long run. Hardly anyone even remembers yesterday’s star managers. Everyone with half a brain is using index funds…and they really do work to build wealth, over time.

1998: Hard to believe, but okay, if I drop the investment hobby, what should I do with my free time?

2018: Study Italian Renaissance art, cook meatless paella, and learn to do some stuff around the house. All of them are more enjoyable and will serve you better than trying to pick future investment winners.

1998: Meatless paella? Am I still a pescatarian?

[caption id="attachment_2498" align="aligncenter" width="300"] Meatless Paella[/caption]

2018: Yes, but now you are cheating because the word, “pescatarian” will not be known to you for a few more years.]]>

Meatless Paella[/caption]

2018: Yes, but now you are cheating because the word, “pescatarian” will not be known to you for a few more years.]]>

This past weekend over 2,000 like minded people converged in Orlando, Florida for #FinCon18. A place for financial bloggers, podcasters and influencers to meet “in real life” and exchange ideas and encourage each other to keep on spreading the message of financial freedom!

My favorite “online celebrities” were walking around, like Mr. Money Mustache, Jean Chatzy of Her Money, and even Joshua Becker of Becoming Minimalist!

My favorite part of the conference was hanging out with my fellow #FinConDocs! Close to 25 of us were there. How often do you get to hang out with doctors of other specialities who are financially like minded? These are my people! And the list of #FinConDocs keeps growing – some have said, or rather lamented about this. Ugh, ANOTHER copycat doctor finance blog? I beg to differ! There aren’t enough! Until every doctor is taking care of their finances there is more work to be done. Every one of us has a unique voice and not every doctor will connect with us.

Just some awesome #FinConDocs hanging out: Nii Darko of Docs Outside the Box podcast, his wife Renee Darko, Peter Kim of Passive Income MD, Carrie Reynolds of the Hippocratic Hustle Podcast, David Draghinas of Doctors Unbound podcast, Victor of 39point6 and Dr. Nikki of The Female Money Doctor (representing the UK!).

I learned a TON (and my to do list has ballooned by 1000000%). Here are some of the pearls I learned:

“Businesses die by suicide, not by murder”

LOOOOVE this quote. When we collaborate and support each other’s work, we ALL win. Cultivate a mindset of abundance not scarcity. I love that there are so many physician voices in the finance space. I love even more that there are more women physicians creating great content.

“Gratitude, not attitude”

Andy of the Marriage, Kids & Money podcast gave me this tip. He interviewed Rachel Cruze (daughter of Dave Ramsey) about gratitude at #FinCon18. Start the day writing at least two things you are grateful for. I’ve struggled to make this a daily habit for decades. This habit keeps your mind open and generous.

Outsource!

When I first started this blog I never thought I would get to a place where I would need help to manage it. FinCon taught me the value of having a virtual assistant to assist with the “the scut” so I can stay focused on creating content.

Find your niche, the specific the better!

Emma from Wealthy Single Mommy gave one of the closing keynote talks on tips for finding your avatar and niche. The more specific the better! This niche does not mean you’ll only get those exact readers! Emma caters to professional single mom but she also attracts married women (who may be angry or contemplating divorce and …isn't there a single mom in all of us?) and men. When I first started this blog I worried that my niche of women physicians was too small but it’s actually perfect.

Did you attend #FinCon18? Share a pearl below!

Physician burnout is on the rise, but I’d like to discuss a different type of burn out that I recently experienced. Specifically, I found myself facing FIRE burnout.

The Start of FIRE Burnout

Once I drank the financial independence Kool-Aid, I wanted to get there … yesterday. I found myself feeling envious and jealous of others who have achieved FI or those that are already able to work less. Must be nice, I'd think.

Impatience spurred lots of number crunching to see if I could somehow get around the fact that time is a pivotal part of compound interest. No matter how I ran the numbers, the truth is inescapable. There's no way around it.

Enjoying the Journey to FI

The goal of a FI is definitely a worthy one and en vogue according to the NY Times. However, like all goals, it is not about the goal itself but about the journey. Why is it so important to enjoy the journey? Because tomorrow is never guaranteed.

Sometimes you need to be personally reminded that tomorrow is never guaranteed.

A very important person in my life passed recently. Someone that truly helped sculpt who I am today. I didn't even know he was gravely ill. He never got a chance to meet Eggy.

These moments always cause the world to stand still. They prompt self-reflection and remind you to be present. They remind you that life is not a series of curated Instagram images. Life is now.

Life is what happens to you while you are busy making other plans – John Lennon

Final Thoughts on Facing FIRE Burnout

So, I am learning to enjoy the FI journey. Perhaps the best part of the journey is meeting other like-minded folks. They are truly a wonderful and supportive community. There may not be a perfect cure for burnout on the road to FIRE, but learning to enjoy the journey is a start.

How is your journey to FI going? Are you feeling any FIRE burnout? Comment below!]]>

This is Part 2 of Making A Million Dollar 18-year Bet, a guest post by Platinum Sponsor Johanna Fox of Fox & Co. Wealth Managementt, a fee-only financial planning firm. Start as early as you can As Bonnie says, compound interest is the 8th wonder of the world – you want to make it work in your favor. If you can afford to begin at birth, choose the most aggressive portfolio possible and contribute at least enough to get your state’s annual income tax break. Learn the rules in your state, too: some states allow tax breaks for contributions to other states’ plans and the cutoff for contributions vary: 12/31 in some states and 4/15 in others. Even if you can only afford to fund a minimal amount at birth, start with something as long as you are not compromising your retirement goals. In the Varkeys’ case, assuming 7.5% average return, choices include (not considering the time value of money):

- Frontloading the 529 with $108,859 (because they are allowed to frontload $75k/person, they can split the gift and fully fund college). OOP savings = $384,801

- Contribute $27,500/yr to the baby’s 529 for 5 years. OOP savings = $351,660

- Make monthly contributions of $818/mo. for 20 years. OOP savings = $297,380

Use ESAs for lower grades

Our couple hopes to send their children to private high school. In this case, we recommend they add Coverdell Education Savings Accounts (ESAs) in addition to 529s. ESAs are often overlooked because:- Contributions are limited to $2k/yr per child and

- Those with income over $190k are phased out from contributing (but you can get around this).

Underfund your 529s and ESAs

This may sound contrary to the key principle “start as early as you can”, but please bear with me and it will make sense. My goal is to use up all of the money in your tax-blessed accounts. Otherwise, in general, you’ll pay a 10% penalty on funds you withdraw that are not used for approved education costs. There are exceptions to the 10% penalty, such as if a child gets a scholarship, but not for just having money left over. Of course, you can pass account leftovers down the line to younger siblings, and we plan to do that, but I’m trying to keep it simple – say, you don’t need as much because your children decide to start out at a community college or want to go to a state school with a best friend, or, even worse, follow a boyfriend or girlfriend there. How can you possibly plan for that? To mitigate that risk, we recommend that about 75% of projected expense goes into ESA/529s, with the remaining 25% going into a taxable investment portfolio. When following this recommendation, start the taxable account only after you have funded the 75% in 529/ESAs, which will maximize your tax-free funding. If you end up needing the taxable account, you’ll be able to take advantage of lower long-term capital gains and dividend rates. If you don’t need the taxable account for education, voila! Can you say “beach home?” So what about med/grad school – what should the Varkeys do? At this level of income with 3 children, they will probably need to raise their family in a LCOL area of the country, plan to work extra shifts for a few years (if that is an option), determine to be extremely frugal, or save to fund a less expensive college experience – after all, they are saving for 6 educations. Possibly forego the private high school. Or they could save only enough for 50% of med school (1.5 educations instead of 3.) Remember, planning is about prioritizing how to allocate limited resources to achieve your goals. We’re back to priorities – what are your priorities about lifestyle and education? It’s very important to get those figured out in the beginning rather than simply saving what’s left over in your bank account each month. For example, one of our clients in this very situation has opted to set aside enough for med school for one child using the 75%/25% rule. If one or both of the other two siblings also decide to be physicians, then we are planning to have enough saved in a taxable account to also send them. This couple lives fairly frugally and in a LCOL area.Finally, invest aggressively if you can self-fund

Here’s the way I look at it – if you can cash flow the early years, particularly private K – 12, then you should keep your savings invested in a well-diversified equity portfolio up until the time you need it. If the market is down, we would plan to pay cash for private high school in this situation. If the market is climbing, we’ll liquidate enough of the 529/ESAs to pay the tuition annually. The 75/25 rule comes in handy again to prevent you from over-saving. And, of course, you can allocate your own savings any way you want: 60/40, 80/20, and so forth. By thinking through your choices, resources, and priorities, and then following your plan, you will have a much clearer path to saving for huge expenses that seem too far away to even think about when your children are young. I hope this information has been helpful!]]>… (or Smart ways to fund your children’s education) This is a guest post by Platinum Sponsor Johanna Fox of Fox & Co. Wealth Managementt, a fee-only financial planning firm. Until recently, she was also our financial planner. Saving for college is on the minds of most of our clients since around 75% either have young children, are pregnant, or both. The amount you need to save for education depends upon the choice of college, how many children you have, how much your funds grow, and the percentage of college, grad school and/or med school you want to fund. For a family with even two young children, you can easily looking at a need of $1M – $2M by the time they are ready to start college, especially if you plan to fund post-grad. Of course, that’s not even considering private school for K-12. Planning ahead and doing it right will both save taxes and increase your long-term net worth. But planning so far into the future for little creatures with minds of their own is a daunting and expensive challenge. To explain how to build an education savings plan for your own family, let’s review a case study. I’ve built a composite family, the Varkeys, using details from several clients’ plans:

- Dual physician family earning $680k/yr with children ages 2 and 6 plus another on the way

- Want to save enough for 4 years at Georgetown University, their dad’s alma mater, and maybe medical school.

- Hope to send children to private high school @$15k/yr/child.

- Student loans of $150k, refinanced @3.875%

- 2 mortgages: $850k on a $1.3M house and $450k on a rental duplex

- One spouse has access to a 401k and the other has access to a 403b/457b combo, and they both do annual backdoor Roth IRAs.

- And by the way: they hate debt

Prioritize

One of the biggest challenges of planning is prioritizing how to allocate limited resources to achieve your goals. The first rule in saving for education is not to sacrifice your own future: there are no scholarships for retirement and you will not be doing your children a favor by providing for nice educations at the expense of having to rely on them in retirement. However, you may be able to forego some retirement savings in the near term in favor of early education savings, and then get back on schedule. So, if your projections show that you will be able to skip a few years of 457b and backdoor Roth IRA contributions and have a few million dollars left at death, and that’s the only way you can fund your education accounts, then we might consider frontloading education to launch early tax-free growth and then return to maximizing all retirement space possible. Save for school or pay off debt? Since the debt feels so burdensome, I wouldn’t have a problem attacking the student loans heavily for 3 years but not the mortgage or rental interest. The reason is that student loan interest is not deductible, and lingering student loans are oppressive to many graduates because it represents nothing tangible. The interest on the mortgage is deductible as an itemized deduction and the interest on the rental will be deductible at some point – either when their rental begins to show a profit or when they sell it. And having tangible assets that are appreciating in value mitigates the emotional aspect of paying for “nothing”. Note: If you have access to an HSA, I would not forego contributing – ever (but that’s another article.)]]>

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]