couples finance

Since the engagement, everyone has been asking, “So, when's the wedding?” When most people think of engagements and weddings, the legal aspect of marriage is not the first thing that comes to mind. But saying “I do” is a legal contract. That's one of the reasons why we are happily engaged but not planning to be married anytime soon.

The fact that marriage is a legal contract isn't the only factor shaping our decision. In fact, here are the reasons in no real order:

- Marriage penalty tax

- M is divorced and has a child from a previous marriage

- Neither of us really feel like blowing money on a wedding

I have 6 figure student loan debtWe are trying to start a family

Marriage as a Legal Contract

Marriage is a legal contract and nothing more. People add the other stuff– mainly the religious part (we aren't particularly religious but our parents are). Don't get me wrong. I fully respect the institution of marriage and the commitment and all that it entails. It's just that legal marriage isn't the necessity it was for women as it is today.

The Marriage Penalty Tax Does Exist

Most people think you get a tax break by getting married. It depends.

Most people don't realize that the married filing jointly tax brackets are not double the single brackets. Depending on how much you and your spouse make, you may actually pay a marriage penalty tax. This mainly occurs when you both make a similar income. The marriage bonus mainly applies to couples where one spouse makes a lot less or is a stay at home parent.

Note: Since this post went live, there was a major overhaul in the tax code in 2018. The “penalty” is much smaller now.

The Divorce Rate Is Not Zero

Then there is the possibility of divorce. Divorce rates are going down and are lower among doctors (but higher among female physicians), but most of us still have a 30%-ish chance it won't work out.

Would you sign a contract that said things don't work out in 30% or more cases in which case you may lose half of your retirement and possibly a % of your future income? Of course not!

But that's what a marriage contract is. For some reason, all logical reasoning goes out the window when it comes to the marriage contract and nobody thinks they will be in that 30%.

Of course, there are lots of benefits to being married – spousal Roth IRA, unlimited gifts to each other, and double the federal estate tax limit to name a few.

Division of Property

Divorce laws are state specific and how they “split things up” falls into two categories – community property and equitable state. In a community property state (Alaska, Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin), any assets (and debts) acquired during the marriage are considered to be equally owned by both parties. In an equitable state, the more common type, anything acquired during the marriage is considered the property of the spouse that earned it.

Spousal Support

Then there is spousal support or alimony. In some states, while a divorce is in process, you may have to pay pendente lite support, or basically, alimony until the divorce is finalized and then pay actual alimony. Alimony laws vary by state in terms of how much and how long. Any high income earner should seriously consider a pre-nuptial agreement prior to marriage.

Blending Families Can Be Complicated

Bring in kids from a previous marriage and that can complicate things more. Laws are also state specific for child support and generally do not consider the income of a new spouse. No matter what your new family looks like, blended family finances are important to consider carefully.

Final Thoughts on Marriage As a Legal Contract

Marriage means different things to different people. It also means something in the eyes of the law.

Before you rush down the aisle, it's important to consider how marriage will impact your finances and family.

Ask yourself questions like:

- Do we need a prenup? (yes!)

- Who else would be impacted by our marriage?

- Do we understand how marriage could impact our taxes?

You can also check out this checklist for blended family finances to get the conversation started. And, consider delaying marriage or not getting married. Unmarried couples are becoming more commonplace now.

While these discussions might not seem romantic at first, it's another way to commit to your future together.

What do you think? Did you consider marriage as a legal contract before getting married?

Welcome to another installment of Interviews with Real Female Physicians. The goal of this series is to share their story so that you, the reader, may learn and be inspired from their experiences – good and bad. We all come from different backgrounds and have different situations. Some of you are married, some are not, some with kids, some with blended families. Let’s show other women that any of these can work financially! So let's introduce our next woman physician rockstar – Heather!

Tell us about yourself:

Hello, I’m Heather. I’m family medicine and a brand-new attending. I practice both inpatient and outpatient medicine at an academic hospital, and enjoy spending time teaching residents and students in addition to my clinical duties. I was born and raised in a medium-sized city in the Midwest with the greater metropolitan area approaching approximately 1 million. Both of my parents are practicing physicians. They gave me a small amount of money toward my education (to be applied toward undergrad), but otherwise the rest has been paid for through scholarships and loans. I came back to the same city to complete my residency and am now just starting faculty. Because my parents both work, they aren’t incredibly helpful with childcare, but it is still wonderful to be close to family! My husband is in his final year of surgical subspecialty training, and also plans to work in the academic setting upon his graduation. I have two young children, and am expecting my third child soon. I can’t say I have much time for hobbies after just finishing my training in a dual-physician household with young kids. In my former life, I enjoyed soccer, skiing, traveling, reading, and spending time outside. I went into medicine because I love helping people reach their greatest health potential. In family medicine, I feel I am in a unique position to do this as I am able to care for patients in the clinic, providing preventative medicine, education, and chronic disease management. When patients are sick, I am able to see them in clinic and also care for them in the hospital. I especially enjoy working with underserved patients, and academic medicine allows me to have a great diversity of patients with the majority of my patients not speaking English. Most days, I am happy with my decision, although it is frustrating the amount of paperwork and non-clinical duties I have to complete. It is sometime frustrating when seen as a lesser physician than specialists, especially when I graduated cum laude from medical school and as a member of AOA, and have such a wide breadth of practice.

Did you graduate with student loans? How much & what are the interest rates?

I went to a state school, and originally took out about $170,000 to pay for my education. Interest rates were between 5.16% and 7.90% and all unsubsidized. I did receive a partial scholarship all four years. I was awarded a full ride scholarship to a different school, but elected to go take out the student loan burden to attend medical school in the same city as my husband. While I would make the same decision again, it is frustrating to think of how my financial situation would be different without this loan burden. My husband graduated medical school with a similar loan burden.

How fast (or not) are you paying them off?

I paid off one loan in medical school, a Grad PLUS loan at 7.90% interest for only $3,000 taken out my first year of medical school. I paid this off my second year, when I was able to take out an unsubsidized loan at a lower interest rate (6.55%, so only a bit improved). I have not yet paid off my loans or refinanced them, although I am in the process of refinancing at the moment now that I am an attending. Although I qualify for PSLF, I am not pursing it as it makes me too nervous. I have paid the bare minimum through income based payments throughout residency, and my loans are now over $200,000 (yikes!). However, we have paid off more than $100,000 of my husband’s loans. We knew that my loans were much more likely to qualify for forgiveness or PSLF than my husband’s, and that I would be an attending sooner (thus able to refinance), so we’ve paid anything we can toward them in residency. I am comfortable with this plan and completely trust my husband, although I understand that some may not take this approach. We plan to continue to pay his off as aggressively as possible, and hope to be done with his loans in about 18 months. We will then aggressively pay mine down, and hope to be done within 4-5 years.

Financial aspects of kids

When did you have them?

I have two kids, and a third on the way. The first was born my fourth year of medical school, and the second in residency. They are both young, and when my next child is born, I will have three children under age four.

Are you planning to fund their college expenses?

Our kids do have 529s set up, although we haven’t significantly contributed to them given our own student debt. We encourage grandparents to gift toward them instead of extra toys for birthdays and Christmas. When no longer with our own debt, we would like to fund them with enough for them to attend an in-state university.

What are your child care expenses?

We have used day care exclusively for my children. I did not feel comfortable with a nanny or spending time alone with infants, so went the daycare option. We are overall happy with our decision, although sick days and drop off/pick up times have been stressors in the past. I currently spend $1200 per child per month, which means I will soon be spending $3600 each month in childcare. This is, by far, our largest monthly expense. We also spend quite a bit more on trusted babysitters (especially college-aged family members) to help us with early morning, late evenings, nighttime, and weekend coverage. Now that I am an attending, I have the luxury of more predictable hours.

Are your kids in private or public school? What is the cost including after care if needed.

We plan to send our children to public school when they start kindergarten, as we have good public schools in our area and like our children to be exposed to diversity.

Financial aspects of marriage

Are you married?

I am married.

Did you get a pre-nuptial or post-nuptial agreement?

We got married in medical school and had no prenuptial agreement – we only had debt at the time!

Do you and your husband agree on finances?

We agree on finances, largely because I am responsible for almost everything financial in my household and my husband agrees with my decisions (and is grateful he doesn’t have to do it)!

What financial mistakes have you made?

I probably could have taken out slightly less student debt as I graduated with approximately $10,000 in my bank account. I did eventually use this to pay down student debt, but was worried about keeping enough of an emergency fund available. I contributed the maximum amount my Roth IRA since I was 16, however, I put the money in and didn’t invest it for quite a while because I was overwhelmed with the options. While I am grateful for this money, I wasted the benefits of years of compounded interest.

Have you experienced a financial catastrophe?

We have been fortunate to have avoided any financial catastrophe.

General Finances

What’s your FI (financial independence) number?

We don’t have an FI number, largely because it seems too far away at this point. We are aggressively paying down student loans, and then would like to move to a bigger (but still modest) house. I am working 80% as an attending, but would love to decrease that further to 50-60% in the future if financially able (and my department supports this!).

Who handles the finances in your relationship? Are you DIY or do you have a financial advisor?

I handle almost all the finances in our relationship. We DIY. This does result in some mistakes (such as not investing Roth IRA initially, as mentioned above). I do budget through Mint, more to track our spending. Both my husband and I are fairly frugal. We rarely spend money on entertainment, eating out, or travel. Any leftover money not used by childcare, mortgage, monthly expenses, or to replenish our savings/emergency fund goes toward loans. As we finish our training and have more control over scheduling and finances, we would love to travel more.

What is your net worth?

We do own a modest 3 bedroom home. It was purchased at the start of residency for around $175,000, as we had a dog and a monthly mortgage was cheaper than renting a house with a yard. We also knew we planned to be in the city long-term. It is currently valued at $230,000. We are hoping to pay off our student loan burden (or at least be close!) before moving to our “forever” home. I don’t plan on a new build or anything extravagant, but I do wish for a bit more space for our growing family! In addition to our student debt and mortgage, we do have one car loan. When we found out we were expecting our third, we needed something bigger than a compact sedan to accommodate three car seats! We are typically pretty opposed to financing things, but our car interest rate (0.5% for three years) is so much lower than our student loan interest rates (lowest rate 5.16% and most at 6.55%) that we used the money for the car to pay down our student loans and will both be attendings to pay off the car loan before the three years are up. I am fairly conservative and keep at least $10,000 in our emergency fund. I know I could probably get by with much less, given that we are a dual-physician household, but with young kids and a current pregnancy I don’t want to be caught surprised.

How are you saving for FI/retirement?

We both contributed to Roth IRAs maximally from age 16 until starting medical school. Neither of us contributed anything in medical school. We then contributed to our Roth IRAs maximally in residency, but no other contributions. Now that I am entering the attending world, I will have a 403(b) and 457(b). As a university employee, I get fairly generous matching starting next year (2019). We plan to maximize these contributions starting next year. The area of finances I feel most deficient in is investing. We do our investing ourselves. I admit I don’t fully understand investing/the market. Most of our money is in index funds, like the S&P 500. I would like to learn more about this in the next year to better invest my money.

Do you have insurance?

We both have term life insurance, no whole life insurance. We both have personal, own-occupation disability insurance. We have umbrella insurance through our home/car insurance company. We’ve never had to use it. We also just established a revocable trust and updated will.

Do you give to charity? If so, where and why?

We give to charity, although only about 2% of our net income. We would like to give closer to 10-15%, as soon as our loans are paid off. We currently/plan to contribute to our church, our undergraduate university, and local organizations we support.

Any parting words of wisdom?

Our financial plan largely comes from White Coat Investor and Dave Ramsey. We are financial amateurs, but we at least know where our money is going each month and can use that to cut it down to the bare minimum to allow for loan repayment. We are both so excited to be a bit more loose with our money as soon as we don’t have that over our heads!

Tell readers a fun fact about you

I took a month off between residency and starting as an attending, and it was wonderful to spend time with kids, catch up on life/adulting, and be able to read my first book for pleasure in 5 years (whoops!)

And … that's a wrap! If you're interested in doing this please send me an email – I'd love to hear from you!

I loved reading Heather's story and I hope you did too. I was totally inspired about reading how she was able to take control of her and her husband's finances and get on track for financial freedom.

If you're interested in learning more about finances and don't have the time or interest to wade through books, blogs, and online forums then this course is for you. I wish this course was available when I first got interested a few years ago. I had to read several books, read a ton of blog articles, and post a lot of questions online to learn what I know now.

When you finish the course, you’ll feel confident that:

If you're interested in learning more about finances and don't have the time or interest to wade through books, blogs, and online forums then this course is for you. I wish this course was available when I first got interested a few years ago. I had to read several books, read a ton of blog articles, and post a lot of questions online to learn what I know now.

When you finish the course, you’ll feel confident that:

- You have all the insurance you need at the best possible price and none of the insurance you don’t need

- You are managing your student loans the right way, maximizing the benefits of government programs, minimizing interest paid, and getting out of debt as soon as possible

- You are either capable of managing your investments yourself, or you are paying a competent advisor a fair price to do it for you

- You are saving enough money to reach your goals and can spend the rest on whatever you like without feeling guilty

- You aren’t paying any more taxes than you need to

- Your children and your assets will be taken care of if something should happen to you

- Your assets are protected from lawsuits as much as possible with a simple, straightforward, and inexpensive plan

- You have a written plan to follow that will guarantee your financial success

Click here to find out more details and to purchase with code: MATCHDAY18 for 15% off

As an affiliate for this course (the course is the same cost to you regardless of who you purchase from) I was able to take the course for free. It is quite comprehensive and I cannot think of a more time efficient way to learn this stuff. Have you taken the course? Comment below! ]]>

push presents are a thing. And it turns out that I got the best push present ever!

About a year ago, M asked me to marry him and promised to keep our net worth positive. At that time, I was dragging us down with my student loans.

Well, not anymore! M paid them off!

Yup, I no longer have student loans. Happy dance in order:

And, we are now officially DEBT FREE !!!!!!!!!!!!

The Case to Wait to Pay Off Debt

I hear people say all the time that you don't “need” to pay off low interest debt quickly. I see their point and I wasn't planning on paying off these loans for another 3 years. Right out of residency, I favored maxing out my tax advantaged retirement accounts over making extra payments towards my student loans.

Why No Debt Is the Best Push Present Ever

Despite this argument, having no debt really feels fantastic. And it comes with some really significant perks too.

Being debt free means:

- No extra monthly payments

- A lower monthly operating budget

- Any extra money we get goes to us, not debt

Final Thoughts on Being Debt Free

Existing loans and taking on new ones (mortgage, car loans, etc) give you the illusion that you can afford something you actually can't.

Like 0% interest car loans – trust me, they aren't doing that to be nice to you. They know you will buy a more expensive car on credit even if you aren't paying interest. After all, it's just another monthly payment, right?

Couples who pay off debt together stay together. Of course, not every couple might have the means or the desire to pay off debt in one fell swoop like this. The most important thing is to make sure that you're on the same page financially, or at least taking steps to get there. Having solid financial footing before bringing a baby into the world truly feels like the best push present.

2018 is well underway. Last year, M and I had a good amount of tax advantaged retirement “pots” available to us along with some employer match and contributions:

- My 403(b) + generous employer match + contribution

- My 457(b)

- My cash balance plan

- My backdoor Roth IRA

- My solo-401(k)

- His 403(b)

- His Roth IRA

- His solo-401(k)

- My 401(k) + employer match

- My solo-401(k)

- My backdoor Roth IRA

- My HSA

- His 401(k) + employer match

- His Roth IRA (may need to backdoor it this year)

- His family HSA

- Our taxable account

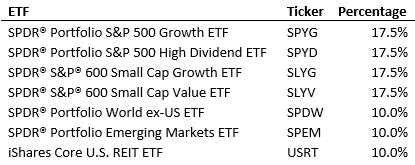

- 68% US stocks

- 17% Large cap growth, 17% Large cap value

- 17% Small cap growth, 17% Small cap value

- 24% International stocks

- 12% Large cap developed countries

- 12% Diversified emerging markets

- 8% US REITs

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

We will be opening our taxable account at Vanguard.

What do you think? Comment below!]]>

I've estimated that these mistakes have cost me at least $350,000. Meaning that if I didn't make them, I'd have at least that much more money saved. Big sigh.

Here are the biggest financial mistakes I've made and survived to date:

#1. Cashing out my old work's 401(k) plan & selling company stock

I started a coveted job at Morgan Stanley in 1999 right after college. It was the height of the tech boom. My starting salary was $50,000 + a small guaranteed bonus. (I made the same as a resident in 2012!) My first 6 months was in London with all expenses paid.

I was an ex-pat there – meaning I was paid my U.S. salary but received free housing (picture beautiful 2 bedroom, 2 bath furnished apartment with marble bathtub, heated towel stand across the street from Hyde Park, neighboring the Grosvenor House) and a generous cash per diem. I did not have to spend any of my actual salary to live in London.

Now I don't totally regret this part – I was able to explore Europe on the weekends – weekend trips to Paris, Spain, Amsterdam. Priceless. Back then, friends and family from NYC could visit me in London for less than $400 roundtrip.

Plus, I had access to a 401(k) plan for the four years I worked there. I'm pretty sure I didn't max it out, but I still had a nice chunk in that account.

Still, I cashed it out in 2004. Yup, it gets worse. In addition to a company match, we also got free stock as part of our retirement plan. I sold it.

#2. Barely saving despite high earnings as a 22 year old

I listed my starting salary in mistake #1. About 1 year later, I got a $22,000 raise and a $25,000 bonus. This meant I hit 6 figures at the tender age of 23.

My only wish is that I had some savings to show for that! I lived paycheck to paycheck despite a high income. I guess I can blame NYC.

#3. Racking up $20,000 in credit card debt before starting dermatology residency

Yeah …. someone went a little nuts during intern year in NYC. I had awesome clothes, though. I paid it all off before graduating residency. Thankfully, I no longer carry any credit card debt and pay off cards in full every month.

#4. Not funding a Roth IRA until 2014

The Roth IRA was enacted in 1997. I've been earning money since at least 1992, so I'm not even counting opportunities to fund a regular IRA prior to that!

I actually never heard of the Roth IRA until sometime during residency so I feign ignorance prior to that. I couldn't imagine forking over $5,500 a year as a resident, but I totally could have. This is especially true because I moonlighted most of residency.

#5. Not paying off student loans during residency

Every year during internship and residency I meticulously applied for deferment or forbearance on my student loans. Isn't that what everyone does? Apparently not.

By the end of residency in 2015, I had almost $50,000 of interest capitalized onto my loans.

Surviving My Biggest Financial Mistakes

You can always earn more income, but you can't create more time. That's why some of these financial mistakes really sting.

Despite these awesome mistakes, I should be able to reach Financial Independence within 15-20 years and pre-Financial Independence within 10 years or less.

Feel free to share your mistakes below!]]>

The blended family is defined as a family consisting of a couple and their children from current and previous relationships. Blended families are on the rise and you need to know how to prepare yourself financially.

I've already written about a Premarital Financial Checklist that all couples should consider before walking down the aisle. In this post, I'll discuss some of them in more detail. Plus, I'll share some possible legal & financial ramifications for blended families.

Please note – I am NOT a lawyer. I strongly recommend you consult with a family lawyer in your state (and the state bonus kids live in).

To kickstart your blended family finances, here's what you need to know:

1. Know your partner's full financial obligations to his/her children and ex-spouse

You'll want to know if your partner owes alimony or spousal support. Specifically, you need to know how much and for how long. You'll want to know what his/her child support obligations are and for how long.

Each state has different age limits – 18 through 21+. Generally, if the child goes away for college, support payments stop. If the child lives at home, payments continue.

You'll also want to find out what their financial obligation for college is. In general, this is split between the biological parents in proportion to their income.

I strongly recommend reading your partner's divorce decree and parenting agreement to know what the obligations are. Often, parents are required to have a certain amount of life insurance for their kid(s). This area is one big reason I recommend delaying marriage for blended families.

I have read M's divorce decree and understand his child support obligations as well as his required life insurance requirements for his son.

2. Consult a family lawyer

Just like you'd have a lawyer review your job contract, make sure you consult with a family lawyer in the state where the bonus children live (where the custodial parent lives, if not with you and your partner).

Ask them if your income could ever count and/or if there is precedent for this. They will generally say no.

This does not stop an ex-spouse from going after your money, especially if your partner is making less than usual or went back to school. Child support laws vary by state.

I consulted with 2 family lawyers and both told me to not get married!

3. Consider Delaying Legal Marriage

You may have heard that your income and assets won’t matter since they are not your biological children, but that may not be the case. This will not deter an ex-spouse from trying to get at your assets. Even if the suit is frivolous, you will still need to hire a lawyer (read: more fees) and spend time on the matter.

This is a top reason to delay marriage until the children no longer require child support and college support. The FAFSA does not ask for your income, but the college can.

If you are going to take this route I highly recommend you get paperwork in place – Wills, Health Care Proxies, and Power of Attorneys, especially if you have children with your partner.

We are delaying marriage until his bonus son graduates college.

4. Prenuptial Agreement

Prenups are essential for blended families to protect the interests of the partners (and children). This is a whole other topic and are state specific.

My advice in short would be:

- Keep premarital assets separate.

- Agree to keep retirement accounts.

- Discuss spousal support.

- Child support and custody cannot be stipulated in a prenup.

We are not married now but plan to have a prenup when we do tie the knot.

5. Estate Planning

Estate planning is definitely more complicated with blended families. I often see contention when there are bonus children and new children from the blended couple. Figuring out how to make sure the partner and children are taken care of requires gentle treading.

It is also difficult to really know what the assets and means of their ex-spouse truly is. If you are reading this post, chances are, you and your partner will have the means to be generous with everyone.

As mentioned in #1, your partner may have life insurance obligations to his/her children from the previous marriage. Take this into account when deciding on additional life insurance policies if needed.

My advice: Do not be stingy with your bonus children. Reverse the situation and see how it feels if your partner decided to cut them out if they were your children.

We have wills, POAs, HCPs and living wills. We have named each other as beneficiaries. Both children are well taken care of.

6. Financial Planning & Logistics

Blended families are often older when they marry and may continue to operate as separate financial houses. I recommend seeing everything as “one pot.” This does not necessarily mean having one joint checking account, however.

I favor the one joint checking account for joint expenses and two separate accounts. Additionally, I strongly encourage blended families, like all families, to plan financially together. This will take some additional planning to ensure everyone is taken care of.

At this time, our banking accounts are totally separate, but we operate as “one pot.” I ensure both of us max out our tax advantaged retirement accounts as it is all going towards our retirement.

Final Thoughts on Blended Family Finances

When you blend families together, things can get complicated and they also also usually wonderful. One of the ways to mitigate some of the tension and conflict that might come from mixing families is to have the hard conversations upfront. The sooner you do it, the better. Using these talking points, you and your partner can get your blended family finances in order so everyone is taken care of.

Any other tips for blended family finances? Comment below! ]]>

legally married and not be aware of it. Ahem…we aren't.

Marriage has some legal benefits, but it also comes with several disadvantages as well. I've discussed before that marriage is a legal contract.

Most people do not think of it this way and do the typical “I love you” marriage. Historically, marriage was not meant for “love.” It was, in many ways, a business transaction between families.

Moreover, current marriage and divorce laws were put in place to mainly protect the woman as women often were homemakers and would be financially devastated in the event of a divorce. Hence why there are alimony or spousal support laws.

As more women join the workforce and become the breadwinning partner (this is often the case for women physicians!), these laws can seem antiquated and often work against us.

My goal is to make you aware of all the pros and cons of legal marriage. I am not suggesting that you never get married. But, it may make a lot of sense to delay marriage for some time.

So, here are the reasons to consider delaying legal marriage:

Marriage Penalty Tax

Most people think you get a tax break by getting married. It depends. Most people don’t realize that the married filing jointly tax brackets are not just a matter of doubling the single brackets.

Depending on how much you and your spouse make, you may actually pay a marriage penalty tax. This mainly occurs when both partners make a similar income. The marriage bonus mainly applies to couples where one spouse makes a lot less or is a stay at home parent. Here is a calculator to see if you'll get a marriage bonus or penalty.

Since this post went live there has been a major overhaul in the tax code in 2018, so the marriage penalty is lessened.

Blended Families

Blended families are commonly defined as one partner brings in children from a previous marriage or relationship. This factor can add complexity to the relationship. If this is your situation, that doesn't mean marriage is off the table. It's just worth considering the complexities of the situation.

You should be aware of all the financial obligations your partner has and consult a family lawyer in the state of custodial residence of the children. Child support laws are state specific. You may have heard that your income and assets won't matter since they are not your biological children but that may not be the case. This will not deter an ex-spouse from trying to get at your assets. Even if the suit is frivolous, you will still need to hire a lawyer (read: fees) and spend time on the matter.

In my opinion, this is a top reason to delay legal marriage until the children no longer require child support and college support. The FAFSA does not ask for your income, but the college can. If you are going to take this route, I highly recommend you get paperwork — Wills, Health Care Proxies, and Power of Attorneys — in place, especially if you have children with your partner.

Student Loans

Delaying legal marriage can make a lot of sense financially if you are with another high income earner and you're pursuing some some of income-based repayment for student loans. Otherwise, most attendings have their loan repayment as an attending capped out at the standard 10 year plan. That means that there is no benefit unless the debt to income ratio is above 2 for the attending.

If you are getting married, timing matters! Do not get married in November or December due to the timing of recertifying payments. January weddings are great because of when you need to certify repayment, which looks back at prior year tax returns. Before delaying marriage for this reason, I definitely recommend seeking professional student loan advice.

Financial Issues

One of the biggest challenges in a relationship comes when you and your partner are not on the same financial page. I recommend premarital financial counseling for all couples. Through this process you may find there are some major discrepancies.

Getting married will not magically fix them (or other pre-existing issues!). If both of you are committed to each other despite these differences, take the time to iron out them out before walking down the aisle.

The Divorce Rate

And finally, you might want to delay legal marriage because the divorce rate is > 0%. This may seem obvious, but no one really thinks about the divorce rate nor do they think they will get divorced. The divorce rate overall is not 50% as often quoted and even lower among physicians and highly educated folks. You're looking at 25-30ish%. But it still is not 0%.

I think it is foolish to think divorce cannot happen to you. This is not a reason in itself to not get married. Premarital counseling, discussing common life goals, and a well thought out prenuptial agreement will go a long way.

Why We Plan to Delay Legal Marriage

We will face a marriage penalty tax. I'd rather throw the 5-10K in penalty taxes towards my student loans. Also, my income would bump M up to my tax bracket, so that means less take home income for him.

We are a blended family. He has a son from a previous marriage. Unfortunately, us getting married puts us at financial risk. After consulting a few family lawyers, they all told me I should delay marriage until my bonus son has completed college as my income will likely be imputed for his financial aid eligibility.

Final Thoughts on Delaying Marriage

This isn't about not being in love or not being committed. In fact, deciding to wait to get married could be another way to show just how dedicated you are to your relationship. Whether you decide to wait or not, make sure you consider each of these reasons before tying the knot.

What do you think? Would you consider delaying marriage?

NY Times questions to answer before marriage. First, congratulations on meeting someone special. Feels great, doesn't it? Now, wouldn't you want to make sure you have the best possible chance of making it? Well, I'm no John Gottman and I can't predict the likelihood your marriage will succeed, but I do know that some pre-marital financial planning can go a long way to ensure a happy marriage.

Remember, marriage is a legal contract and you are uniting assets, not just families. That means that you need pre-marital financial planning. Yes, even if you're in love. Truly.

I suspect many people avoid this topic for a number of reasons. It's not “romantic.” Or it doesn't feel that way at first.

I actually think it is romantic to talk finances. You are establishing a deeper layer of trust that happens when you fully disclose finances to each other. By making financial goals together as a couple, you envision the future together.

Let's talk about something truly unromantic. Imagine being that woman or man who is ill-prepared to deal with the financial consequences if things go south. Being stuck in a marriage where one party is spending everything, leaving the other to salvage whatever money is left. Perhaps, it even comes down to one person hiding assets. That is truly unromantic.

I will not be discussing prenups (but if you need a refresher, click here!) in this post, but these discussions are the foundation of creating one.

Question 2 of the aforementioned NY Times Questions is the focus:

Do we have a clear idea of each other’s financial obligations and goals, and do our ideas about spending and saving mesh?

Let's break it down further:

1. Money history

What did money mean to you growing up?

If you don't know how your partner grew up financially, this is a good time to find out. For example – did they ever have to worry about whether there was enough money for dinner? What money lessons, if any did they learn growing up? This is also a good time to start learning about each other's parents' and other family member finances that can affect you. This will be further delved into below.

2. Income

How much do you earn? Is this job stable? What are you career goals?

3. Financial obligations: Liabilities and Debt

Do you have debt – how much and what kind? How do you feel about having debt (debt tolerance)? What is your credit score? Have you ever filed for bankruptcy? If one of you owns a business – find out if you/your partner can be personally liable if sued. What are the business' assets and liabilities? If this is a second marriage and/or if there are children from a previous marriage or relationship:

Do you pay alimony? How much is left?

Do you pay child support? How much? When does this obligation end?

What is your financial obligation for funding their college and more?

If there is an ex-wife/husband: Any concerns that s/he will ask for more financial support?

I strongly recommend reading their divorce decree and parenting agreement.

4. Assets

Do you own property? What retirement and other accounts do you have and what are the current balances? How much do you contribute to these accounts yearly? What is your net worth?

5. Spending

How do you decide to make a large purchase? Do you budget? Do you have credit card debt?

6. Goals

What are your financial goals and by when?

This is a good time to really find out if you and your partner have even thought about “retirement” goals, or as I prefer to call it reaching financial independence.

7. Practical matters going forward

How will we handle finances together? Joint and/or separate checking accounts? Over what amount should we discuss making a large purchase? Will we jointly own future purchases of homes and other investments? How are we going to handle pre-marital assets and liabilities? Will they be jointly shared or remain separate?

8. Finances of parents

Are our parents (insert siblings and other potential family members here) financially stable? Is there a possibility they may need our help in the future? How do we feel about that?

As if it wasn't enough to discuss each other's finances, you need to know what the financial state of their parents and siblings are. This is semi-addressed in question 11 of the NY Times questions:

Do we value and respect each other’s parents, and is either of us concerned about whether the parents will interfere with the relationship?

Financially ill-prepared parents and family members are common. Not being on the same page on this topic can wreck havoc on a marriage. It's tough to be prepared for this, but having a conversation in advance can help.

So, did my partner and I go through a checklist? Not this systematically, but, I did ask him most of the above questions before we got engaged. I am fully aware of his assets and liabilities. I have read his divorce decree and parenting agreement. We did all of this to make sure that our relationship is on the same financial page.

Continuing Your Pre-Martial Financial Planning

If you're a female breadwinner, I highly suggest this book. You can also work with different counselors or therapists. Some people think that having an outside perspective can keep the emotions at bay, allowing you to better focus on your goals and dreams. No matter how you proceed with your pre-marital financial planning, it is important to start conversations and ask questions now. You might not think it's romantic, but it's a great way to say how much you love your partner.

![]() What do you think? Comment below. ]]>

What do you think? Comment below. ]]>

Last month I spelled out how we are investing our money in 2017. I mentioned there were some moving parts – namely, M was unemployed and we knew, at the time, that I was (newly) pregnant. Now, M has a job (yay!) and looks like this pregnancy will stick, so now we can do some real projections for 2017. Our asset allocation will remain the same.

This year our total “retirement” contributions will consist of:

This year our total “retirement” contributions will consist of:

- $18,000 my 403(b)

- $20,800 employer match + contribution into my 403(b). Currently 20% vested. 40% vested as of August 1, 2017 so actually $8,320

- $18,000 my 457(b)

- $5,500 my Roth IRA

- $18,000 his 403(b). No matching at this time

- $11,000 his Roth IRA (his first! For 2016 and 2017)

- Other sources:

- A very modest amount ~$1,000 into my solo-401(k). Yes this blog likely won't lose money this year 🙂

- ~$5,000 his solo-401(k) – he has some 1099 income this year

Get started on your journey to wealth by getting my FREE book- Defining Wealth for Women.

[convertkit form=7480157]